FlexShopper, Inc. (NASDAQ: FPAY) – Q3 2024 Earnings

FlexShopper, Inc. (NASDAQ: FPAY) – Q3 2024 Earnings

Earnings Release Date: Nov. 14, 2024

Stock Price: $1.29

Market Cap: $27.7 million

Q3 2024 sales of $38.6 million vs $31.4 million in the prior year

Q3 2024 EPS of $0.05 vs ($0.01) in the prior year

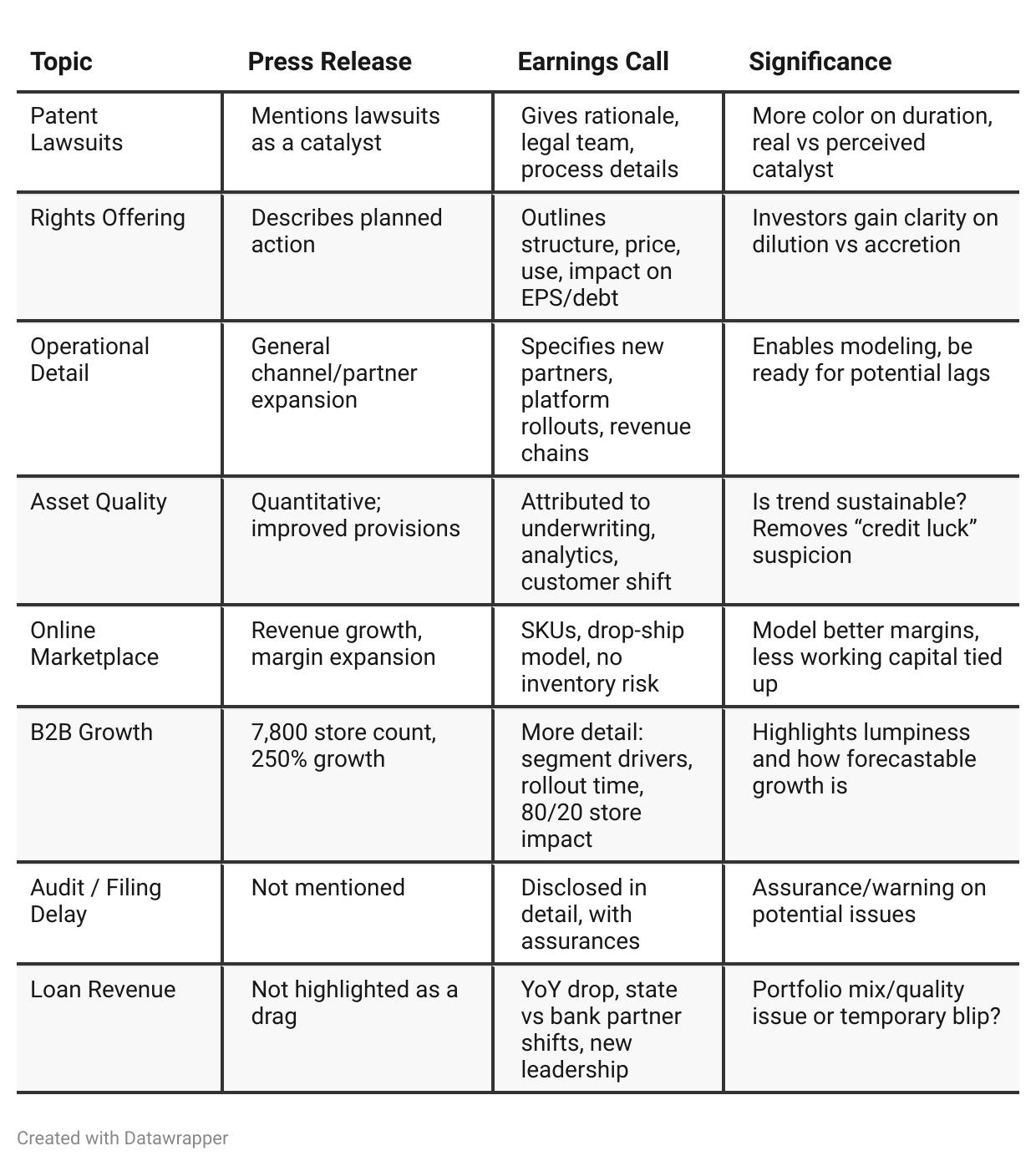

Press Release vs Call Transcript Comparison

Press Release is sanitized/optimized for positive investor perception. The call adds the “how”, lays out execution/operational timelines, and discusses challenges/open issues.

Key themes for investors: FlexShopper is in a period of potentially lumpy but explosive growth, with improved profit margins—but continues to face execution, competitive, and external risk factors.

Transformation is genuine, with credible YoY/sequence improvement, but certain revenue/cost lines (loans) are under pressure or require further strategic pivots.

Capital structure simplification is a positive—but only if growth continues and dilution is managed vs. promised accretion.

Audit/timing risk: Not a huge red flag yet, but worth noting for those with higher governance sensitivity.

New growth drivers (AI servicing, product categories, high-credit-class payment products) can be catalysts—if executed.

