FitLife Brands (NASDAQ: FTLF) – Q2 2025 Earnings

FitLife Brands (NASDAQ: FTLF) – Q2 2025 Earnings

Earnings Release Date: Aug. 14, 2025

Stock Price: $16.22

Market Cap: $149.4 million

Q2 2025 sales of $16.1 million vs $16.9 million in the prior year

Q2 2025 EPS of $0.18 vs $0.27 in the prior year

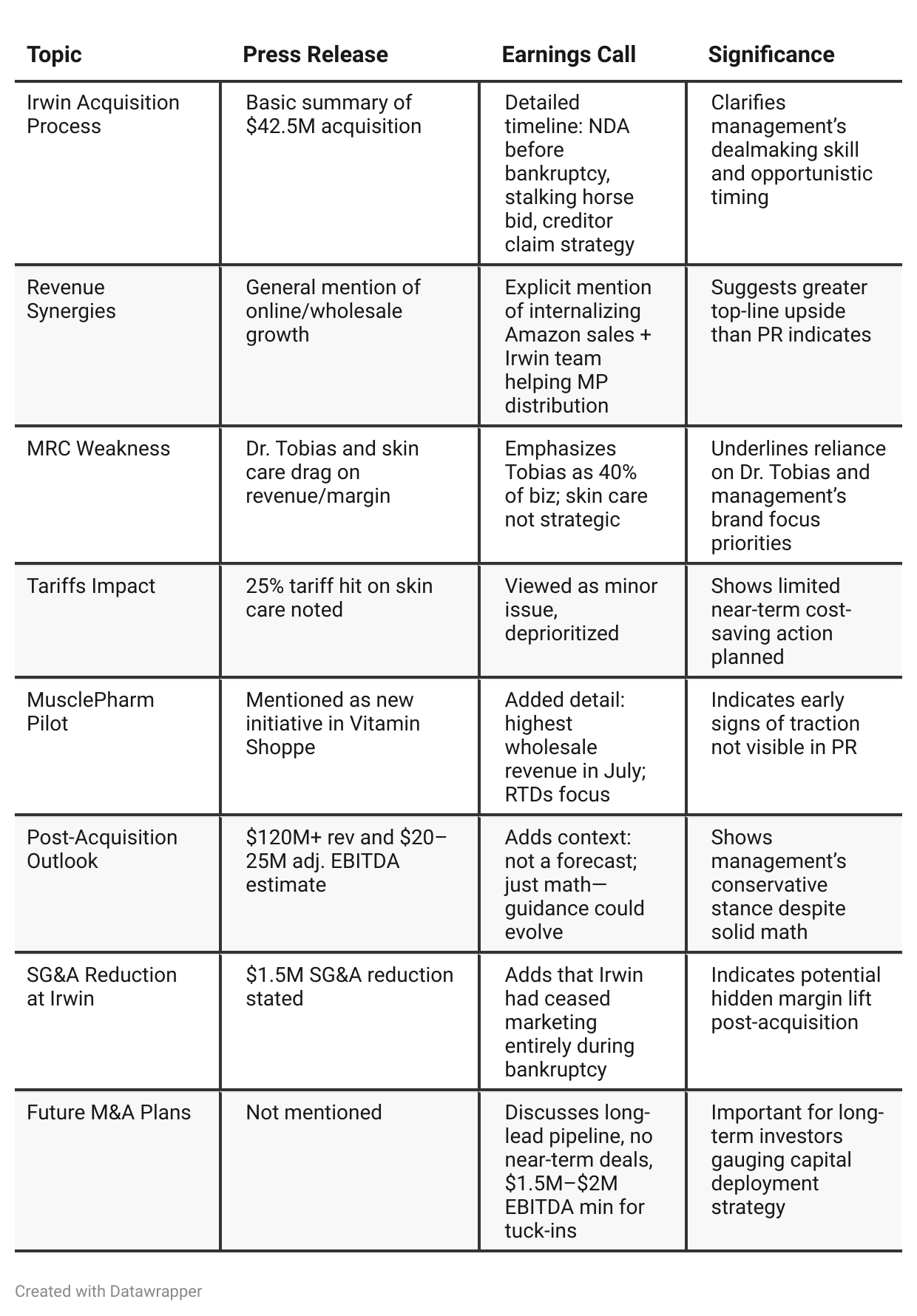

Press Release vs Call Transcript Comparison

The press release presents a surface-level snapshot emphasizing the Irwin acquisition and ongoing revenue declines, but the earnings call reveals a much more detailed—and strategically important—narrative. Management’s disciplined M&A process, clear integration priorities, and realistic tone about challenges (e.g., Dr. Tobias traffic, MusclePharm margin) show a mature leadership approach.

Investors relying solely on the press release would miss key operational levers, brand-specific risks, and revenue synergy potential. The call provides the more investable insight, especially regarding future upside from Irwin and the company’s evolving consolidation model.

