Expensify, Inc. (NASDAQ: EXFY) – Q2 2025 Earnings

Expensify, Inc. (NASDAQ: EXFY) – Q2 2025 Earnings

Earnings Release Date: Aug. 07, 2025

Stock Price: $1.98

Market Cap: $181.1 million

Q2 2025 sales of $35.8 million vs $33.3 million in the prior year

Q2 2025 EPS of $-0.10 vs $-0.03 in the prior year

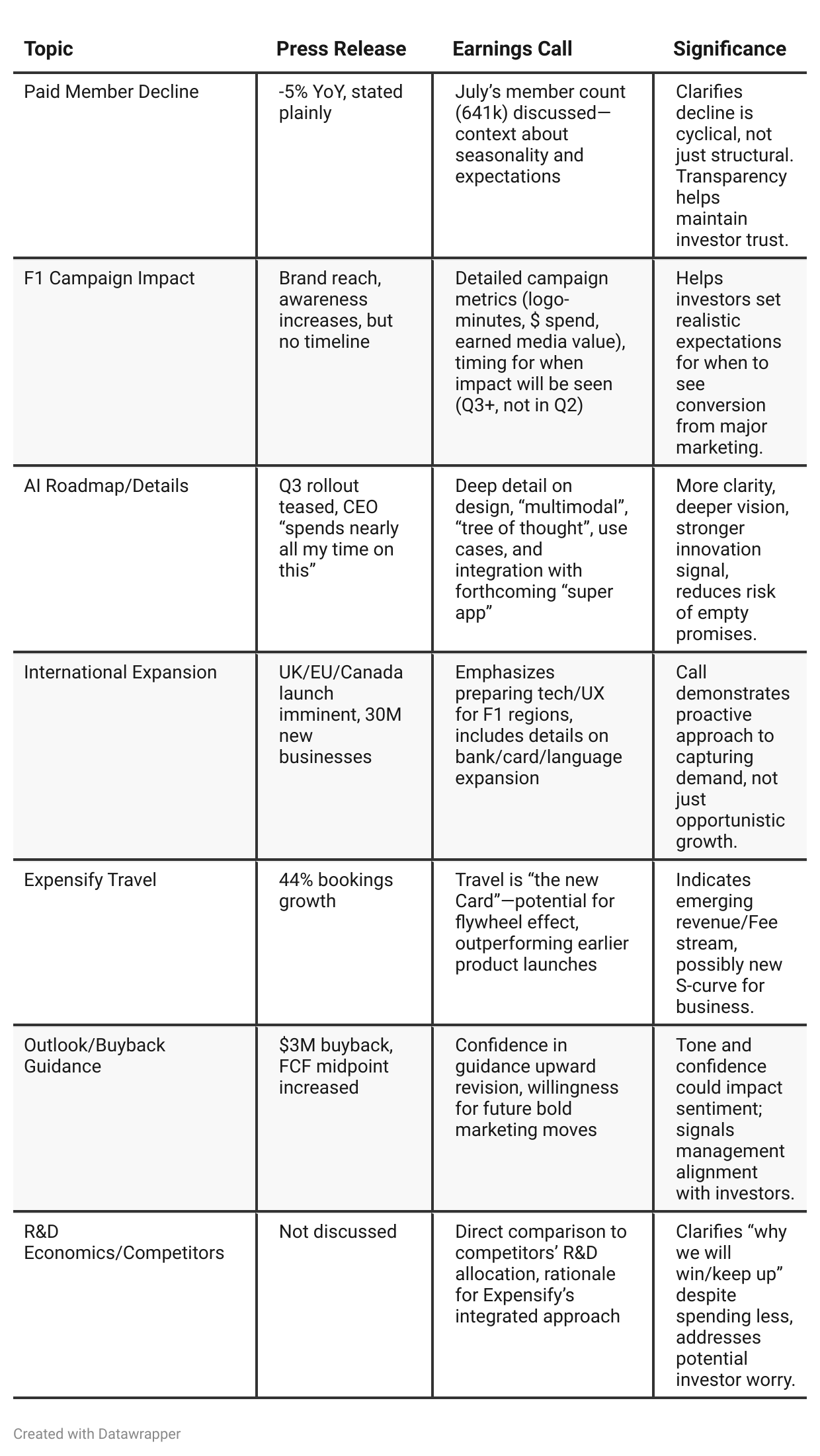

Press Release vs Call Transcript Comparison

Seasonality and Churn: Management is proactively communicating that member churn is expected in summer, and not indicative of an underlying change in demand.

Transparency: The call is forthright about what data is and isn’t available (e.g., F1 acquisition attribution), even in the face of investor pressure to show direct conversion from marketing campaigns.

Long-term Strategic Clarity: The earnings call clearly articulates that the “super app” vision is not abandoned, just sequenced behind completing migration and core AI features.

Marketing ROI: The call quantifies indirect marketing reach (earned media, logo views), indicating sophisticated attribution modeling—important for investors skeptical of splashy ad spends.

Competitive Readiness for AI/SEO Paradigm Shift: Expensify’s pre-existing strong SEO position and specific focus on chat-based AI differentiates it from other PLG companies that may not adapt as well to evolving search paradigms.

Cautious but Positive Tone on Guidance: Both documents reinforce confidence but avoid over-promising on near-term metrics, which could signal disciplined management.

