Firan Technology Group Corporation (OTCPK: FTGFF/FTG.TO) – Q3 2025 Earnings

Firan Technology Group Corporation (OTCPK: FTGFF/FTG.TO) – Q3 2025 Earnings

Earnings Release Date: Oct. 08, 2025

Stock Price: $11.66

Market Cap: $293.5 million

Q3 2025 sales of $47.7 million vs $43.1 million in the prior year

Q3 2025 EPS of $0.11 vs $0.11 in the prior year

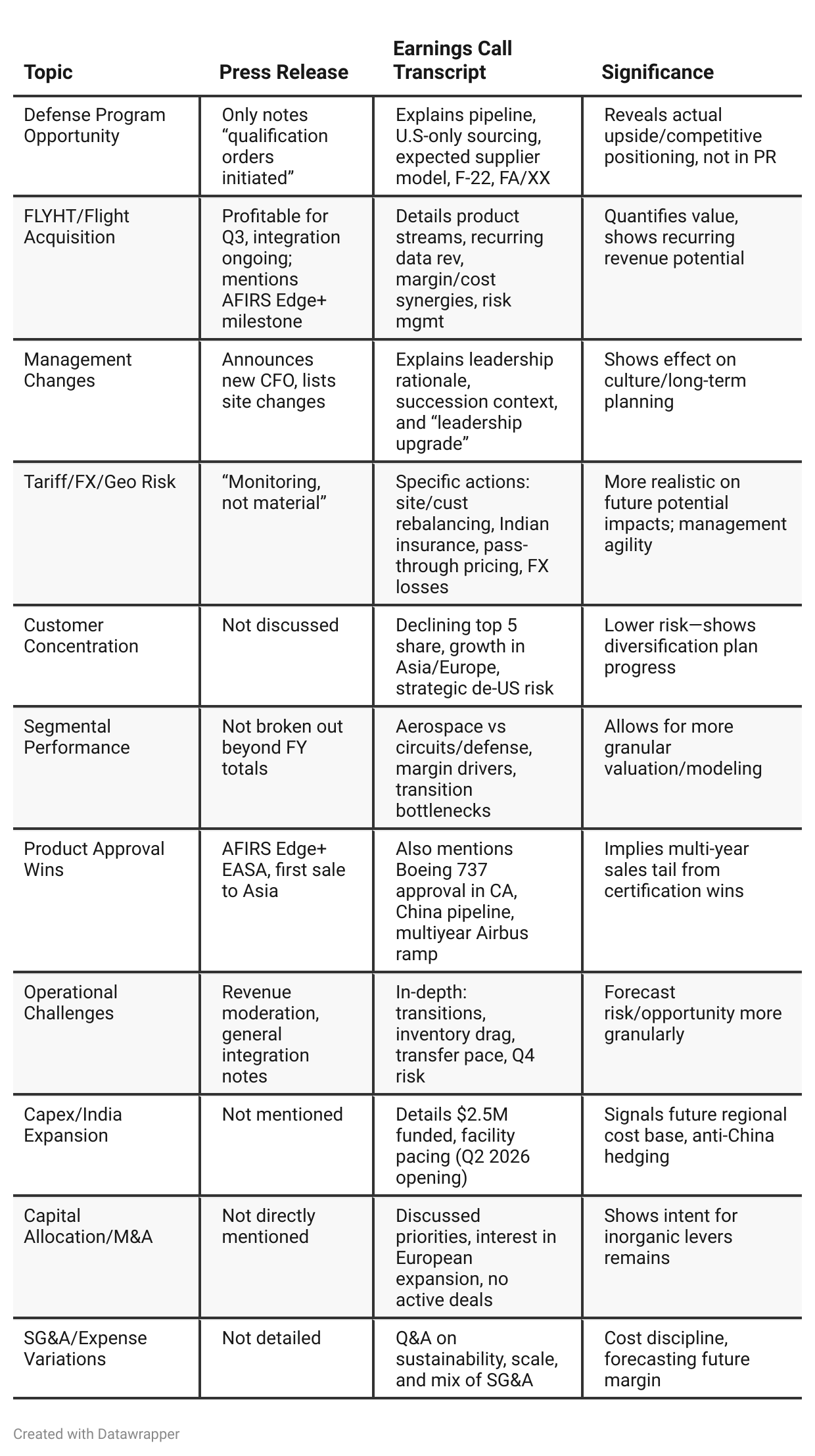

Press Release vs Call Transcript Comparison

Management Candor: The earnings call is refreshingly candid, admitting to uncertainties, transition risks, and non-smooth integration, while the press release stays positive/filtered.

Future Growth Vectors Clearer in Call: The call distinctly lays out where future growth is being built—new product ramps, global site optimization, China/India linkage, and careful risk-balancing between aerospace, defense, and regions.

Investor Guidance: The call indirectly signals that Q4/early 2026 growth may be lumpy, but foundational strength is being laid for outperformance in the medium/long-term.

Execution Risk: Execution on transitions, product qual, and customer handoffs is the key gating factor—not just demand, as implied in the press release.

Valuation Implications: The nuances in the call may justify either a higher multiple (on upside potential/optionality) or caution (on volatility and margin “lull” risks), depending on investor preference.

