Golden Entertainment, Inc. (NASDAQ: GDEN) – Q2 2025 Earnings

Golden Entertainment, Inc. (NASDAQ: GDEN) – Q2 2025 Earnings

Earnings Release Date: Aug. 7, 2025

Stock Price: $26.90

Market Cap: $713.1 million

Q2 2025 sales of $163.6 million vs $167.3 million in the prior year

Q2 2025 EPS of $0.17 vs $0.02 in the prior year

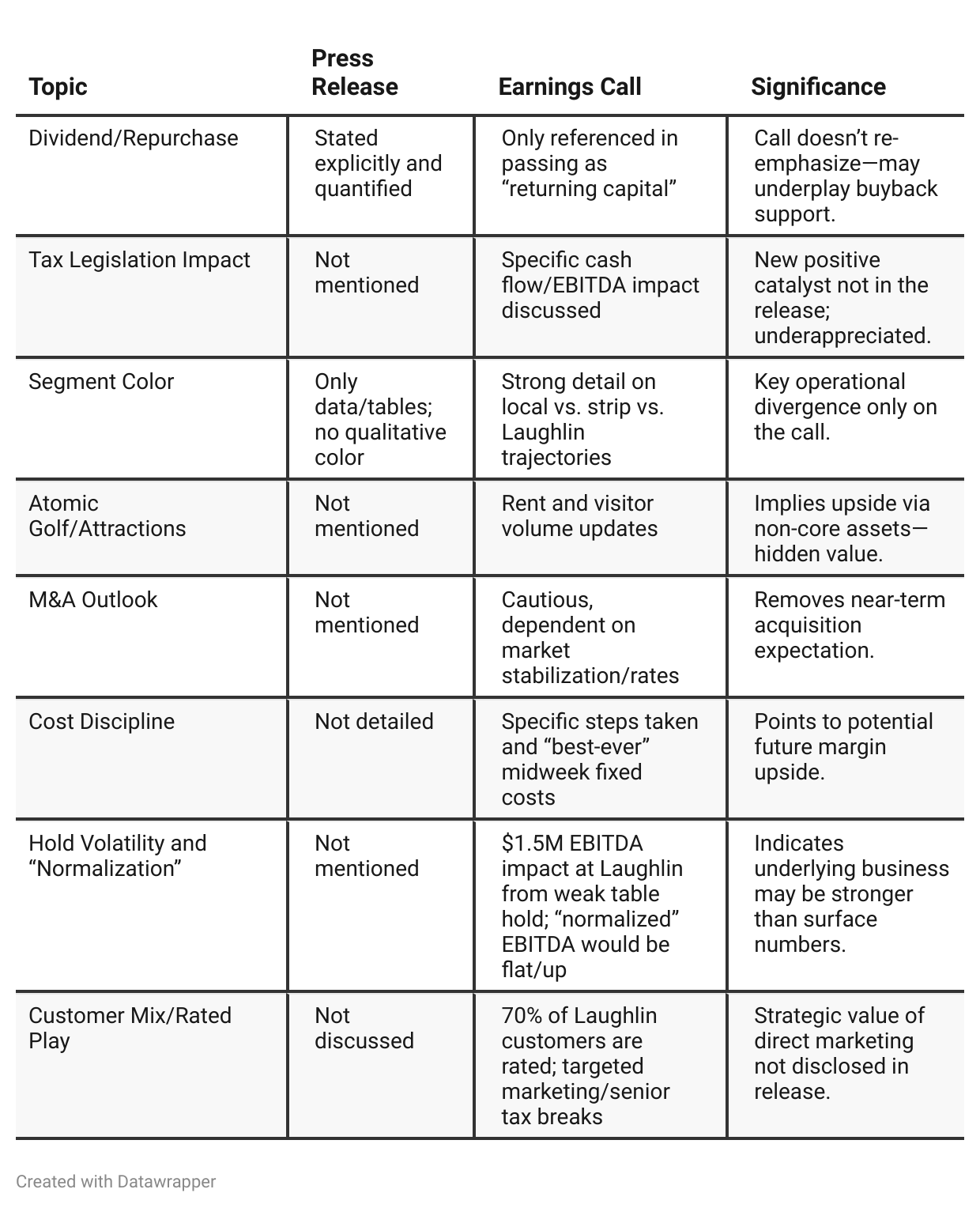

Press Release vs Call Transcript Comparison

Press Release is Backward-Looking: Focuses on past quarter, frame of reference is primarily financial/statistical.