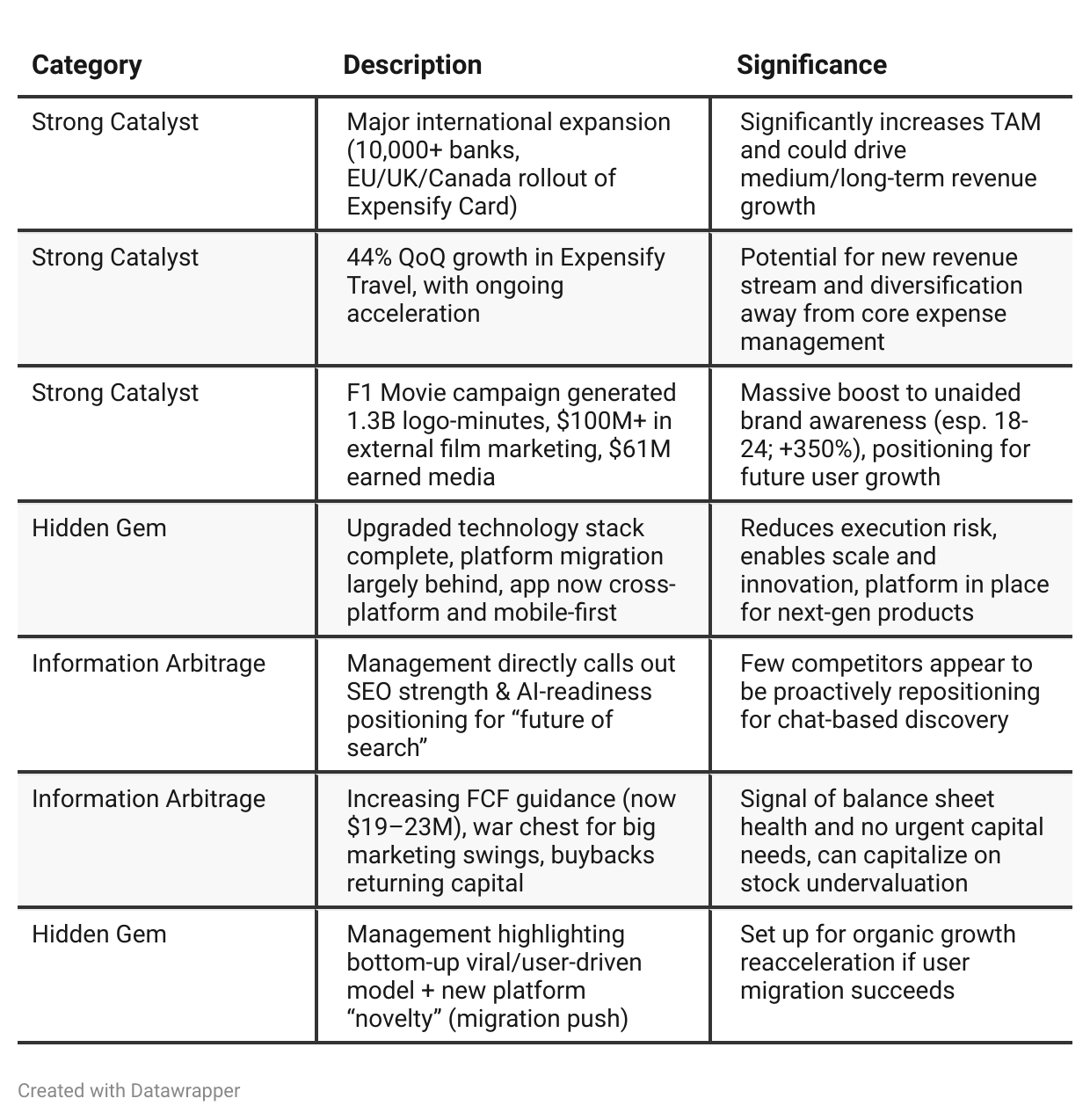

Positive Insights

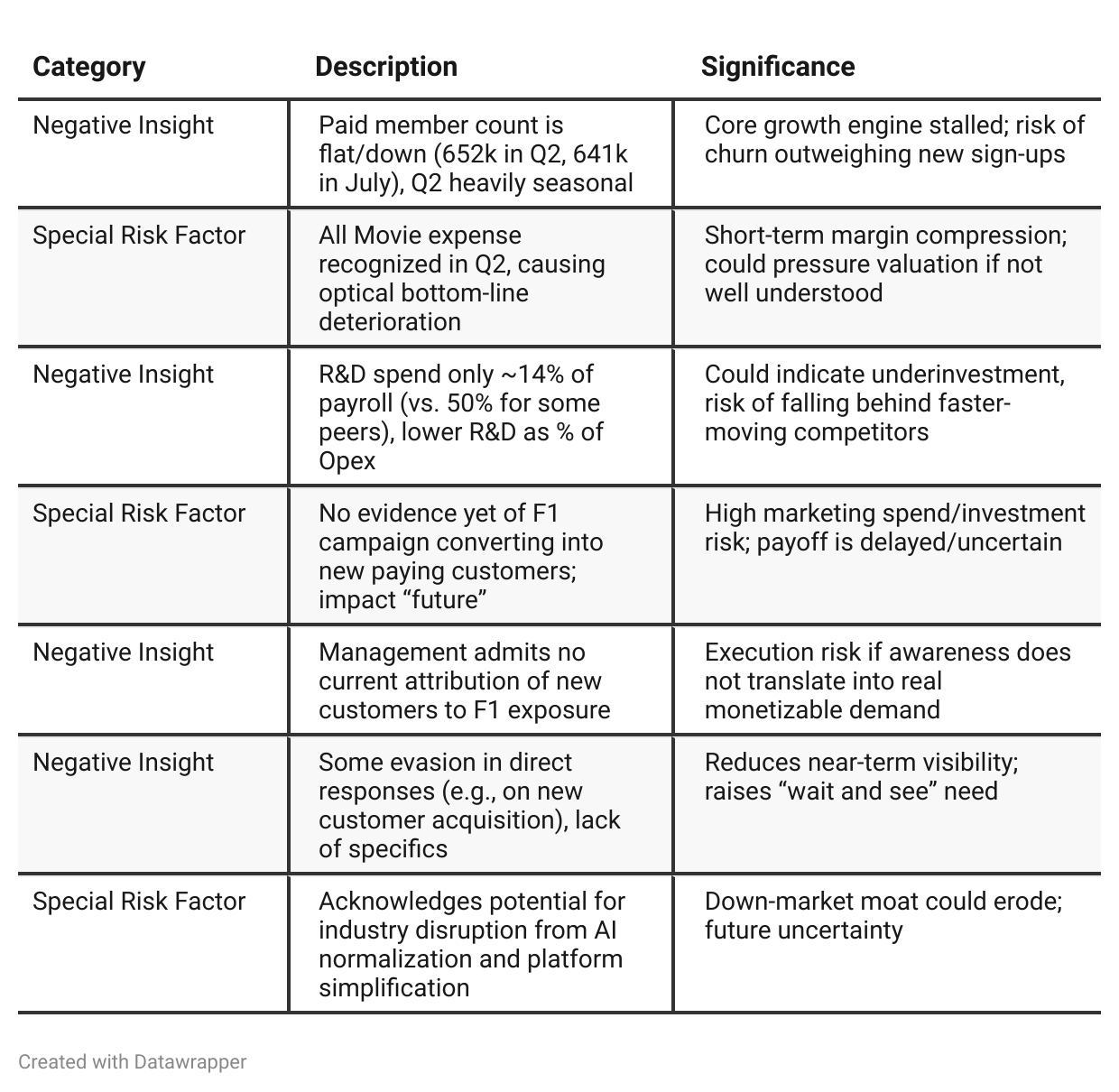

Negative Insights

Tariff Risk

Transcript Analysis:

There are no direct mentions of tariffs, trade policy, or related supply chain concerns in this transcript.

No discussion of shifting suppliers, currency/FX, or tariff-driven cost pressures observed.

No commentary on potential or actual impacts to revenue, market share, or innovation stemming from US-China or any other tariffs.

Conclusion for Tariff Risks:

For this period, analysis of Expensify’s risk profile does not require tariff monitoring. Investors should verify future transcripts and filings for any changes, especially in the context of international expansion, but as of Q2 2025, tariffs are not a factor for the investment thesis.

Previous Earnings Call

Quarter-over-quarter comparison

From Q1 to Q2 2025, Expensify’s narrative has evolved from optimistic anticipation of long-awaited marketing and product catalysts to a phase of active digestion, strategic recalibration, and more