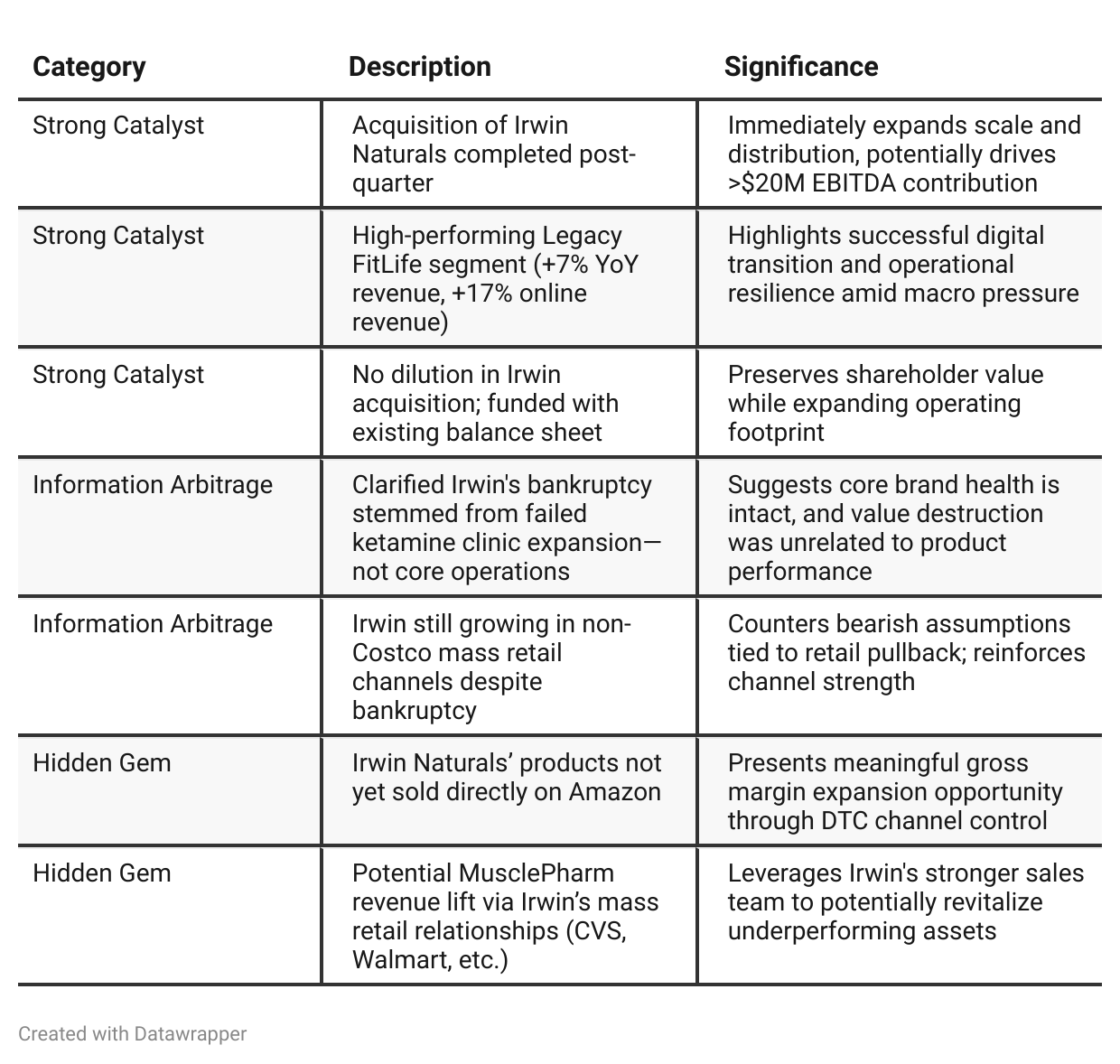

Positive Insights

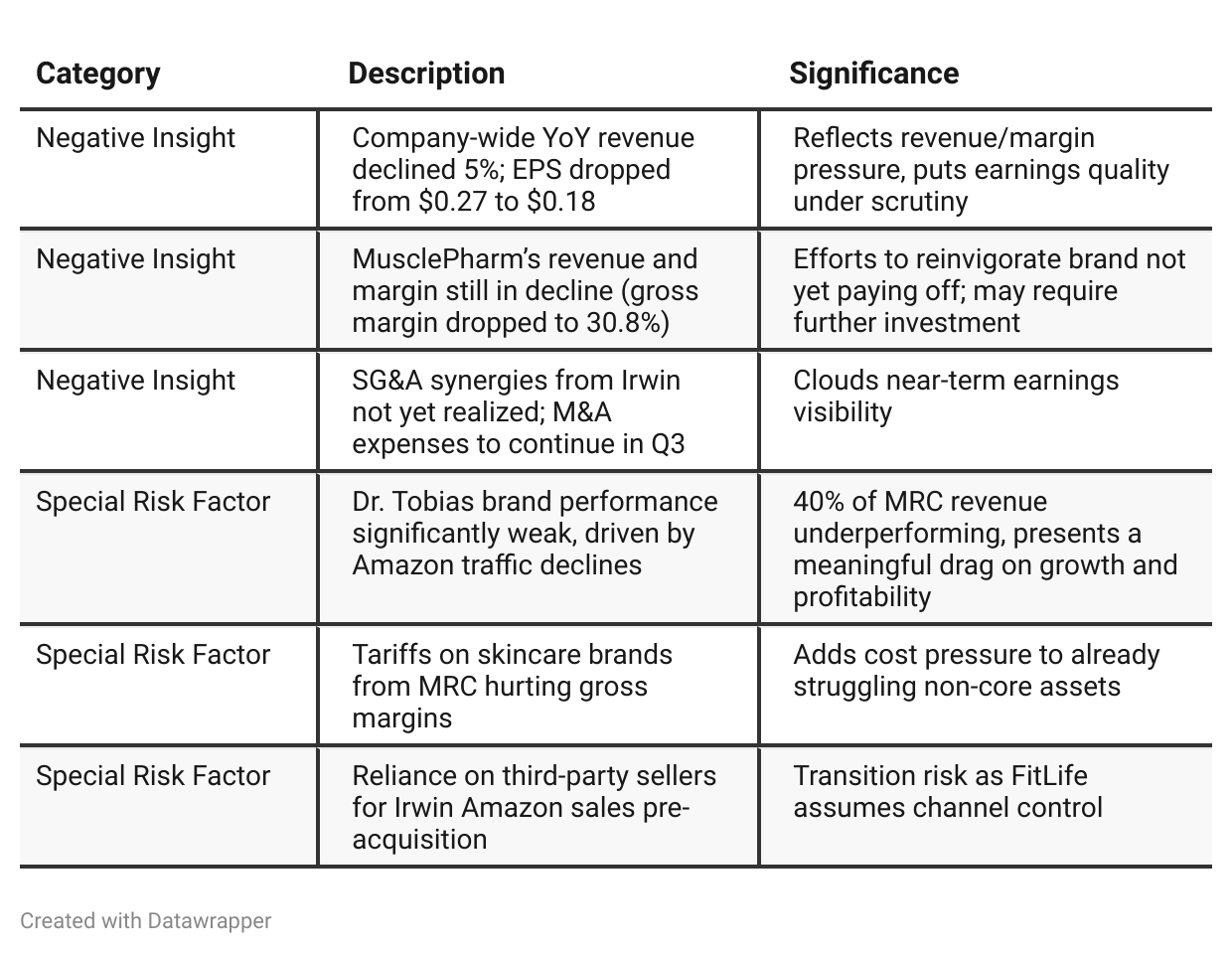

Negative Insights

Tariff Risk

Mentioned Impact: 25% tariff on MRC skincare brands imported from Florida to Canada cut gross margin for affected products by ~50%.

Magnitude: Low tens of thousands in impact; not a strategic priority for near-term.

Mitigation Potential: Possible to switch suppliers or shift production; deprioritized due to limited financial impact.

Market Effect: Tariff-induced gross margin pressure contributes to segment-level underperformance but not material enough to affect total company trajectory.

Forward Guidance: Management not assuming tariff relief; focus remains on higher-ROI initiatives like Irwin and Dr. Tobias stabilization.

Previous Earnings Call

Quarter-over-quarter comparison

Between Q1 and Q2 2025, FitLife’s narrative transitioned from stabilizing its portfolio (post-Mimi’s Rock, MusclePharm rebuild) to executing on a significant growth inflection via the Irwin Naturals acquisition. Q1 was largely defensive—fighting margin pressures, digesting prior M&A, and making promotional bets on MusclePharm.

By Q2, management had delivered on its M&A promise with Irwin and began pitching a consolidated, scalable health supplement platform targeting $120M+ revenue and $20–25M EBITDA. However, lingering challenges with MRC and the risk of integration complexity suggest a careful balancing act ahead.

