Frequency Electronics, Inc. (NASDAQ: FEIM) – Q4 2025 Earnings

Frequency Electronics, Inc. (NASDAQ: FEIM) – Q4 2025 Earnings

Earnings Release Date: Jul. 10, 2025

Stock Price: $22.75

Market Cap: $219.1 million

Q4 2025 sales of $20.0 million vs $15.6 million in the prior year

Q4 2025 EPS of $0.34 vs $0.28 in the prior year

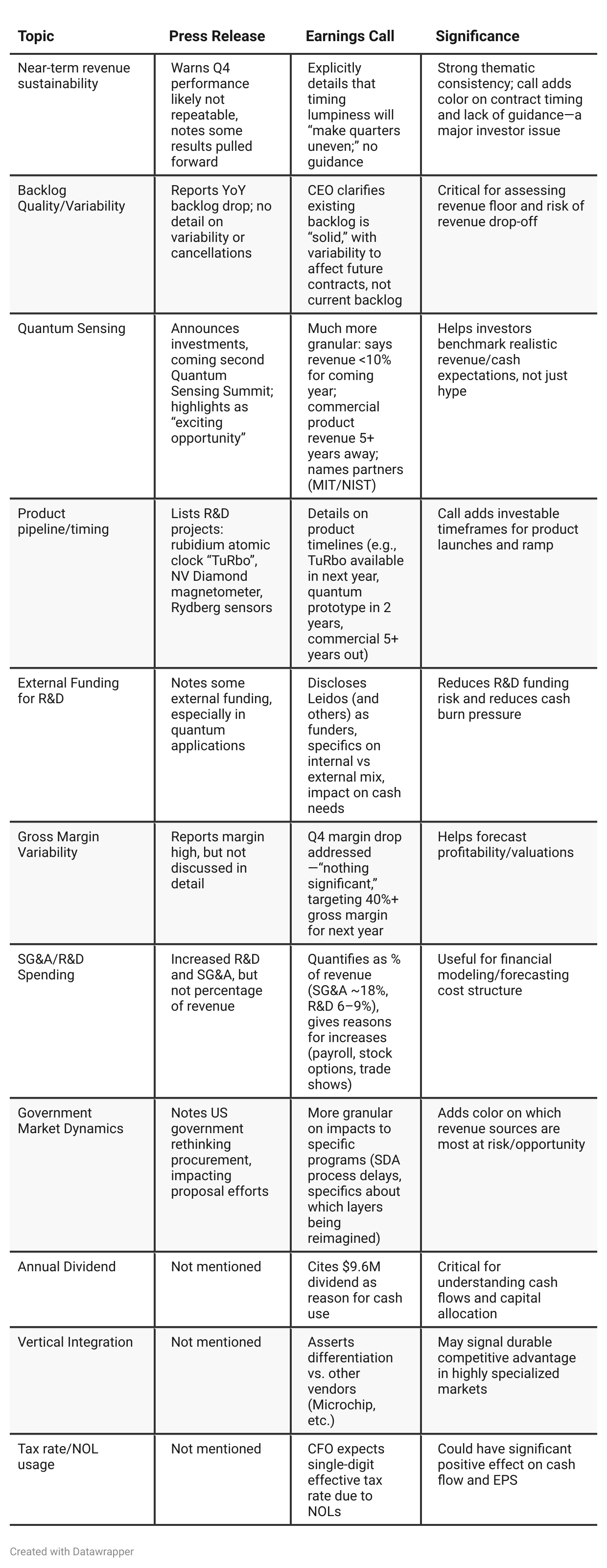

Press Release vs Call Transcript Comparison

Backlog Decline: While revenue hit record highs, backlog declined. The call clarified existing backlog is stable, but future order timing is uncertain—watch for new contract wins.

Cash Usage: Negative operating cash flow in FY25 was driven mostly by a large dividend, not operational weakness. Core liquidity and a debt-free balance sheet remain strong.

R&D Funding: R&D growth is largely supported by external partners, reducing pressure on cash and risk of shareholder dilution.

Quarterly Volatility: Both documents signal variability ahead, but the call emphasizes there won’t be regular repeat “record” quarters, so investors should expect fluctuations.

Quantum Revenue Timing: New product launches are coming, but meaningful quantum sensing revenue is years away. Don’t over-expect near-term impact.

Management Candor: The call reflects prudent, transparent leadership—actively managing investor expectations.

