Flexible Solutions International (NYSE: FSI) – Q2 2025 Earnings

Flexible Solutions International (NYSE: FSI) – Q2 2025 Earnings

Earnings Release Date: Aug. 14, 2025

Stock Price: $7.55

Market Cap: $95.0 million

Q2 2025 sales of $11.4 million vs $10.5 million in the prior year

Q2 2025 EPS of $0.16 vs $0.10 in the prior year

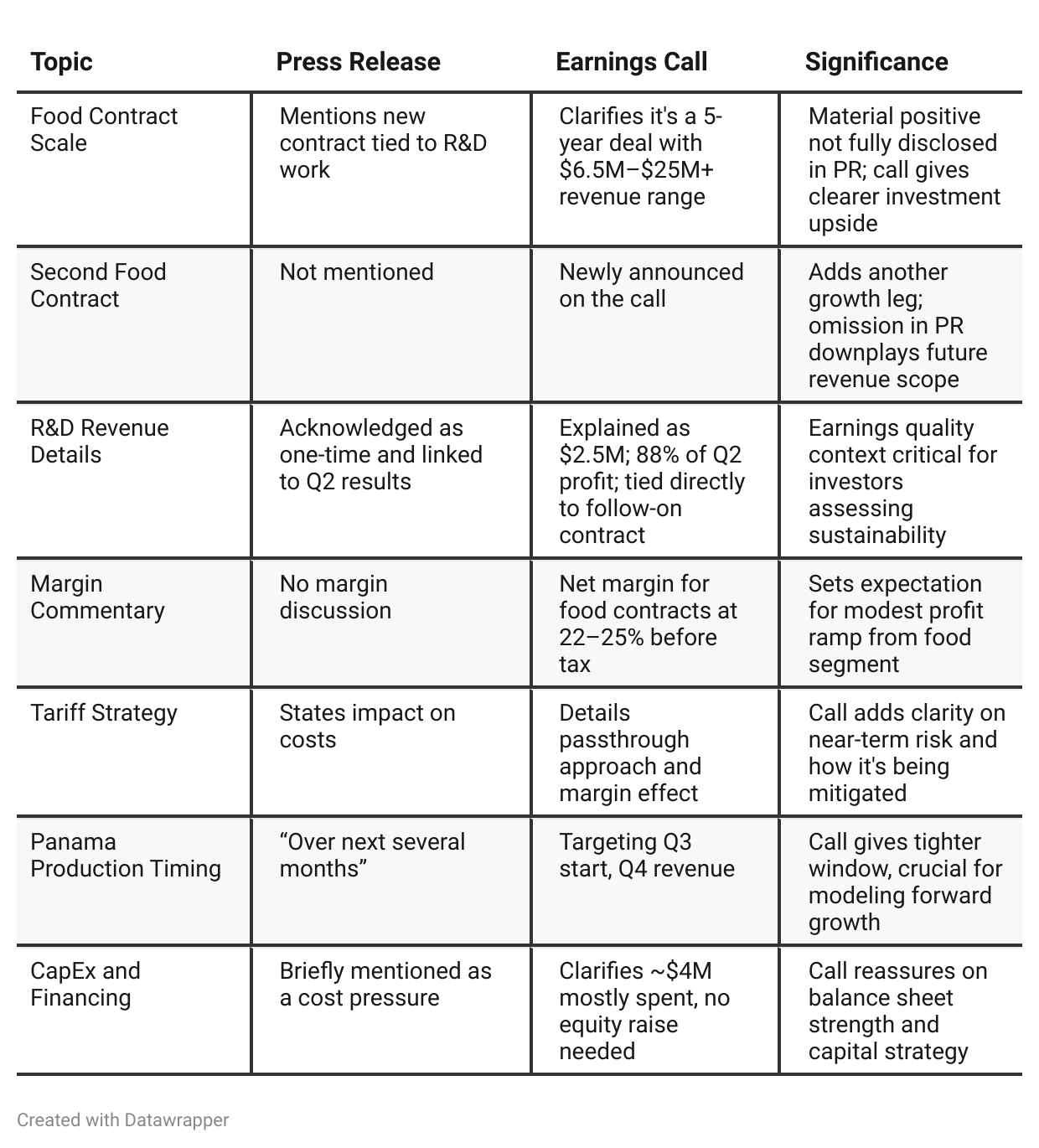

Press Release vs Call Transcript Comparison

The press release provides a high-level financial snapshot, highlighting a strong quarter driven by R&D revenue and the strategic Panama transition. However, the earnings call reveals the true depth of the story: two large-scale food-grade contracts with revenue potential exceeding $30M annually, margin and capacity nuances, and clarity on R&D monetization.

