Firan Technology Group Corporation (OTCPK: FTGFF) – Q2 2025 Earnings

Firan Technology Group Corporation (OTCPK: FTGFF) – Q2 2025 Earnings

Earnings Release Date: Jul. 8, 2025

Stock Price: $8.36

Market Cap: $208.3 million

Q2 2025 sales of $48.7 million vs $38.8 million in the prior year

Q2 2025 EPS of $0.14 vs $0.11 in the prior year

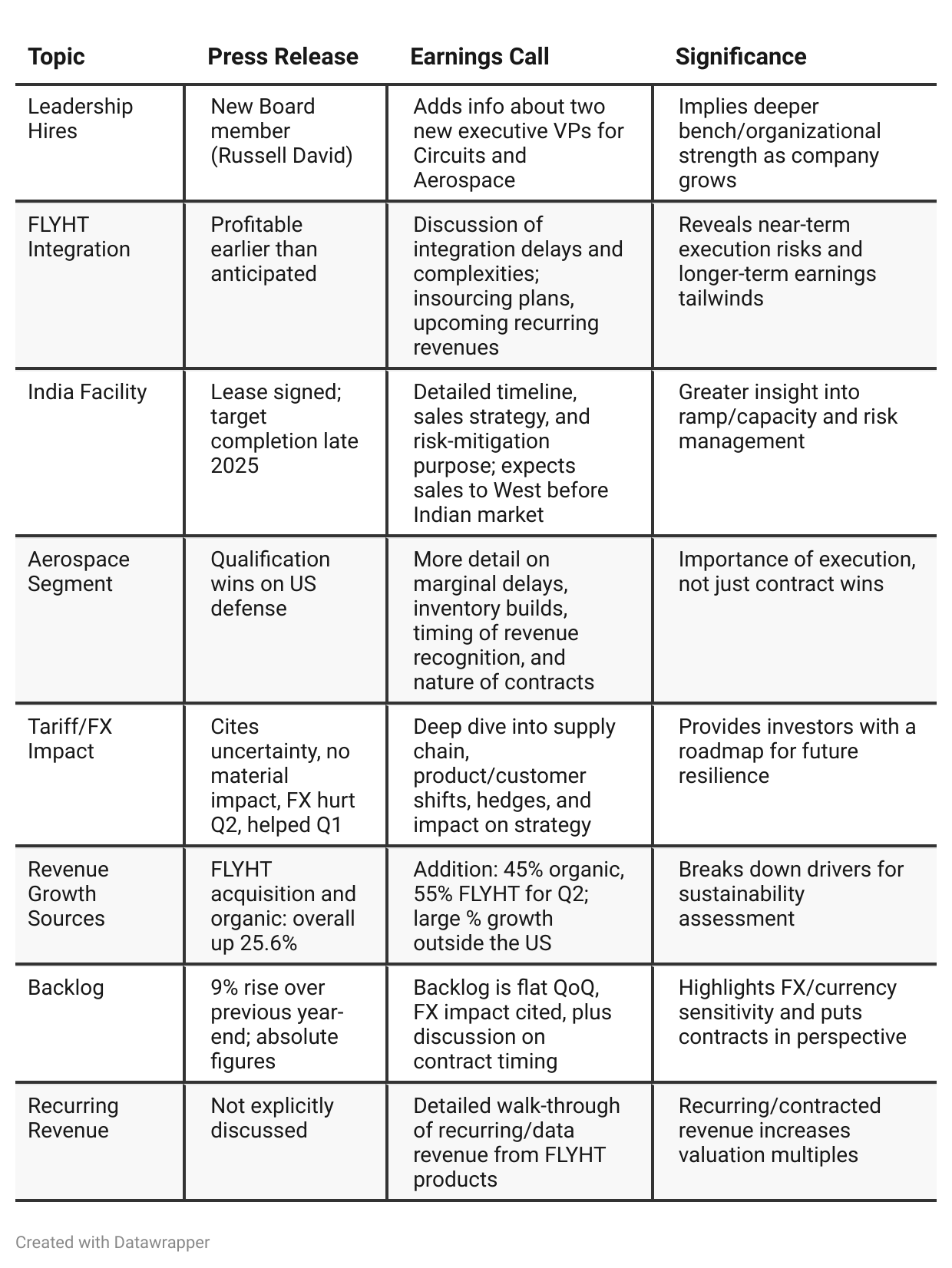

Press Release vs Call Transcript Comparison

Earnings Call has much more forward-looking color on risks and mitigations—especially tariffs, FX, and global supply chain adjustments, as well as direct commentary on their approach to new growth regions (India, Europe, Asia).

Strategic shift to ‘pivotal wave’ from the US market is a key structural change that is not explicit in the press release, but could de-risk the story for long-term holders.

Recurring revenue, SaaS and data-related services model emerging at FLYHT—could be a medium-term valuation re-rating driver.

Repatriation of profits out of China and focus on manufacturing diversification reduce tail risk; not a headline item in the press release but significant.

Inventory build tied to delayed customer qualification is a short-term negative for cash conversion but positive when resolved; the earnings call gives color on timing and potential normalization.

Operational and cost discipline is reinforced in the call; discussion of pricing opportunities and ERP-driven margin optimization at acquired sites is noteworthy for cash flow/capital returns.

Customer concentration is reducing due to diversification—a small but meaningful de-risking trend.

Simulators/defense segment ‘lumpiness’ is a management watch item not headline-worthy, but a reminder for investors expecting straight-line growth.