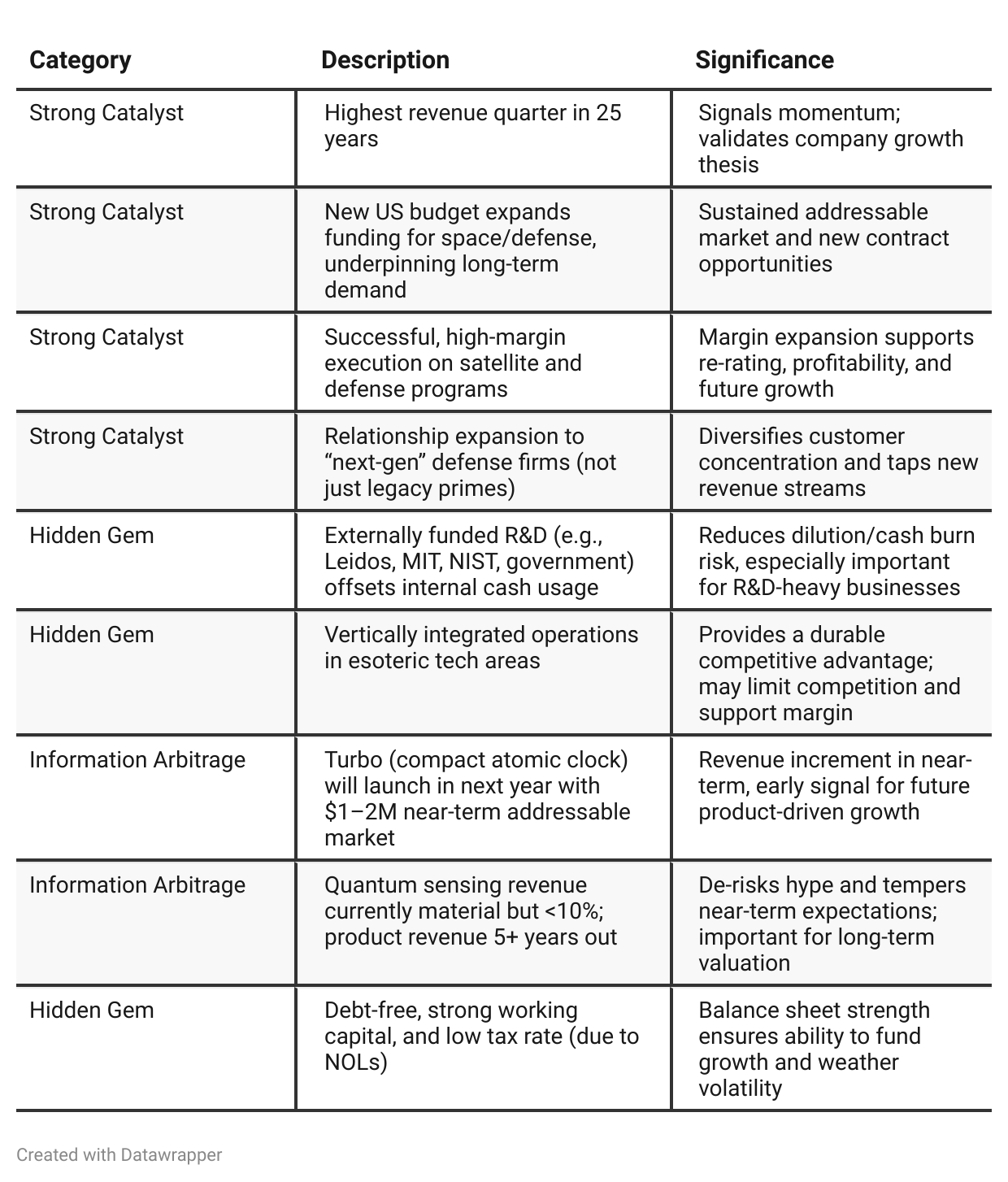

Positive Insights

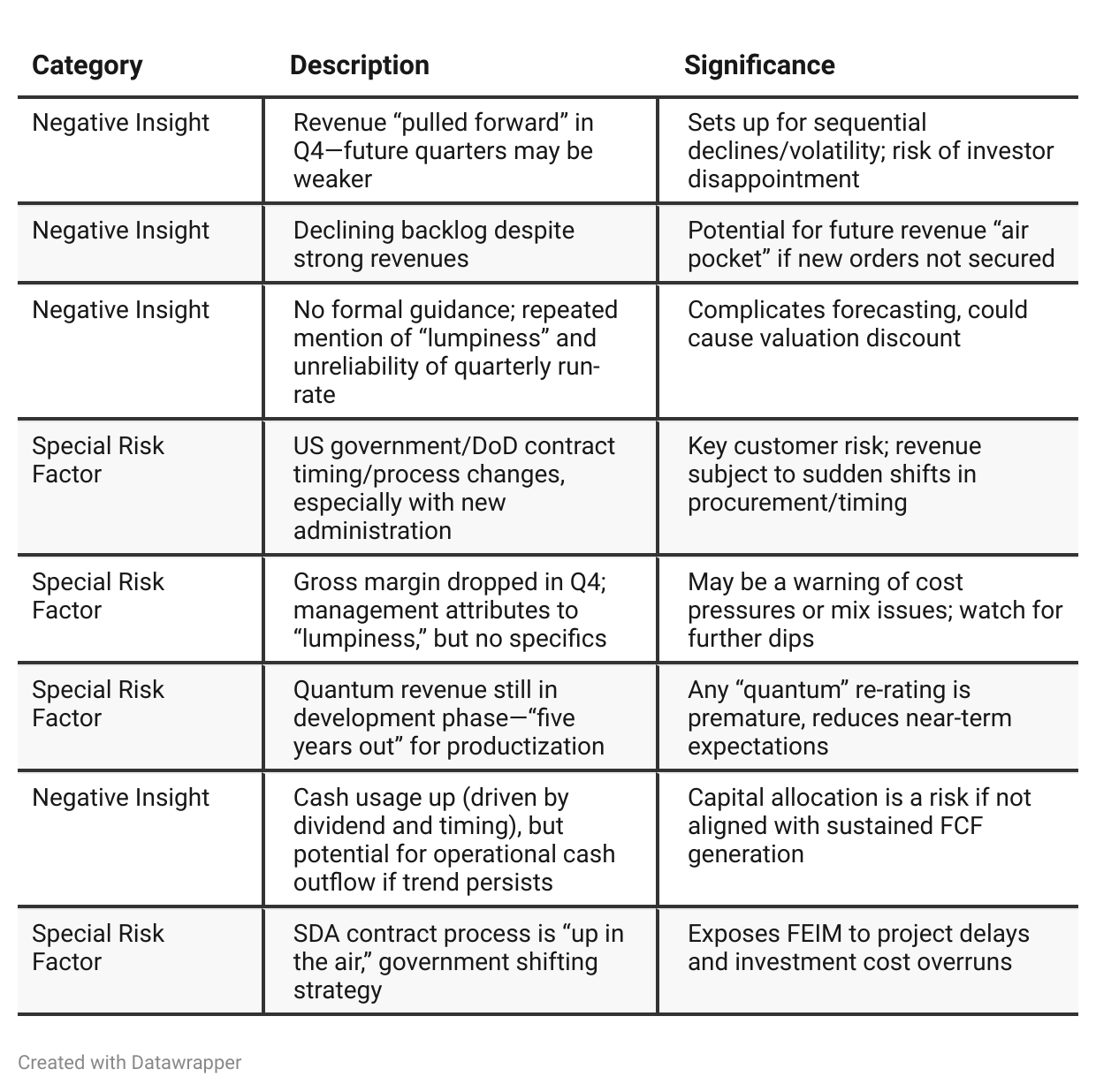

Negative Insights

Tariff Risk

There were no explicit mentions of tariffs or U.S. trade policies in the transcript. The focus is primarily on U.S. government defense/space contracts. Risks tied to trade barriers were neither addressed as direct threats to supply chain, revenue, nor profitability.

No adjustments to production, supply chain, or pricing policies in response to tariffs were discussed.

No anticipated impact on market share, competitive positioning, or innovation related to tariffs was outlined.

No forward-looking statements concerning potential future effects of tariffs were made.

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

From Q3 to Q4 2025, Frequency Electronics has moved from a period of pronounced optimism and pride in operational momentum (driven by new programs, fast delivery, and workforce engagement) to a more nuanced and candid stance. While Q4 proudly delivers record results, management goes out of its way to caution investors not to expect this level to repeat in the near term, citing significant variability in government contract timing due to shifting political and industry priorities. The core strategy—expansion in quantum sensing, navigation, and space systems—remains intact, as does confidence in the company’s long-term positioning, R&D leadership, and staff capability. However, management’s tone now reflects prudence and transparency, particularly regarding the unpredictability of contract awards and the non-linearity of near-term performance. There is also greater emphasis on diversifying the customer base and leveraging external R&D partnerships to manage capital needs. In sum, the narrative evolves from high-conviction momentum to balanced optimism, signaling maturity and honest stewardship as the company faces a more complex, politically influenced contracting environment.Year-over-year comparison

In Q4 2024, FEIM presented itself as a company scaling efficiently with “booming” business, a record backlog, and happy shareholders thanks to robust profitability and special dividends. The main risks were competitive and technical, but management sounded confident in managing them.

By Q4 2025, after delivering even higher (but “pulled-forward”) financial results, management’s tone is more nuanced. They openly acknowledge heightened risks from government contract timing, political change, backlog decline, and the unpredictability of major project awards. Strategy has shifted to prudent, targeted investment, greater external funding, and agile customer diversification while doubling down on long-term technical leadership—especially in high-potential but not-yet-mature spaces like quantum sensing.

Final Takeaway

Frequency Electronics (FEIM) is in a growth phase with strong momentum in defense/space end-markets and a differentiated technology portfolio. Despite record financials, management signals near-term volatility due to contract timing and backlog swings. Key growth initiatives in quantum sensing and resilient navigation offer long-term promise, but revenue impact from these is several years out. Investors should monitor new contract wins and backlog rebuilding, as execution on pipeline conversion will be critical for future outperformance. Verdict: Hold, with upside contingent on new order trends and confirmation of margin resilience.