The disparity in disclosure—particularly around the second food contract and detailed revenue expectations—means that investors relying solely on the press release may significantly underappreciate the growth opportunity and execution risk. For investors, the earnings call paints a far more dynamic and nuanced picture of both the upside and challenges.

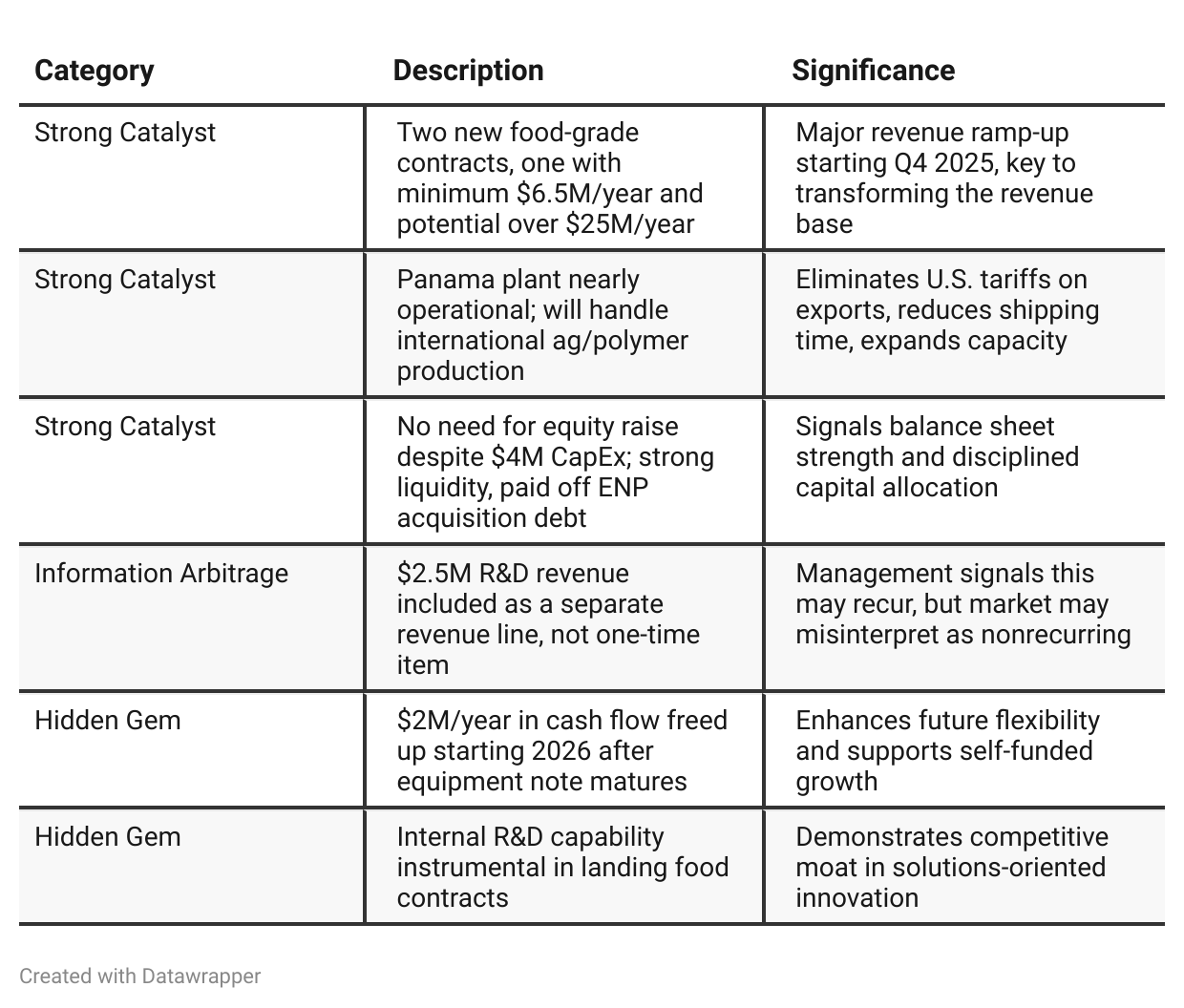

Positive Insights

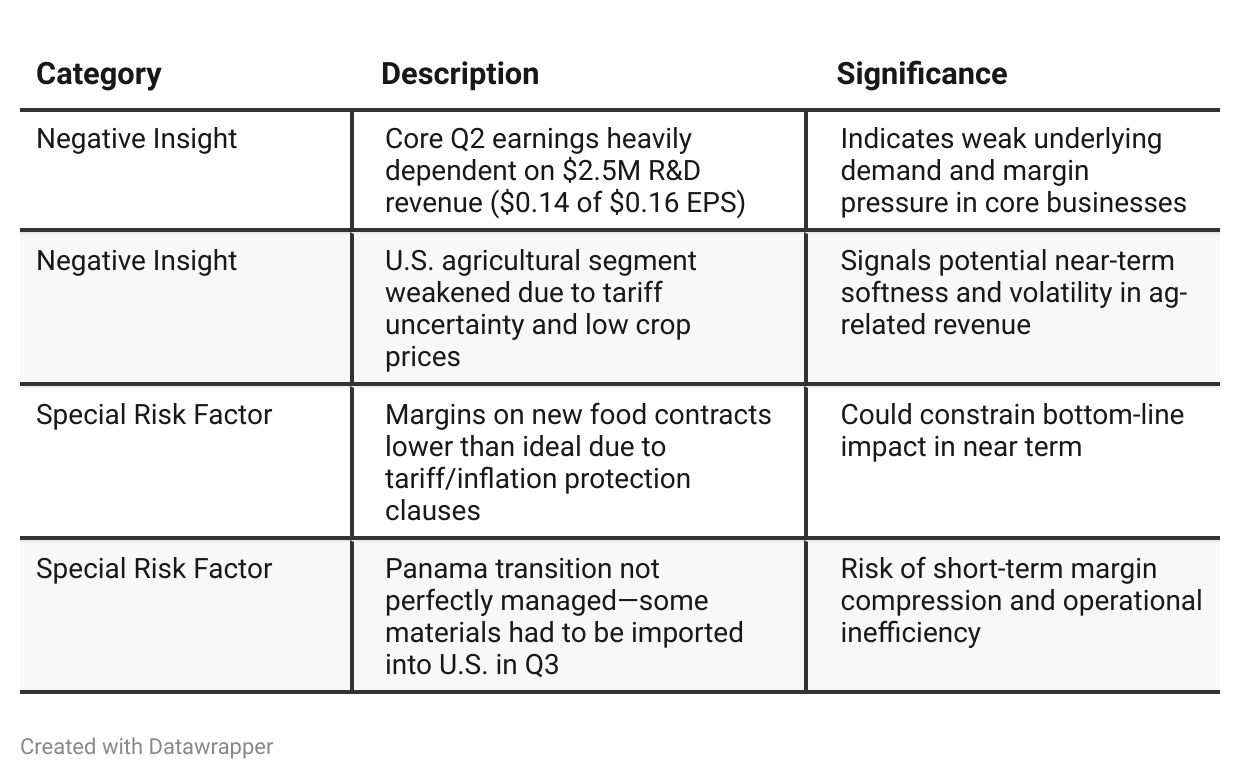

Negative Insights

Tariff Risk

Current Impact: Raw materials from China face U.S. tariffs between 30–58%. Management confirmed some materials still imported in Q3, which could reduce margins slightly.

Mitigation Actions:

Developing Panama facility to fully handle international ag/polymer sales.

Tariff/inflation protection clauses in new food contracts.

Transition plan underway despite imperfect execution.

Strategic Impact:

Panama will eliminate tariff impact on exports.

U.S. customers will absorb future tariff-related costs.

Outlook: Short-term margin pressure likely through Q3, but medium-term margin improvement expected post-Panama transition.

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

From Q1 to Q2 2025, Flexible Solutions International’s narrative evolved from building the infrastructure for a high-stakes growth opportunity to entering the execution and revenue realization phase.

In Q1, the company emphasized CapEx needs, logistical hurdles, and the uncertainty of revenue timing. By Q2, tone shifted to confidence—with equipment on site, customers engaged, and first revenue potentially materializing in Q4.