Earnings Call Looks Forward and Explains Variance: Management talks to trends, “what’s working,” mitigating actions, and how they are proactively managing weaknesses.

Earnings Call is More Candid: Admits uncertainty (“hard to forecast” for STRAT), explains EBITDA shortfalls (hold %), and gives pragmatic expectations on timing of improvements (post-Q3).

Press Release Conceals Operational Issues: No mention of hold volatility, promotional risk, or competition, which are crucial to understanding real risks.

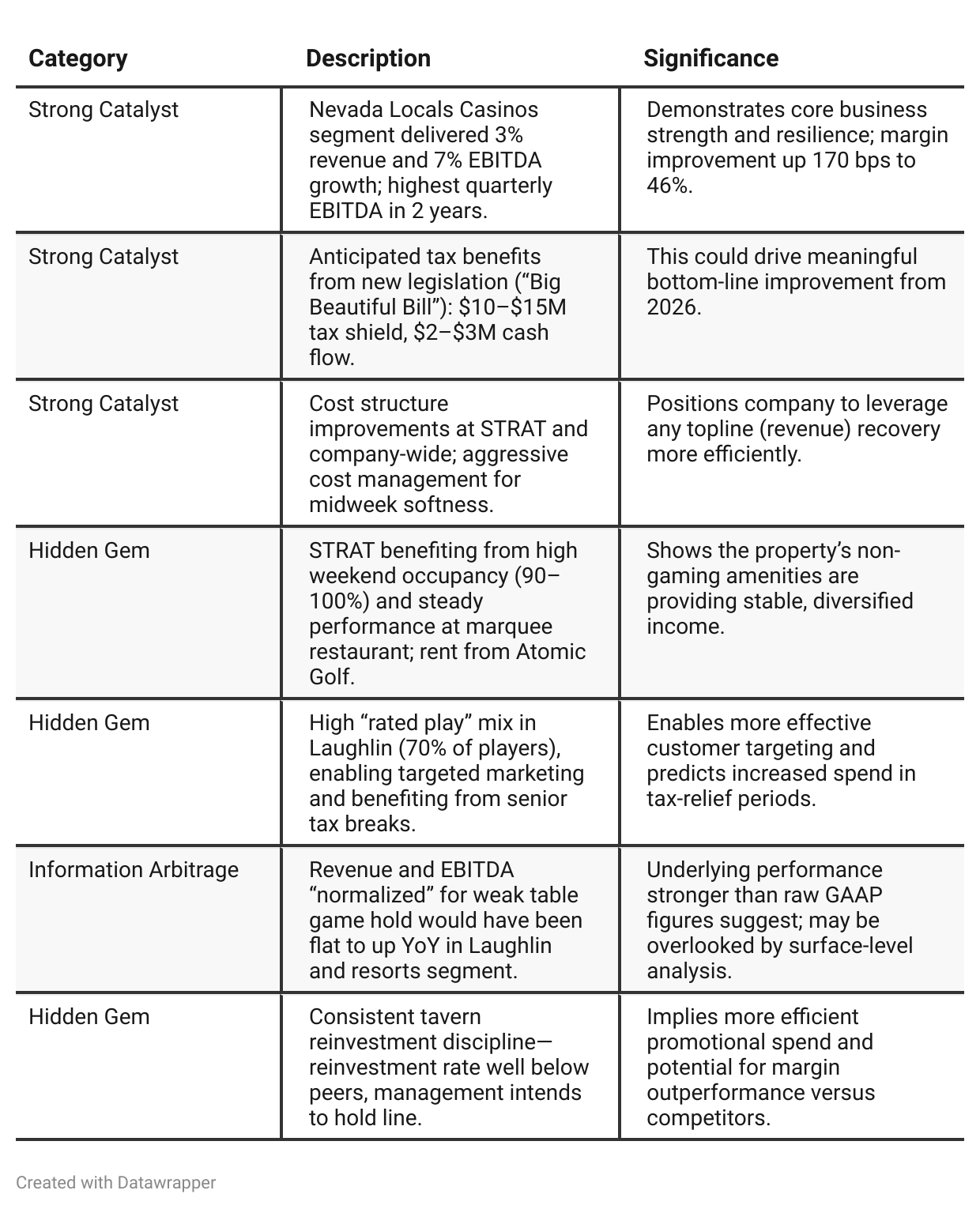

Positive Insights

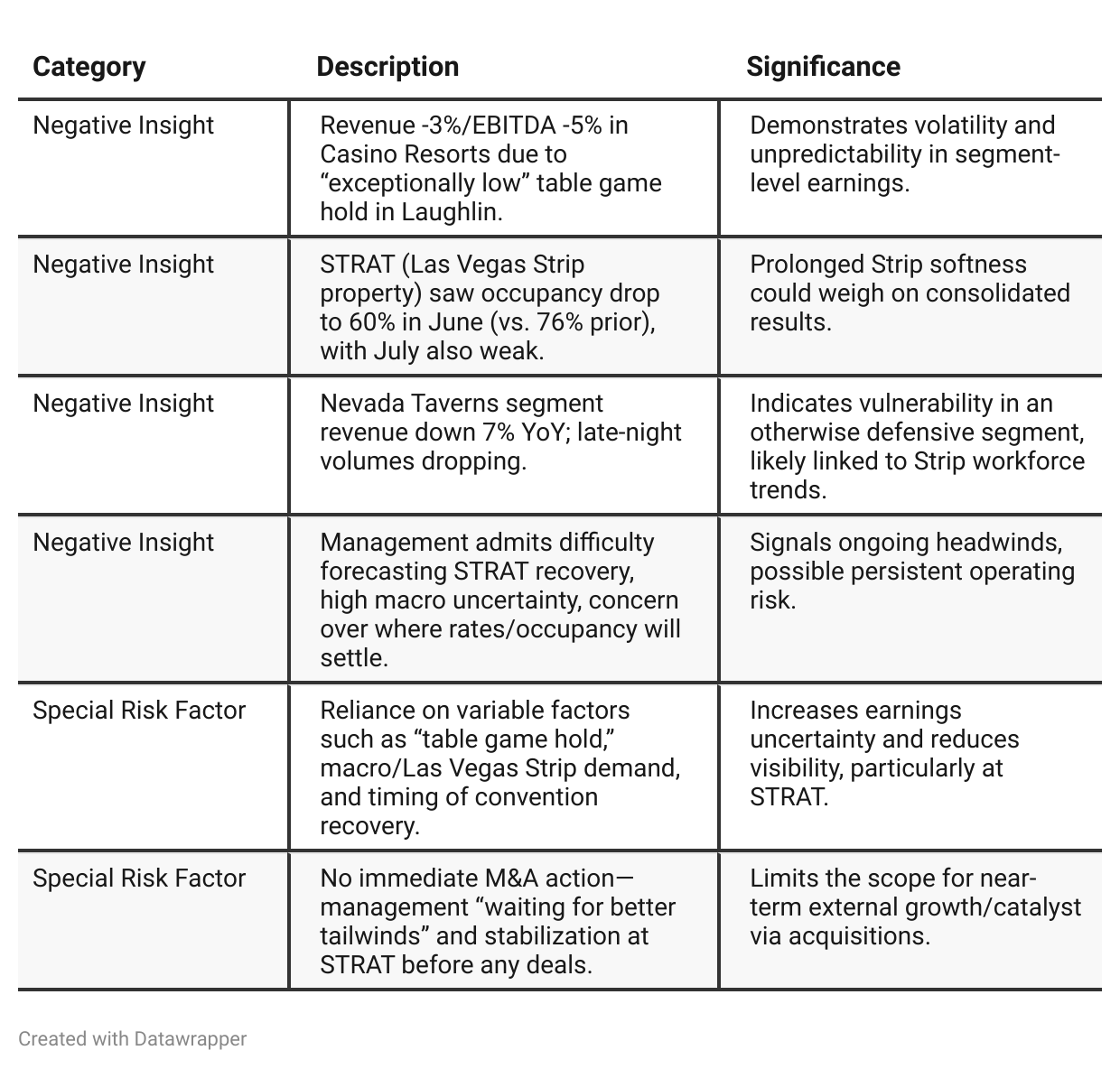

Negative Insights

Tariff Risk

Tariff Mentions: No mention of U.S. tariffs or trade policy impacts was made in this earnings call transcript.

Impact Assessment: No discussion or signal regarding supply chain issues, cost pressures, or market share risks tied to tariffs.

Mitigation/Forward Statements: Not applicable.

Previous Earnings Call

Quarter-over-quarter comparison

In Q1 2025, Golden Entertainment told the story of a company with resilient local gaming operations and a singular focus on shareholder value through capital returns, supported by a disciplined approach to costs and a bullish view on its own undervalued shares. Management appeared confident that competitive and macro disruptions were transient, that its asset base was robust, and