EVI Industries, Inc. (NYSE: EVI) – Q4 2025 Earnings

EVI Industries, Inc. (NYSE: EVI) – Q4 2025 Earnings

Earnings Release Date: Sep. 11, 2025

Stock Price: $27.64

Market Cap: $352.1 million

Q4 2025 sales of $110.0 million vs $90.1 million in the prior year

Q4 2025 EPS of $0.14 vs $0.14 in the prior year

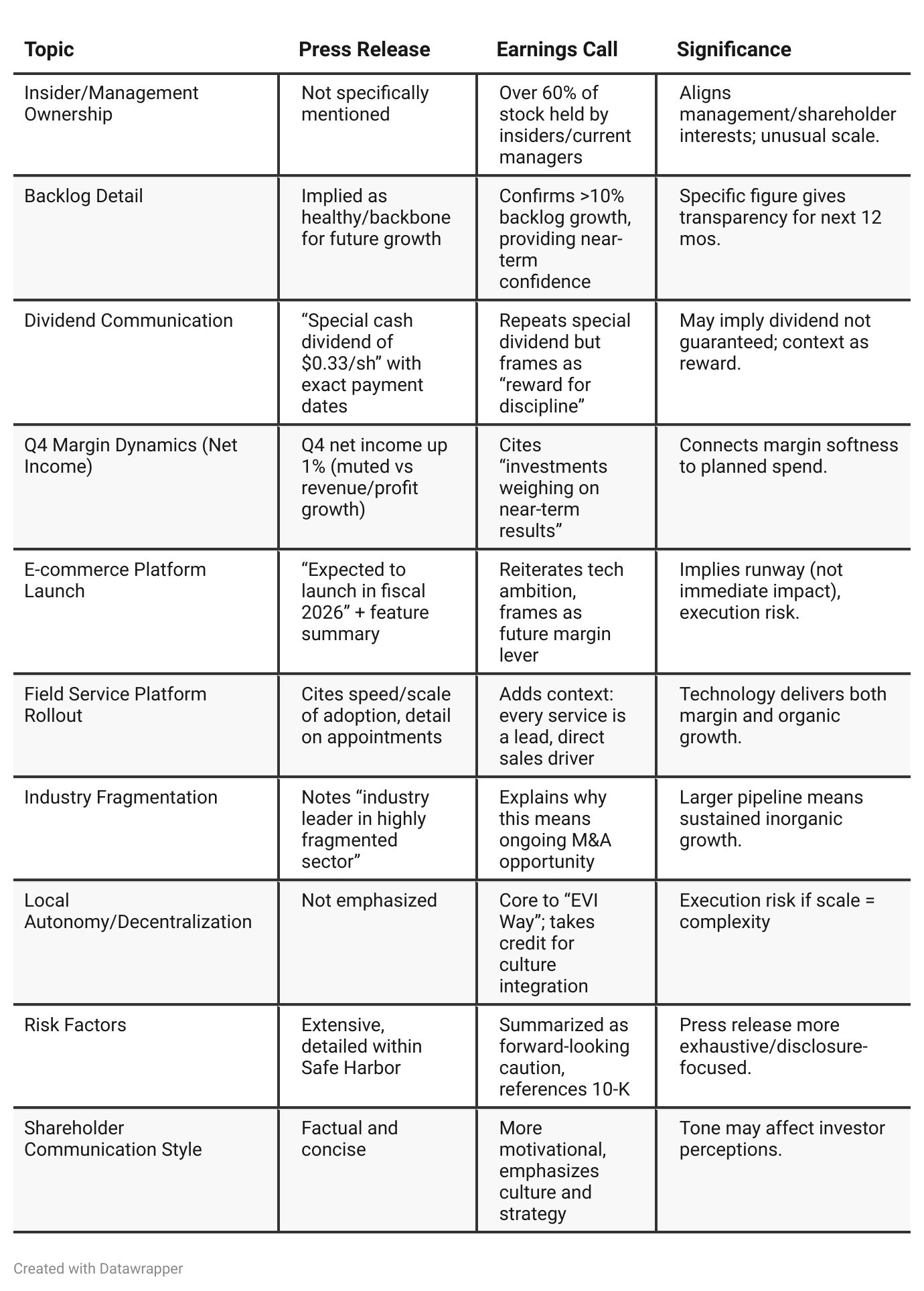

Press Release vs Call Transcript Comparison

Market Position: Both documents reinforce EVI's status as a consolidator and acquirer-of-choice in a fragmented industry. This supports a long growth runway, but also invites the classic roll-up risks.