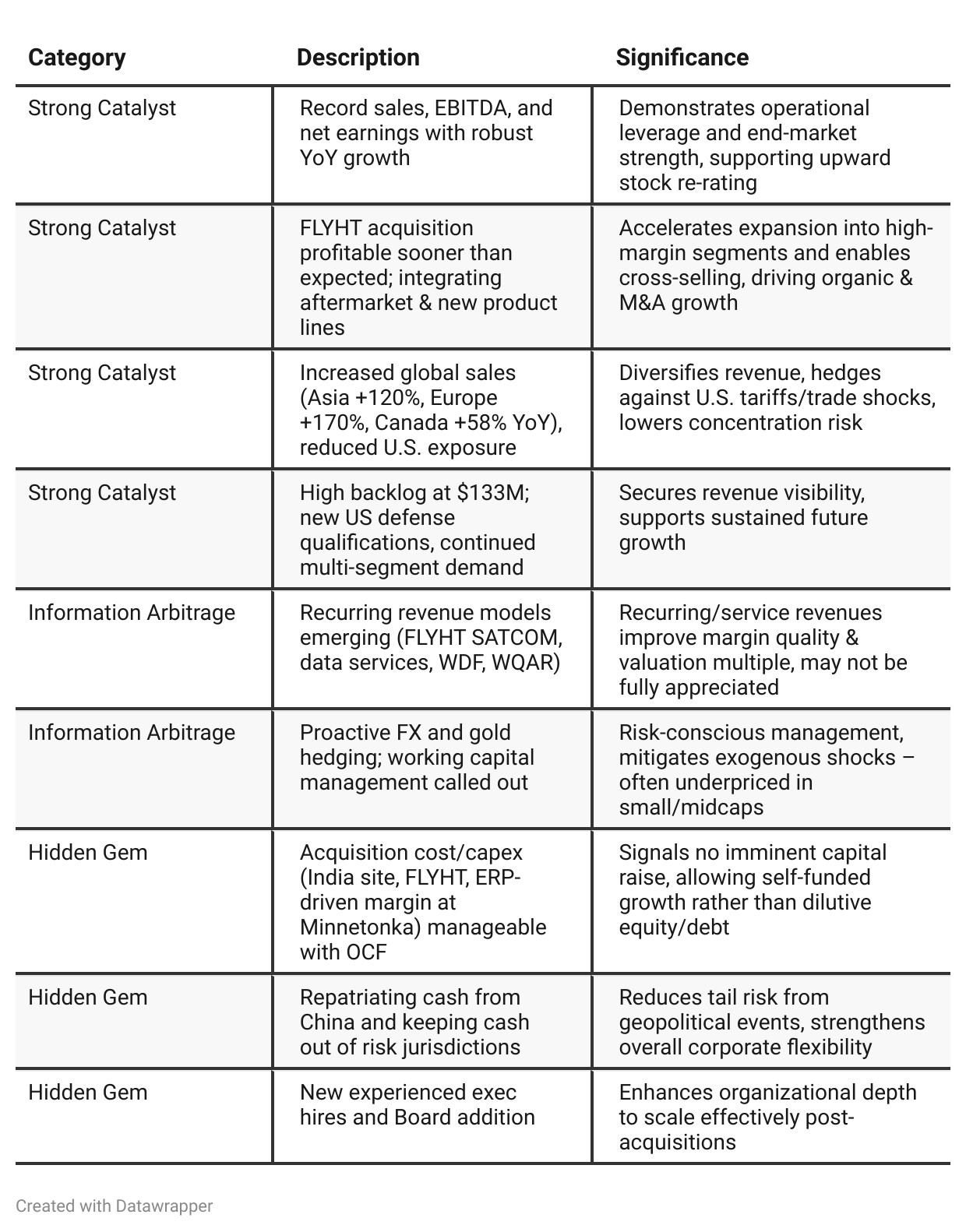

Positive Insights

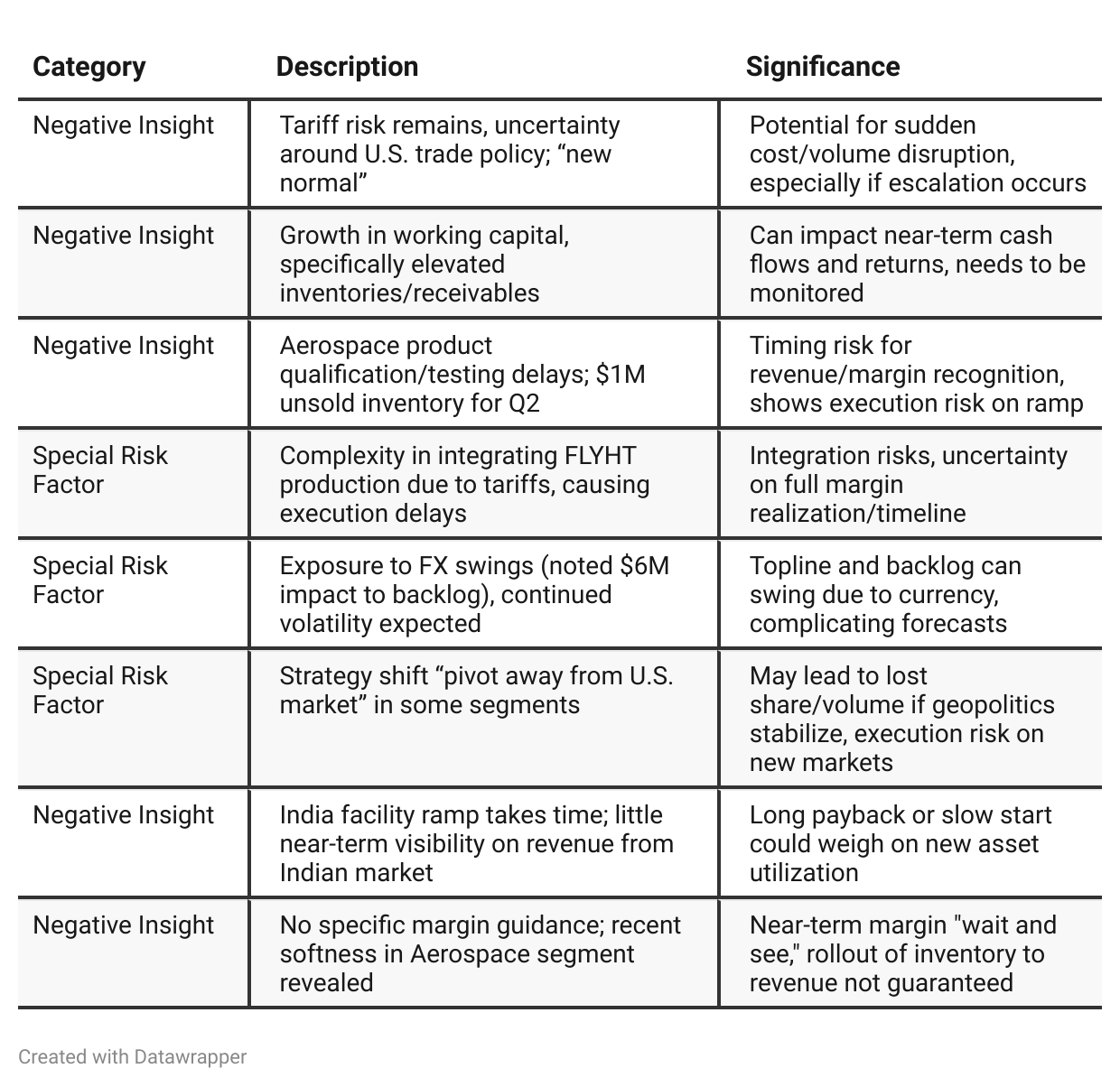

Negative Insights

Tariff Risk

FTG faces ongoing uncertainty from U.S. tariffs, especially regarding goods from China. Currently, only a small portion of their China-made products are affected, and the financial impact is minor. However, management recognizes this risk as persistent and potentially volatile.

Mitigation Actions:

Geographic Diversification: Shifting more sales and production outside the U.S. (major growth in Europe, Asia, and Canada).

Production Realignment: Relocating non-U.S. customer work outside the U.S. and increasing flexibility in supply chains.

Focus on USMCA Compliance: Canadian operations remain unaffected by tariffs for now.

Strategic Acquisitions: U.S. acquisitions reduce exposure for domestic sales.

Scenario Planning: Actively preparing for rapid policy changes.