transparent risk management. The first call was buoyed by strong financials, runaway travel growth, and “wait for F1 impact,” with management shifting attention away from paid users as the linchpin metric. By the Q2 call, reality had set in: The F1 campaign’s true ROI is still on the horizon, paid user growth hasn’t yet inflected, and the company fielded tougher questions on execution and competition. However, Expensify doubled down on longer-term AI innovation, international platform reach, and diversified product ambition—communicating a clear, evolving strategy, and a willingness to be candid about timing, risks, and ongoing adaptation. Story: From expectation and set-up, to delivery, explanation, and a tempered call for patience as investments mature into performance.Year-over-year comparison

From Q2 2024 to Q2 2025, Expensify’s narrative evolved from product launch, technical rebuild, and the anticipation of transformative brand marketing, to the real-world digestion of those investments. What was once “set-up” became execution: the company went from building its platform and setting the table for international, super-app, and AI-led growth, to facing the reality of outcome delays and the ongoing grind of user migration, conversion, and competition. Optimism remains about long-term differentiation, but the story has matured—less about potential, more about measured patience, transparent acknowledgment of timing risks, and project-by-project evaluation of ROI and execution.

Final Takeaway

Expensify is in a strategic transition phase, focusing on international expansion, travel growth, and leveraging a major brand push from its F1 campaign. While catalysts are building—especially with platform upgrades and expanded addressable markets—execution risk remains high until paid member and revenue acceleration are proven. Conversion of heightened brand awareness to monetizable growth and continued success in new markets will be critical. Verdict: Hold, with meaningful upside if F1/Travel/Card expansion converts in coming quarters, but caution warranted until metrics clearly inflect.