Quality of Execution: Management shows consistent awareness of needing to convert tech investments and scale into actual margin/earnings—not just revenue. Explicit mention of near-term sacrifices for long-term gains provides some transparency.

Quantitative Consistency: All financial data and growth rates (revenue, margin, acquisition count) are aligned across both documents, lending credibility.

Leadership’s Forward Focus: The call goes much further in framing long-term vision, employee focus, and the reasons “why” behind every move; the press release is more transactional.

Sustainability of Dividend: Investors should be clear that the ongoing special nature of the dividend is not permanent policy—reinforced by the language in both disclosures.

Potential Red Flag: The heavy emphasis on “record results” alongside only marginal Q4 profit growth could indicate rising costs or deal integration issues.

Balance Sheet Watchpoint: Net debt materially higher due to deal flow; worth monitoring if deal pace slows or integration stumbles.

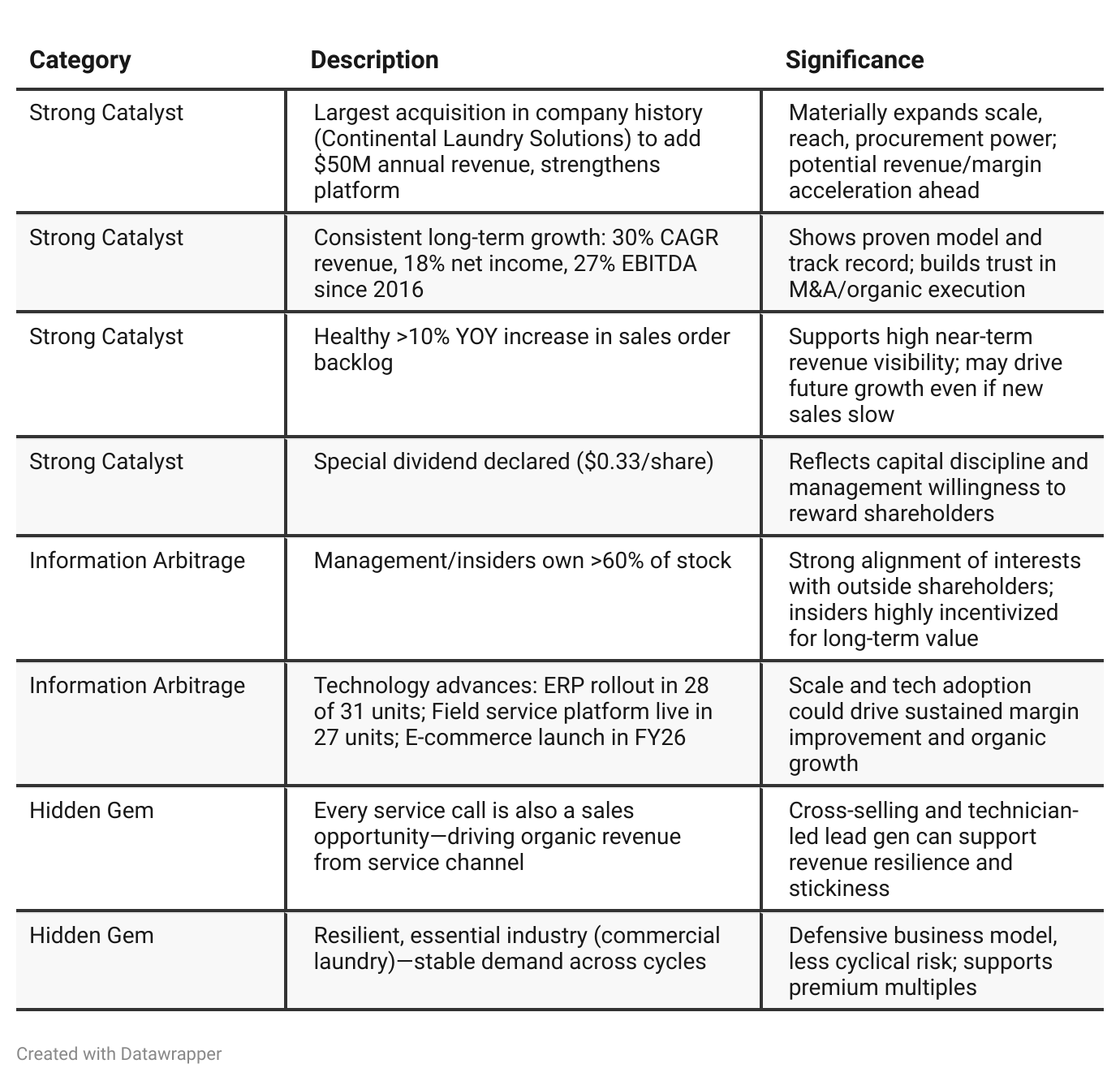

Positive Insights

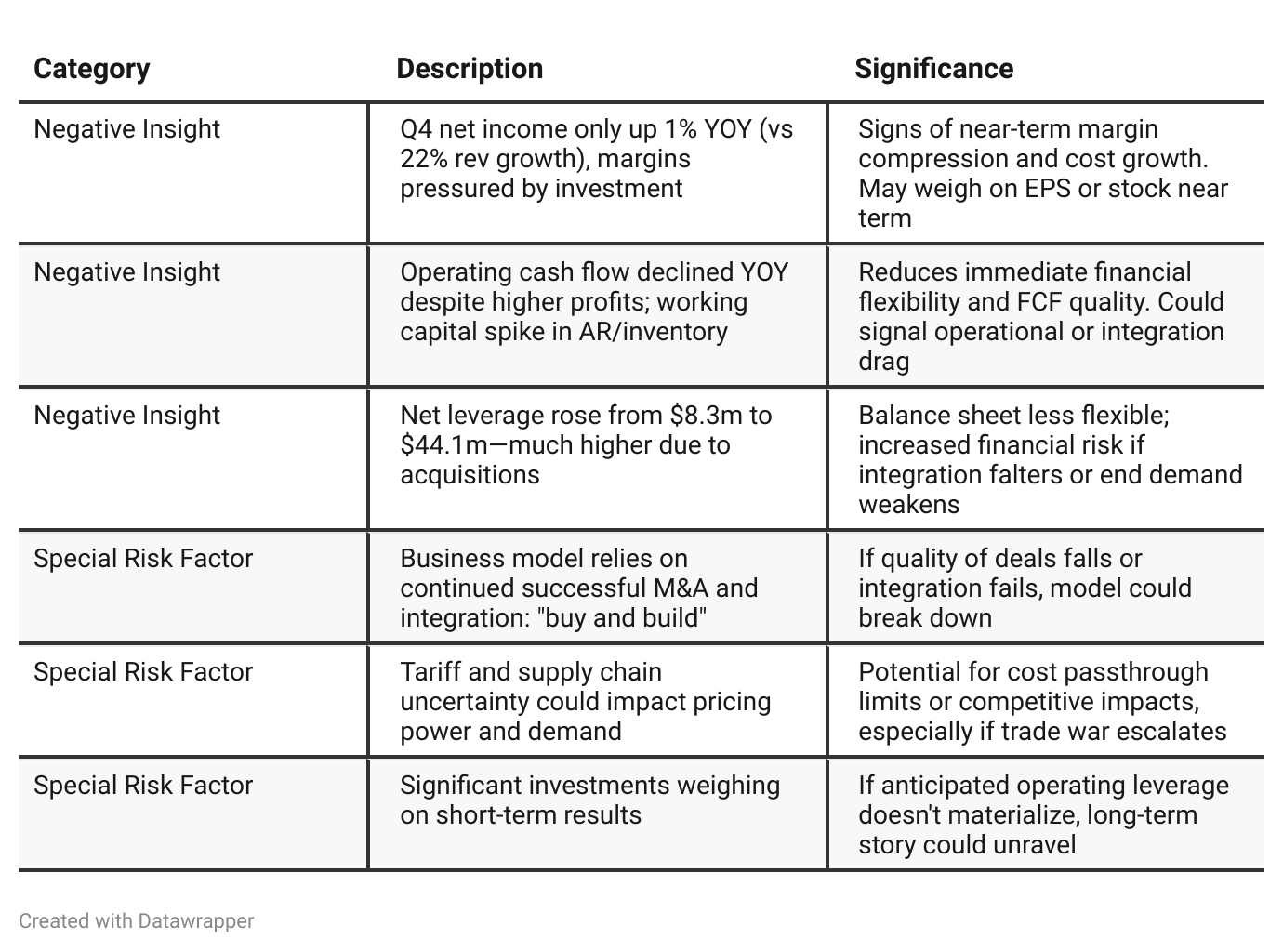

Negative Insights

Tariff Risk

EVI notes "continuing to monitor tariff developments," with OEM partners and suppliers already implementing price increases.

Company has "adjusted pricing accordingly" but acknowledges "uncertainty remains."

Mitigating actions: collaborating with partners to manage costs, maintaining focus on product competitiveness, and diversifying across markets/parts.