that stabilization in STRAT would unlock further upside.By Q2 2025, the narrative had shifted to a more defensive—and realistic—tone, with management acknowledging that macro pressures and operational volatility had become tangible, especially in the Strip and tavern segments. The company highlighted its ability to blunt these headwinds through cost discipline, diversification, and forward-looking legislative catalysts (notably, tax relief measures for 2026). There’s greater transparency around uncertainty at STRAT and a clear-eyed discussion about earnings normalization versus luck-driven table hold swings. While still committed to shareholder returns, the message was less about aggressive upside and more about resilience, risk management, and preparing to capitalize on future macro tailwinds when they return.

Year-over-year comparison

Second Quarter 2024 found Golden Entertainment managing from a position of relative strength, with strong hotel and casino metrics, aggressive capital returns, and emerging opportunities in new amenities and real estate. The company’s narrative oozed with operational confidence and near-term optimism, driven by solid financial footing and the belief that pressure points (e.g., low-end weakness, promo competition) were cyclical and manageable. Real estate value monetization and falling rates were considered future levers for further upside.

By Second Quarter 2025, the tone pivots. Macro softness—especially on the Las Vegas Strip and among value-focused customers—has materialized. Management is still anchored by financial discipline and cost containment, but now speaks more defensively, emphasizing margin preservation, resilience through risk (table hold, STRAT softness), and the anticipation of legislative/tax-driven future catalysts. While shareholder returns remain a pillar, capital deployment has become more cautious, and there is less excitement about near-term asset value realization or M&A. The focus has moved from offense to defense, highlighting the company’s adaptability and preparedness for a potentially prolonged period of sectoral or macroeconomic headwinds.

Final Takeaway

Golden Entertainment is in a stabilization phase, focusing on cost management and optimizing local/regional casino assets, while weathering ongoing challenges at its Strip property and in taverns. Upcoming tax law changes offer a medium-term EBITDA and cash flow boost, but near-term growth drivers are lacking. Improvement in Las Vegas convention activity and successful margin control at STRAT could unlock upside, but investors should watch for sustained recovery signals and evidence of successful capital allocation. Verdict: HOLD, with upside if catalysts materialize as expected.