Electromed, Inc. (NYSE: ELMD) – Q4 2025 Earnings

Electromed, Inc. (NYSE: ELMD) – Q4 2025 Earnings

Earnings Release Date: Aug. 26, 2025

Stock Price: $20.20

Market Cap: $168.3 million

Q4 2025 sales of $17.4 million vs $14.8 million in the prior year

Q4 2025 EPS of $0.25 vs $0.20 in the prior year

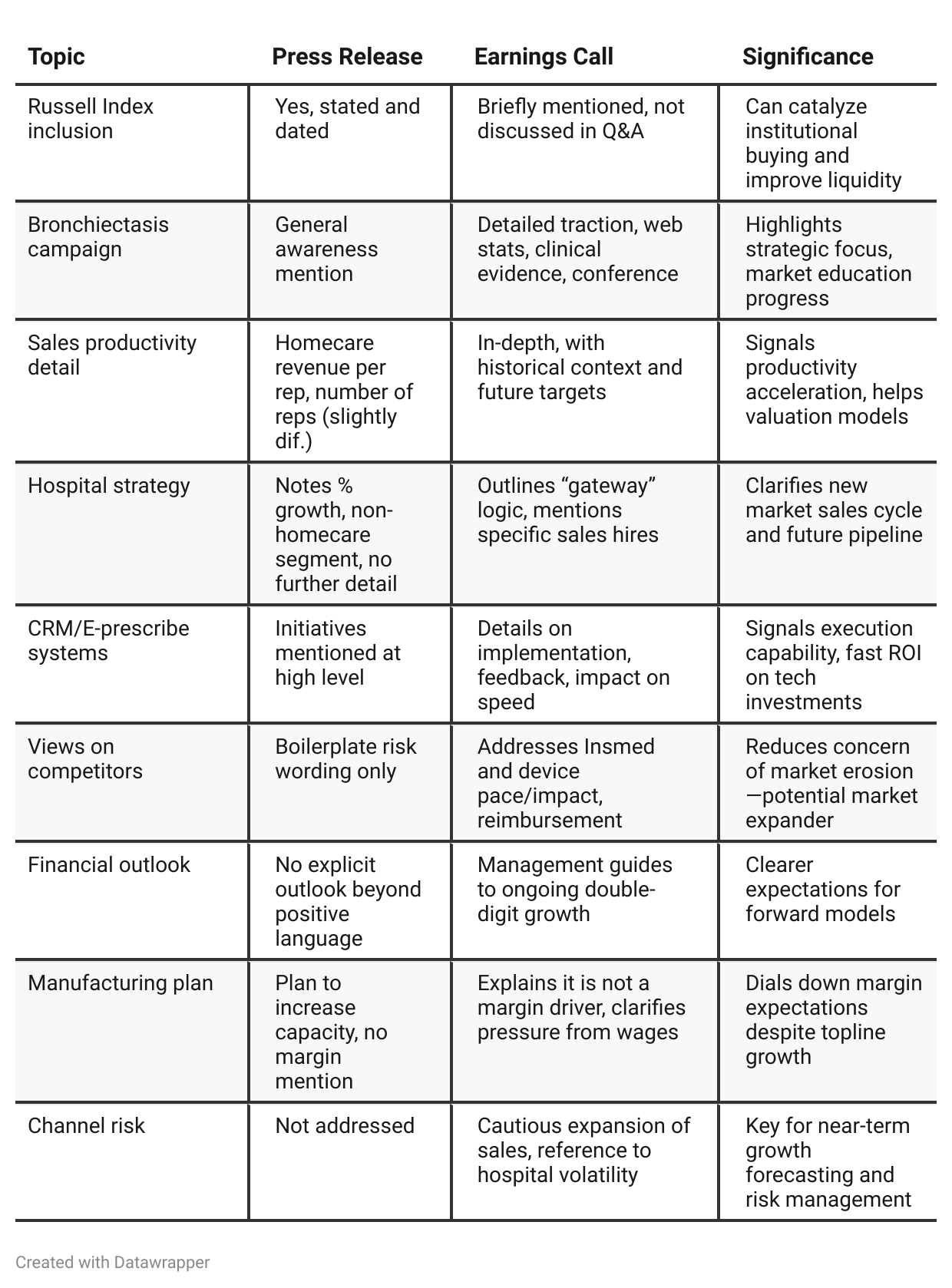

Press Release vs Call Transcript Comparison

Balance Sheet Health: Both documents confirm zero debt, strong working capital, but only the earnings call discusses the sources/uses for ongoing cash deployment.

Capital Allocation: The press release states buybacks, but the call frames these as showing management’s confidence—potential signaling to investors.

Leadership Tone: CEO in call uses visionary, motivational framing (“continuous journey of excellence”), which may boost investor sentiment.

Preparedness for Growth: Call details show a methodical, almost measured approach to capacity, hiring, and sales channel investments—suggesting downside protection but possible modest upside surprise risk if market opportunity accelerates.

Investor Communication: Both documents are conservative in language regarding guidance (typical for Electromed), but the call provides much more forward color.