No mention of shifting supply chain, changing production, or other structural changes in response to tariffs (actions are primarily pricing and sourcing collaboration).

Identifies tariffs as an external risk, but sees core demand as resilient due to "essential equipment."

Forward look: "Working closely with partners to manage, ensure competitiveness even as tariff conditions evolve." No quantified cost/disruption impact given; investors should monitor for price pass-through sustainability and margin impacts if trade tensions escalate.

Previous Earnings Call

Quarter-over-quarter comparison

Between Q3 and Q4 2025, EVI Industries’ narrative has shifted from one of aggressive expansion and optimism following a transformational acquisition (Girbau North America), to a more balanced message that acknowledges both achievement and near-term challenges. The company has matured its messaging: moving from pure top-line and operational excitement to a focus on integrating acquisitions, managing higher leverage and working capital needs, and laying groundwork for future margin expansion through strategic tech investments. The Q4 call evidences a more forward-looking and self-aware management team, openly discussing both current pressures (investment drag, tariffs, rising inventory) and future growth levers (special dividend, backlog, technology, e-commerce launch). Overall, while the core strategy and optimism are unchanged, the tone now exhibits greater transparency, discipline, and strategic patience as the company moves into the next phase of its growth story.Year-over-year comparison

In Q4 FY2024, EVI Industries focused on balance sheet strength, cash flow generation, and steady, incremental gains through organic growth and smaller acquisitions, all backed by a conservative approach to investment and capital return. The narrative prioritized operational discipline, prudent expansion, and groundwork technology investment.

By Q4 FY2025, the company’s tone and story have evolved—now presenting itself as a national, technology-driven consolidator poised for the next phase of scale and efficiency. The acquisition of Continental not only accelerates the pace of growth but also places more emphasis on complex integration, technology platform leverage, and future margin expansion. Management is more transparent about short-term pressures (margin/headcount/inventory/leverage), openly discusses macro and trade risks, and is bolder about their strategic ambitions. The company frames itself as both the market leader and as a business with strong shareholder alignment, signaling readiness for larger, tech-influenced opportunities and also acknowledging bigger execution risks.

Final Takeaway

EVI Industries is in a growth-to-scalability phase, focusing on acquisition-driven expansion, technology-enabled efficiency, and margin enhancement. While the company demonstrates a strong track record and currently enjoys a solid backlog and sector tailwinds, concerns around margin pressures, increased leverage, and working capital usage merit caution. Execution on integration, operating leverage realization, and cash flow improvement will be critical "watch" factors for future performance. Verdict: Hold, with upside potential if fiscal discipline is proven and integration delivers expected benefits.