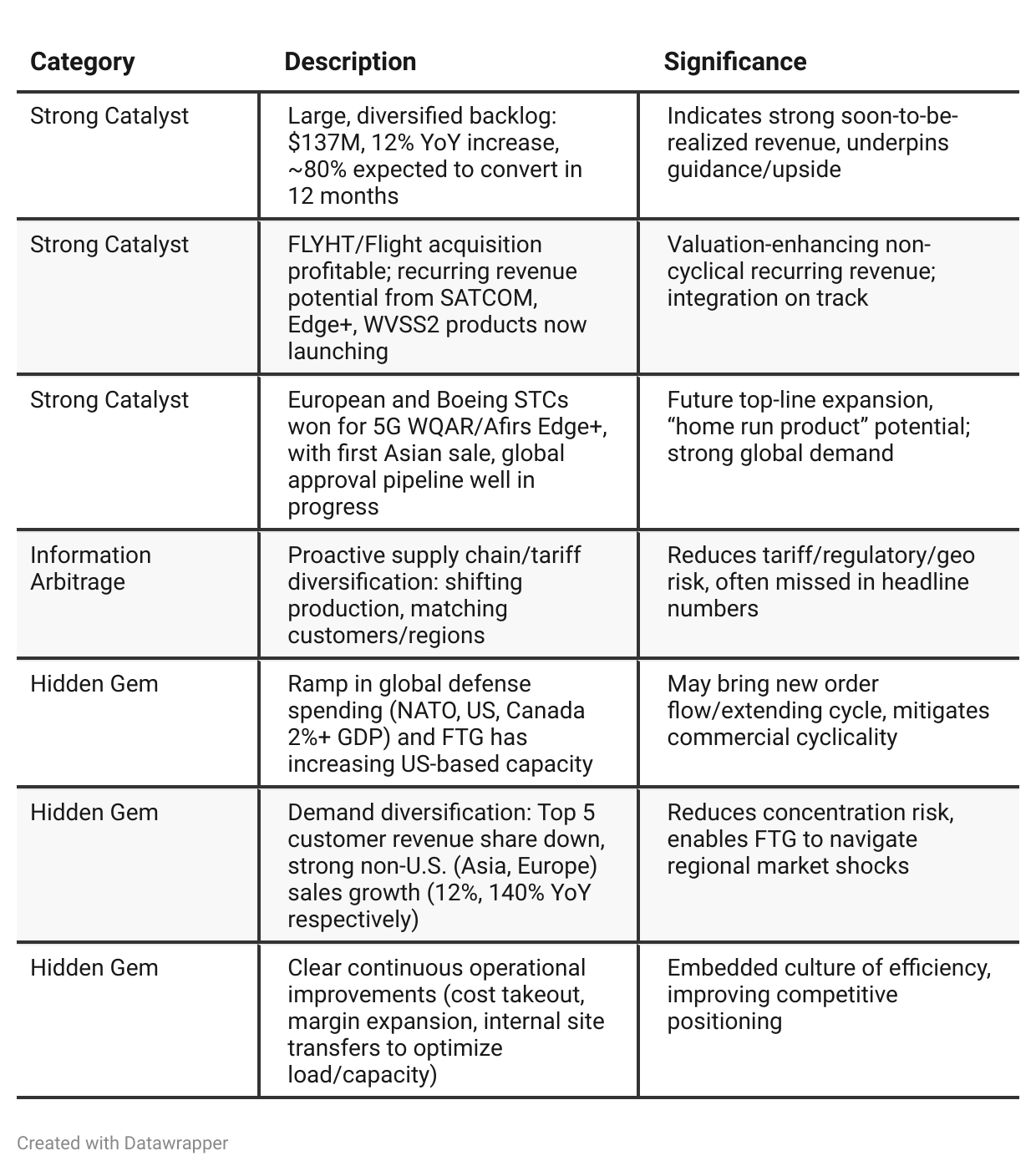

Positive Insights

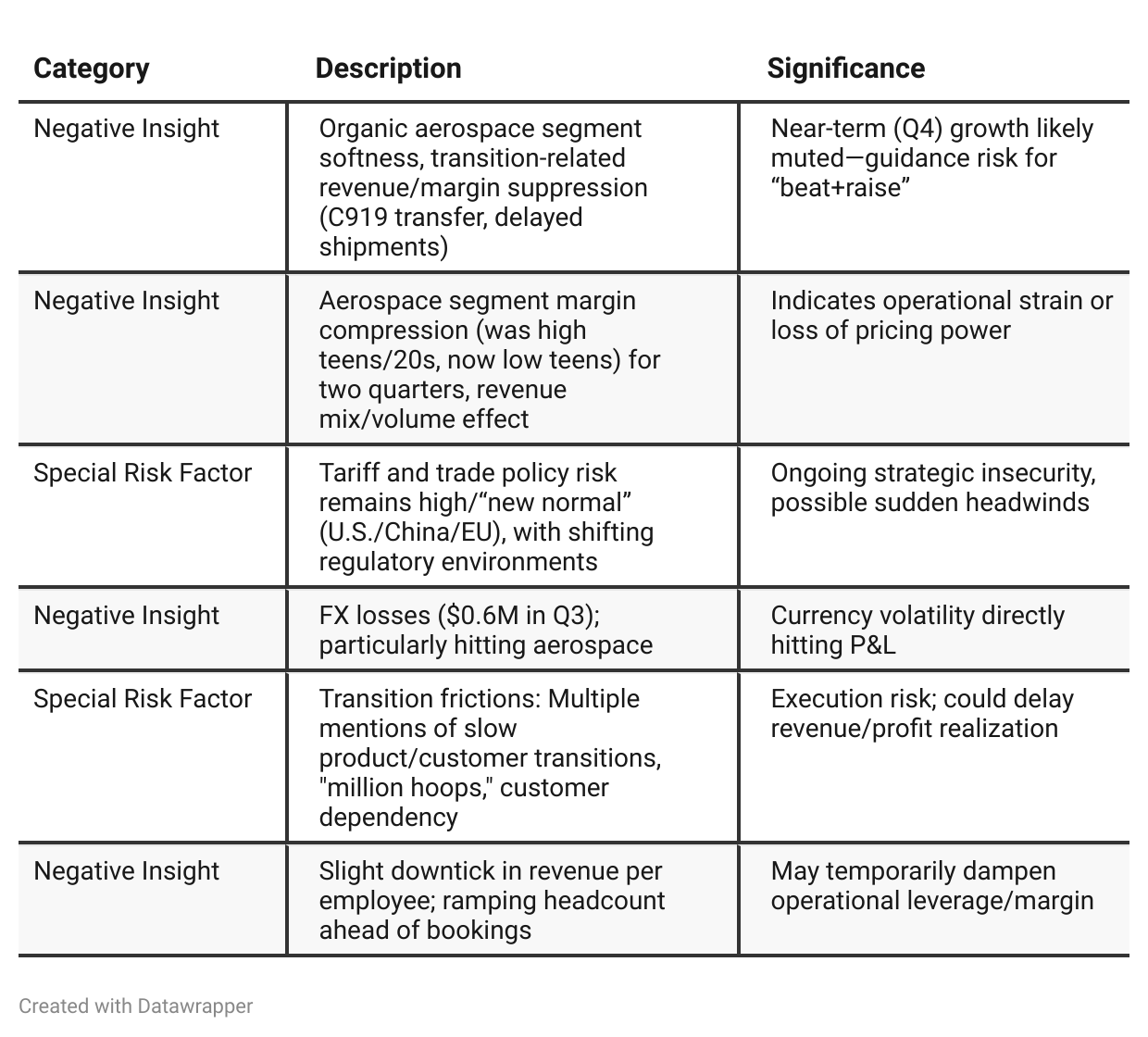

Negative Insights

Tariff Risk

Discussion: Management identifies U.S. tariffs as the “new normal,” admits high uncertainty, and details strategic actions: shifting work to match region/cust, accelerating global diversification (including into India as “insurance”), attempting to pass on input cost tariffs, refocusing Canadian sites onto non-U.S. work, and emphasizing U.S.-based production for U.S. customers.

Revenue Impact: So far “minimal” impact, but significant proportion (historically up to 55%) of U.S. sales originated from outside U.S.—a potential risk if new tariffs enacted. Europe and Asia sales growth (140%, 12% YoY) are seen as natural hedges.

Profitability Impact: Input costs in U.S. rising; passing costs onto customers where possible. Could erode margins if tariffs escalate or if customers resist. FX volatility also compounds risk.

Mitigation: Active relocation, proactive contract/customer management, investment in India, and product/customer “matching” to lower tariff/vulnerability exposure. Flight acquisition, globally diversified revenue, and pursuing Airbus over Boeing further aid strategic hedging.