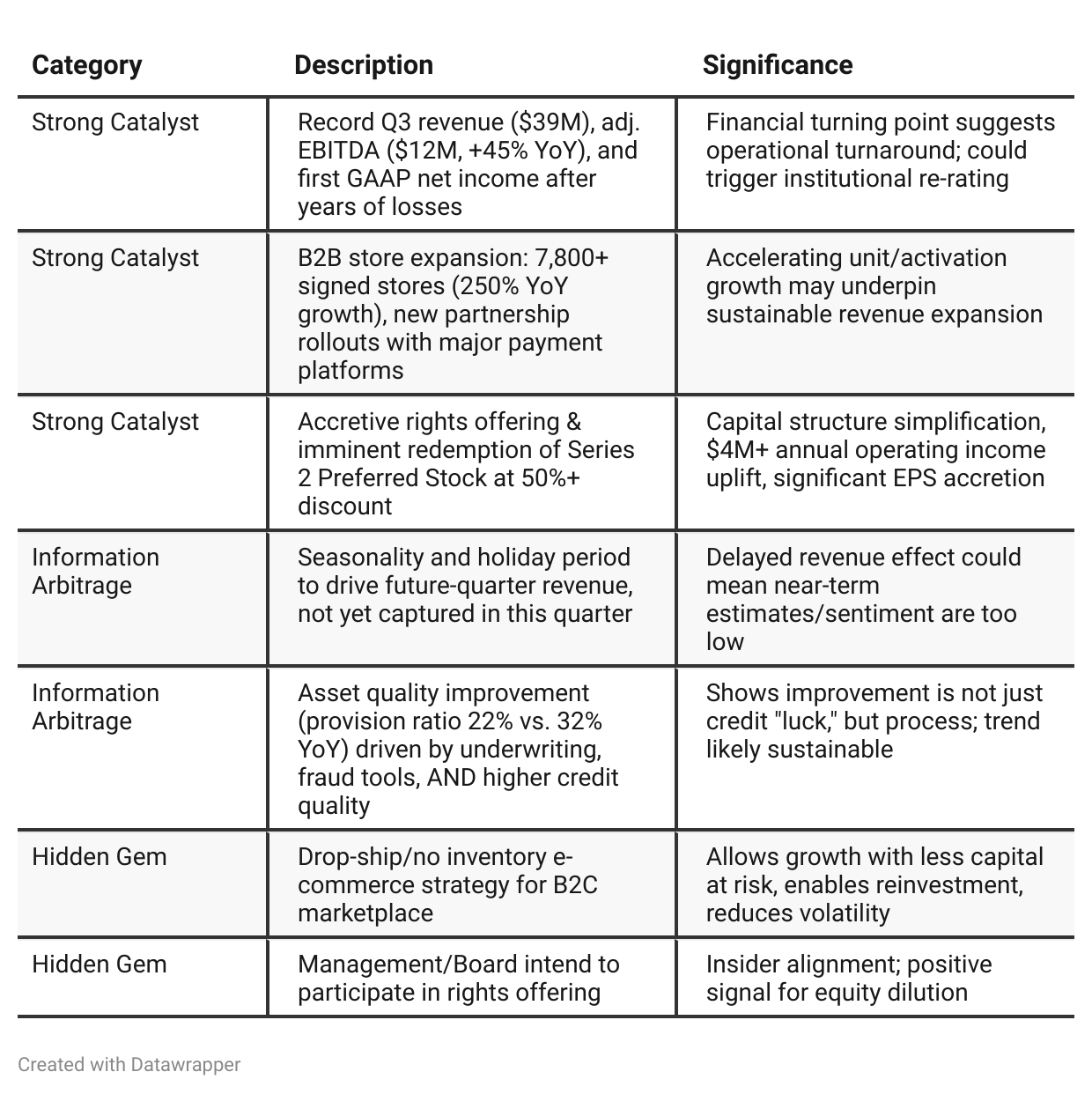

Positive Insights

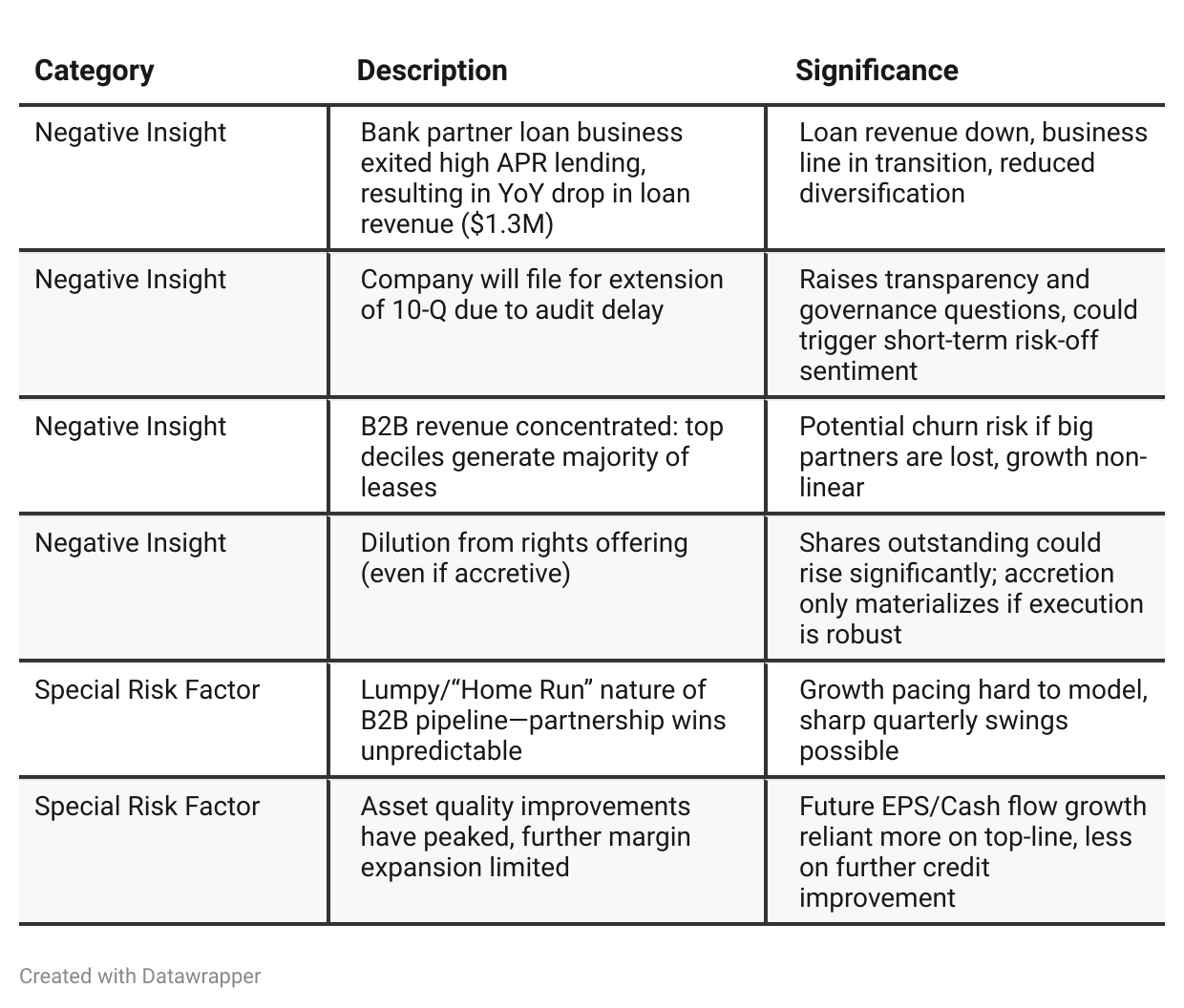

Negative Insights

Tariff Risk

Tariffs/Trade Policy Discussion: No mentions of U.S. tariffs, international trade disputes, or direct/indirect impacts from trade policy were found in the transcript. The company did not discuss input/COGS volatility, supply chain disruptions, or mitigation strategies tied to tariffs. FlexShopper’s product sourcing—primarily via drop-shipping from U.S.-based distributors and manufacturers—may limit direct exposure, but this remains unmentioned/unstated. For supply chain risk assessment, further diligence via 10-K “Risk Factors” disclosures or investor Q&A would be prudent.

Sentiment Analysis

No tweets expressed sentiment about FPAY. The overall sentiment classification is neutral due to lack of investor opinion.

Previous Earnings Call

Quarter-over-quarter comparison

Q2 2024: FlexShopper is executing on its multi-channel fintech retail strategy, expanding digitally and with traditional partners, investing heavily in technology and product breadth, and highlighting improved asset quality. The tone is one of