Management framed the company as lean, prepared, and de-risked, with upside tied to disciplined execution. The Panama plant, a secondary theme in Q1, became a strategic lever in Q2 for both competitive positioning and freeing up U.S. capacity. Overall, the narrative matured from strategic setup to tactical delivery.Year-over-year comparison

Flexible Solutions has transitioned from speculative positioning (emerging food-grade opportunities, potential drug line) in Q2 2024 to one of measurable contract execution and operational focus in Q2 2025.

The company now anchors its growth story around two substantial food-grade contracts, clear capacity planning (Illinois for food, Panama for ag/polymer), and tariff-mitigation strategies.

While core agricultural markets remain challenged, management has demonstrated adaptability by securing stable, high-visibility revenue streams and building infrastructure to support their growth.

Final Takeaway

Flexible Solutions is in a transformation phase, pivoting from traditional ag and oilfield polymers to food-grade, contract-based manufacturing. With two significant food contracts and a nearly complete Panama plant to reduce tariff exposure and free up U.S. capacity, the growth trajectory is compelling.

While near-term results are flattered by a one-time R&D payment, the medium-term story is one of margin expansion and scale. Execution on the food-grade production ramp and Panama transition is critical.

Verdict: Buy (Speculative), with upside contingent on Q4 ramp and sustained contract performance.