Forward Outlook: Management is alert and credibly proactive, but admits rapid scenario-shift is always possible; continued monitoring required.

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Q2: FTG is riding a wave of record sales and EBITDA, integrating recent acquisitions (especially Flight) and rapidly expanding internationally (with India facility progress and surging Europe/Asia sales). The team is growing, and management is upbeat, even as they keep an eye on tariffs and supply chain risks. Market signals in commercial and defense aerospace remain strong, and FTG’s product and geographic diversification are paying off. Margins and pricing are improving (especially due to acquired sites and data-driven price optimization).Q3: The company enters a more operationally complex phase. Momentum on new products and geographies continues (certifications, bookings, leadership hires), but day-to-day execution becomes more critical. The transition of major programs (notably the C919) and production platforms is harder than expected, causing delayed shipments and muted short-term organic growth and margin compression. The company is refreshingly upfront about these challenges—prioritizing organizational depth and resilience as core leadership transitions occur. The story is now about managing through this tough, messy middle phase while keeping a long-term focus on recurring revenue, deeper customer diversification, and global risk management.

Year-over-year comparison

—

Final Takeaway

FTG is in a global expansion and operational transition phase, leveraging new product certifications, a robust order backlog, and disciplined cost management to establish itself as a broadly diversified aerospace and defense player. While demand and backlog are strong, margin headwinds and operational transitions are weighing on reported figures. Investors should monitor the pace of product/admin transition recovery, tariff risks, and evidence of margin inflection. Verdict: HOLD, with potential upside as integration and market shifts play out, but patience required for Q4–26 results.