The company's messaging has shifted from brand-specific optimization to portfolio-wide synergy realization, with operational discipline and Amazon traffic recovery (Dr. Tobias) as critical near-term levers.Year-over-year comparison

From Q1 to Q2 2025, FitLife's narrative shifted from fine-tuning internal brand execution and troubleshooting (MusclePharm promotions, Dr. Tobias traffic, GNC logistics) to strategic expansion and integration of a transformative acquisition.

The Q1 call was more granular and operationally focused, while Q2 adopted a higher-level strategic tone, anchored by the $60M Irwin Naturals acquisition. While MRC’s struggles persist—especially for Dr. Tobias—the overall message now leans toward scaling FitLife's platform via synergistic M&A, leveraging Irwin’s offline retail strength and FitLife’s online expertise.

Despite short-term earnings pressure from M&A expenses, the company projects a significantly enhanced financial profile going forward.

Final Takeaway

FitLife Brands is in a transformation phase, using disciplined M&A to scale revenue and EBITDA while optimizing its brand portfolio. The Irwin Naturals acquisition adds scale, synergistic retail relationships, and a high-margin DTC opportunity.

While MRC (Dr. Tobias and skincare) and MusclePharm remain problem areas, management is allocating resources pragmatically. Execution on Irwin integration and Dr. Tobias recovery will be critical to near-term performance.

Verdict: Buy, with upside contingent on smooth Irwin ramp, Dr. Tobias traffic recovery, and SG&A leverage materialization.