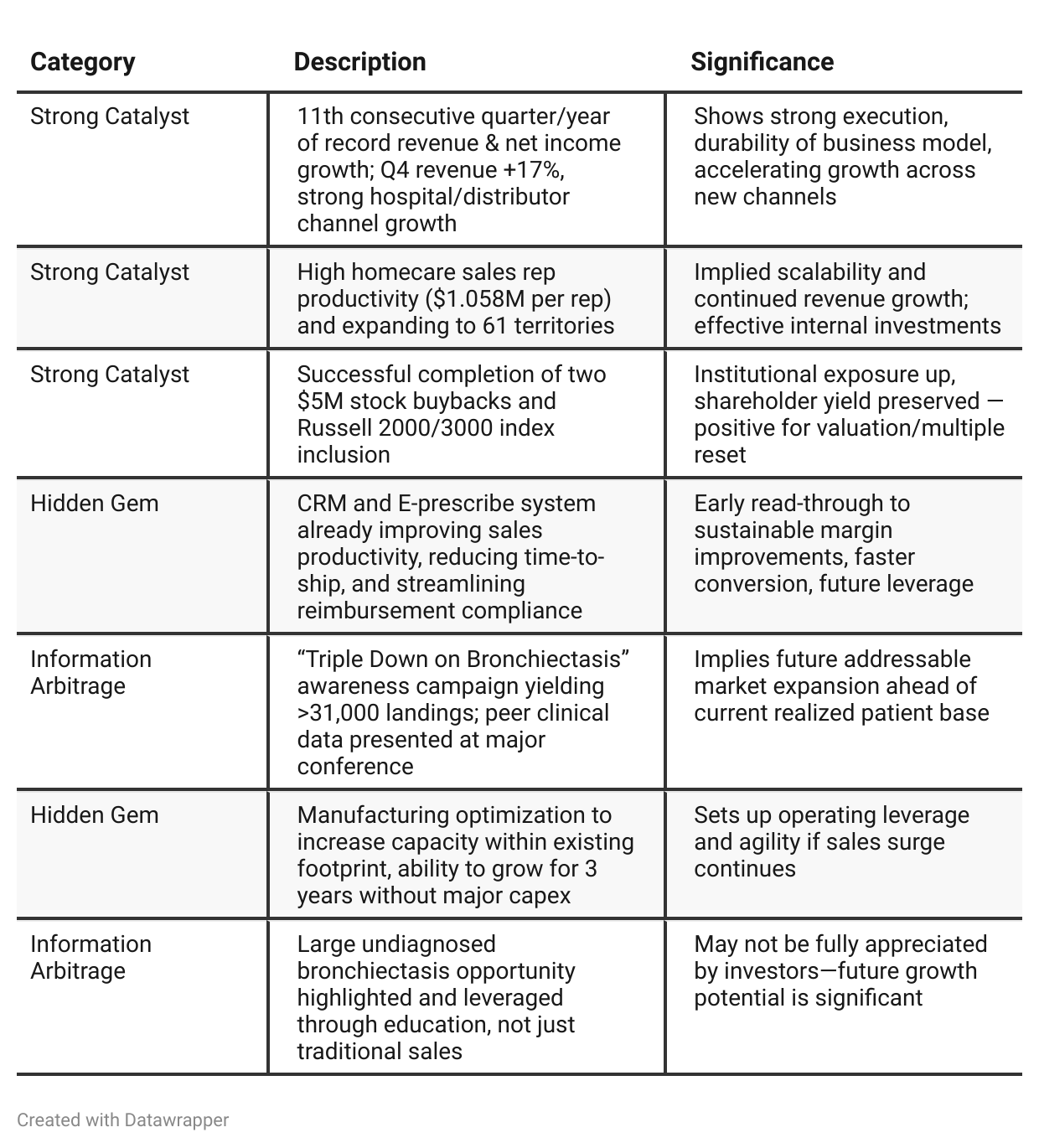

Positive Insights

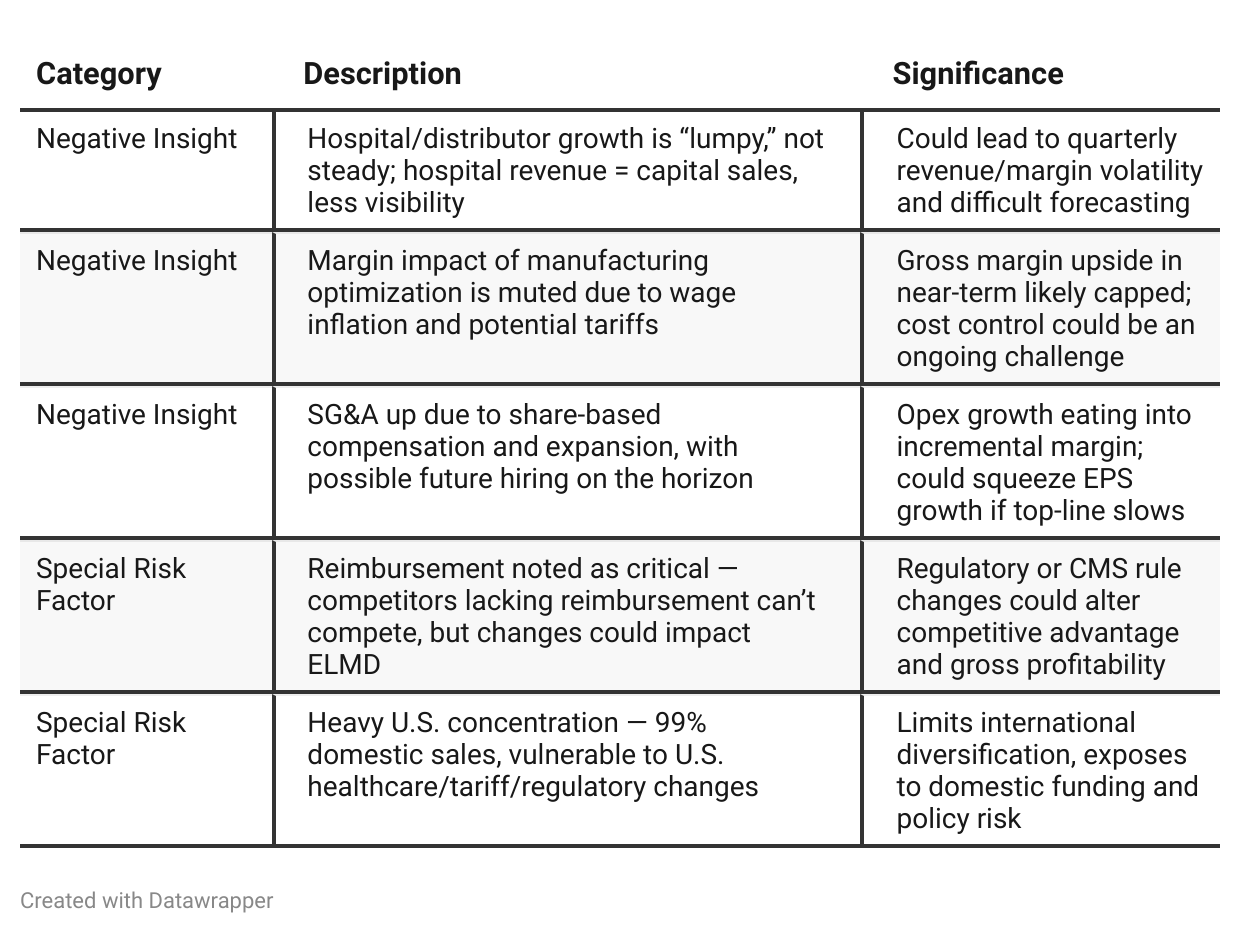

Negative Insights

Tariff Risk

Management states 99% of revenue is U.S.-based and all manufacturing is domestic, which insulates ELMD from direct tariff shocks.

However, "tariffs are a fluid situation"—they monitor U.S. suppliers for upstream exposure. Some supplier risk may exist and indirect cost pass-through is possible.

No impact currently cited on revenue, profitability, or supply chain continuity. Company feels positioned to maintain mid-70% gross margins, but wage increases and any future tariff escalation could offset manufacturing efficiency gains.

No mention of altering sourcing, contracts, or pricing directly—implies they have not faced material headwinds yet.

Forward-looking commentary: management is watching the situation, and margin management is a key focus given potential volatility.

Previous Earnings Call

Quarter-over-quarter comparison

In Q3 2025, Electromed presented itself as a disciplined, steadily growing medical device company, focused on careful and deliberate foundation building—thoughtfully expanding its salesforce, preparing for digital transformation (CRM/e-prescribe), and building brand and disease awareness through industry