Greystone Logistics, Inc. (OTCQB: GLGI) – Q3 2025 Earnings

Greystone Logistics, Inc. (OTCQB: GLGI) – Q3 2025 Earnings

Earnings Release Date: Apr. 15, 2025

Stock Price: $1.04

Market Cap: $29.4 million

Q3 2025 sales of $14.3 million vs $14.0 million in the prior year

Q3 2025 EPS of $0.05 vs $0.01 in the prior year

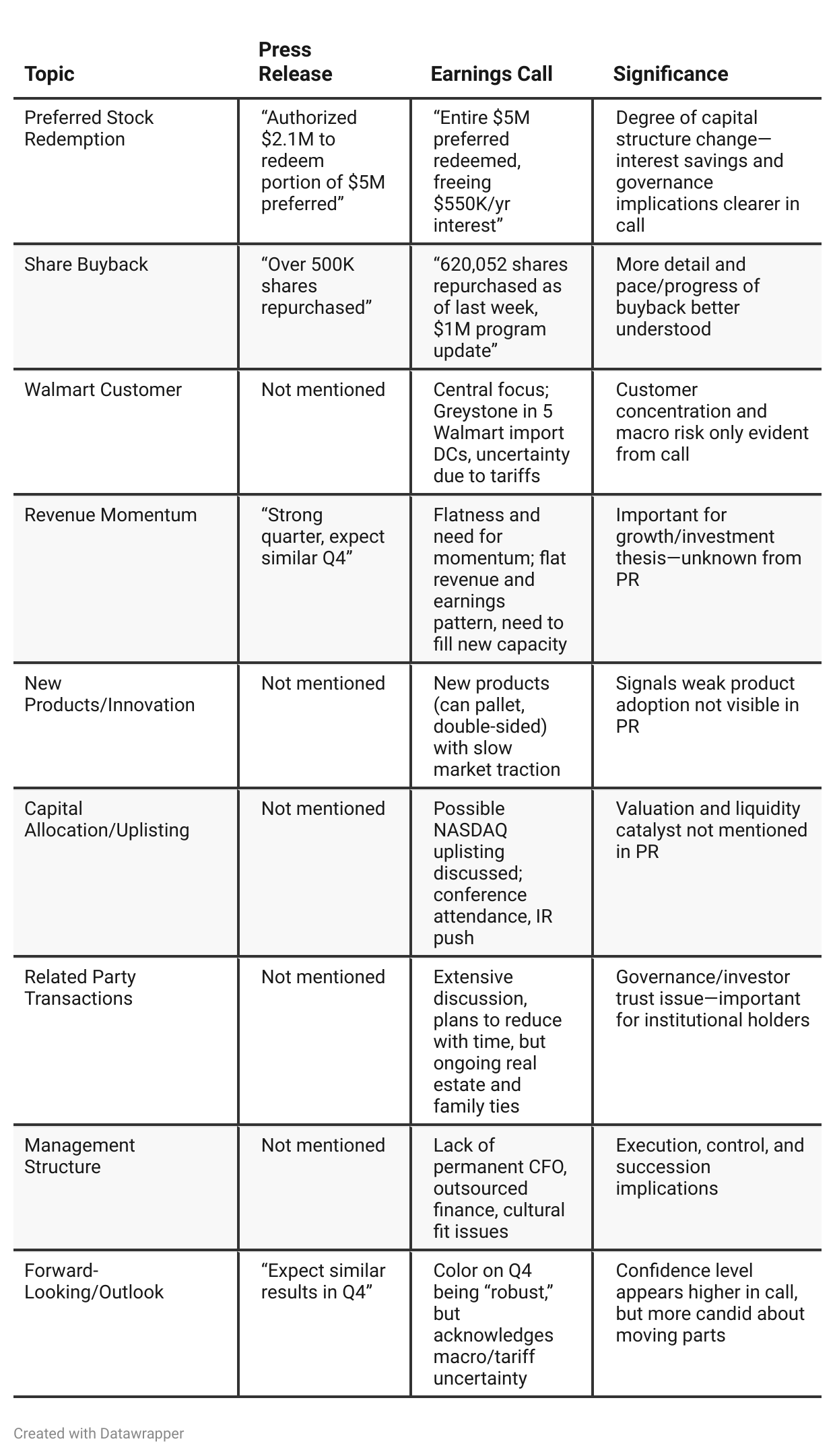

Press Release vs Call Transcript Comparison

Earnings call delivers transparency: Investors get a deeper look into management’s thinking, the actual obstacles (sales execution, product adoption), customer risk, and board/management ties.