diligent progress, recovery from pandemic-era headwinds, and setting the stage for growth.Q3 2024: The company signals a full pivot from strategy execution to scale, profitability, and defensive moat. FlexShopper touts record results, rapid expansion in retail footprint, and transformative corporate actions (preferred redemption, rights offering). There’s a greater sense of confidence and momentum, with the company also going on the offensive via patent litigation and hinting at further “home run” growth opportunities. Macro concerns fade as strong execution and competitive advantages are stressed. The step-up in priorities—capital structure, legal/IP, clear profitability—suggests a company moving from “scrappy digital growth story” to “mature, structurally advantaged fintech.”

Year-over-year comparison

In late 2023, FlexShopper’s story was about getting through macro adversity, stabilizing asset quality, and gradually executing a multi-channel, technology-driven expansion. Messaging reflected caution, attention to risk, and steady progress. By late 2024, the narrative transforms to one of acceleration and offense—marked by record-breaking performance, store count explosions, and a major capital structure shakeup described as “highly accretive.” Instead of reacting to external shocks, FlexShopper is now actively shaping its competitive landscape, leveraging a larger footprint, and delivering GAAP profitability. The language shifts from “surviving and stabilizing” to “winning and leading.”

Final Takeaway

FlexShopper is in a growth and structural improvement phase, propelled by record revenue, strong operating leverage, and meaningful capital structure actions (preferred redemption, rights offering). Management is credibly executing on strategic partnerships and technology/product expansion, while showing discipline in asset quality. Key upside comes from B2B channel expansion and improved credit performance, but success hinges on executing the rights offering and sustaining new partnership momentum. Risks are mainly deal/filing execution, dilution, and revenue concentration. Investors should monitor results from the upcoming holiday season, 10-Q filing, and rights offering close. Verdict: Buy, with strong near-term catalysts but require close attention to execution and regulatory filings.