Takeaway: Tariff risks are real but well managed for now. FTG’s operational changes and growing global footprint make it more resilient, but investors should monitor for sudden policy shifts or rising input costs.

Previous Earnings Call

Quarter-over-quarter comparison

At the start of 2025, FTG’s management celebrated record growth, successful acquisitions (notably FLYHT), and major wins in diversifying its customer base and global footprint. The company’s Q1 messaging was confident, emphasizing growth momentum, new product potential, and a strong offensive against tariff risk.By Q2, while momentum remained strong and another sales record was achieved, FTG’s story evolved. The leadership’s tone became more measured—acknowledging execution hurdles, inventory buildups, and macro volatility (especially FX). Priorities shifted to optimizing operations, integrating acquisitions (with more candor on delays and complexity), and sustaining growth while mitigating real-world risks. Strategy is now focused on consolidating recent wins, ensuring operational follow-through, and maintaining resilience amid continued external uncertainty.

Year-over-year comparison

—

Final Takeaway

FTG is in a growth and diversification phase, leveraging strong end-market demand, global expansion, and successful acquisitions to drive top- and bottom-line momentum. While emerging recurring revenue streams, operational discipline, and expanded geographic reach are attractive, investors should watch for evidence of integration, margin normalization, and tariff-related resilience. Ongoing execution and external risk management will determine whether the positive trajectory holds. Verdict: Hold (with Positive Bias), with upside on successful risk navigation and operational follow-through.