PR is optimistic but omits challenges: Only the positive headline numbers are noted (no mention of operational problems, customer risks, or governance structure).

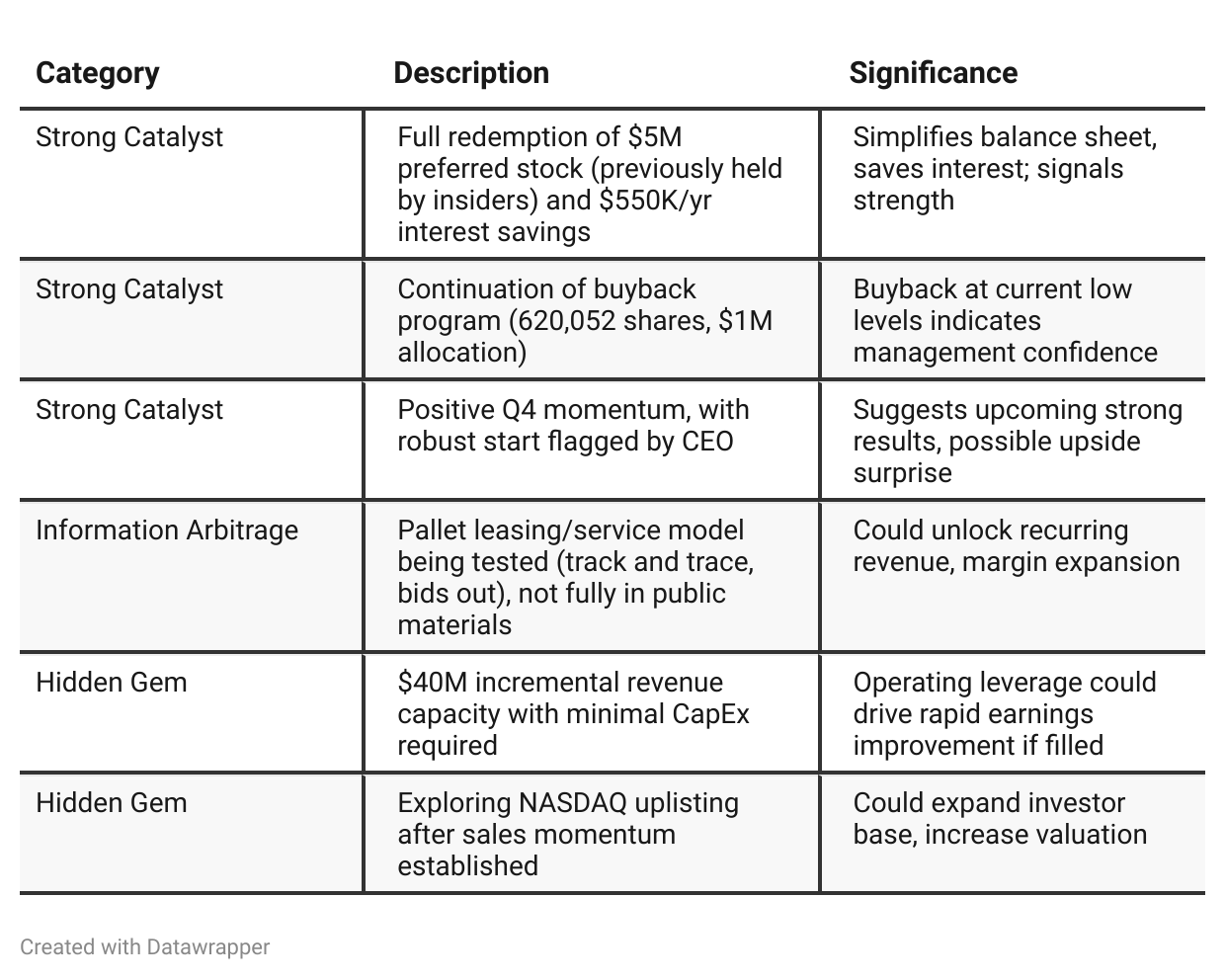

Call reveals both upside and risk in capacity: $40M+ available revenue bandwidth could mean a step-function in growth if sales accelerate, but currently represents underutilized asset risk.

Major upcoming catalysts: Faster sales ramp, success with tracking/“pallet as a service,” new products getting commercial traction, possible uplist, further reduction in related party complexity.

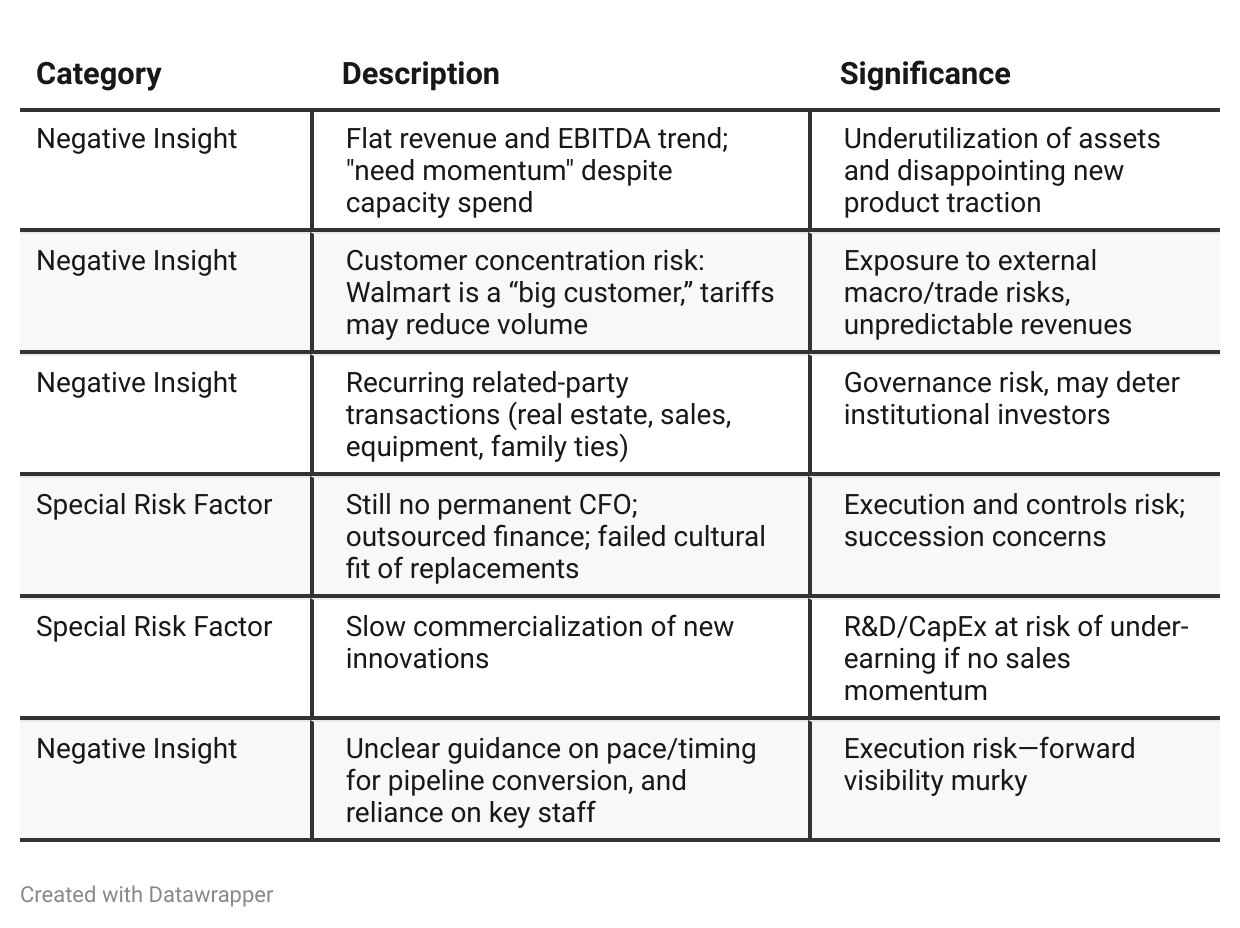

Key dependencies: Success will hinge on converting pipeline to sustained sales, managing customer concentration risk (especially macro impact on Walmart’s supply chain), and progress on professionalizing management/board structure to attract larger institutional investors.

Governance stands out: The related party nature of assets and transactions—while rooted in survival and growth—imposes limits on how the company may be perceived in terms of risk, transparency, and scalability.

Positive Insights

Negative Insights

Tariff Risk

Tariffs & Trade Policy: Tariffs and trade uncertainties ("tariff front in the past 10 days") were cited as a macro risk, primarily impacting Walmart (the company’s biggest customer due to its heavy reliance on Chinese imports). CEO is candid: "I don't know how that's going to play out for us, because we have been filling their import DCs with plastic pallets… It may slow things down, frankly. I don't know the answer to that yet."

Mitigation/Strategy: Most of Greystone's business is US-based, which the CEO frames as competitive insulation versus foreign manufacturers (“freight is the leveler”). However, there's no explicit mitigation strategy outlined beyond geographic focus.

Forward-Looking Statements: CEO expects to have a "better picture" by the next quarter, suggesting monitoring is ongoing but no current forecast on magnitude of risk.

Competitive Impact: Implies some competitive insulation from imported pallet makers but untapped risk via supply chain slowdowns at large customers such as Walmart.

Sentiment Analysis

The overall sentiment toward GLGI is neutral. While there are positive remarks about the company reducing debt, eliminating preferred shares, insider confidence, and the potential for upside with a Nasdaq uplisting, there are also notes of skepticism and hope for a price drop post-uplisting. The discussion is balanced by factual observations and mixed expectations, resulting in an overall neutral investor sentiment.

Previous Earnings Call

Quarter-over-quarter comparison

In Q2 2025, Greystone Logistics was in a cautiously optimistic, yet somewhat defensive posture—acknowledging a soft first half and delayed sales, but touting a robust pipeline, new product development, and an expanded sales push to utilize unused capacity. Messaging centered on structural tailwinds in automation and sustainability, a key long-term vision of $100M revenue, and the early stages of capital return (share buybacks) and capital structure optimization (interim CFO solution).By Q3 2025, the company’s narrative matured and became more introspective. While management celebrates the full payoff of preferred shares and ongoing buybacks as signals of financial strength, Kruger is more transparent regarding ongoing challenges: persistent revenue flatness, underutilized new machinery, and customer concentration tied to macro/tariff risk. New strategic priorities, such as tech-enabled “pallet as a service” leasing, come to the fore. Governance and related-party transparency also become bigger topics. There is a pragmatic admission that, despite momentum, real sales growth and operational leverage remain a work in progress, and management is determined to fill capacity and convert pipeline into actual earnings growth.

Year-over-year comparison

Over the course of a year from Q3 2024 to Q3 2025, Greystone Logistics’ narrative has evolved materially. The earlier call was marked by temporary distortions (Covid credits, delayed tooling), and a tone of measured optimism about resolving sales inertia through new products and salesforce expansion. As challenges persisted, the company transitioned by the next year into a phase of introspective candor: management acknowledged persistent revenue flatlining despite prior investments, implemented material capital structure improvements (buybacks, preferred redemptions), and began critically addressing customer concentration, governance issues, and the urgency of converting capacity into growth.

The storyline has matured from weathering external disruptions to a sharper focus on strategic execution—operational discipline, shareholder alignment, and the necessity of turning pipeline (“sound of silence on machinery”) into sustainable, diversified top-line momentum. The company has shifted from reacting to immediate hurdles to building the structural foundation for long-term growth but now faces the imperative of delivering on that foundation for real investor upside.

Final Takeaway

Greystone Logistics is in a stabilization/growth phase, focusing on recurring revenue models, a major customer relationship, and making better use of installed capacity. While balance sheet improvements and insider alignment are clear positives, growth execution, governance, and customer concentration remain concerns. Success will depend on translating a full pipeline and new business models into real, diversified top-line growth. Verdict: Hold, with upside if revenue momentum materializes and governance structure modernizes.