channels and targeted initiatives. There was healthy caution in their tone, especially around execution risk and operational scaling.By Q4 2025, the narrative matured into one of accelerating momentum and broader ambition. The company not only delivered its 11th consecutive growth quarter but did so with record results in new and existing channels. Management's tone amplified, highlighting bold achievements (record revenue/income, Russell index inclusion, massive channel growth), a completed rollout of new digital tools, and stronger forward guidance for both productivity and expansion. Risks were still openly discussed (tariffs, SG&A, hospital sales lumpiness), but were framed as either manageable or offset by the company’s enhanced capabilities and market opportunities. Competitive threats were reframed as awareness boosters, not existential threats. The overall messaging signaled a company transitioning with confidence from a phase of careful, foundational growth to one of assertive scaling and broad-based execution.

Year-over-year comparison

From Q4 2024 to Q4 2025, Electromed has transitioned from a solid performer focused on building operational leverage and expanding market opportunity, to an accelerated, self-assured growth company positioned as an emerging industry leader. The earlier narrative was about optimization, process improvement, and careful expansion. By 2025, the story is one of scaling, outpacing competitors through strategic execution (including digitalization and sales force productivity), and achieving industry validation (via index inclusion and channel growth surges). Management has moved from simply beating performance benchmarks to confidently setting new, higher expectations for channel expansion, customer engagement, and operational reach. Competition and risks are now openly managed with strategic clarity, while digital transformation and productivity gains are no longer aspirations, but proven realities fueling continued momentum.

Final Takeaway

Electromed is in a high-growth phase, rapidly expanding its core homecare business while skillfully building out new channels (hospital, DME) and improving operational efficiency. Growth catalysts include robust execution, expanding salesforce, major awareness and education campaigns, and process digitization. However, near-term risks exist—mainly quarterly unpredictability in smaller channels and inflation/tariff headwinds—alongside heavier domestic exposure. Execution on sales productivity, channel expansion, and margin protection will be critical for sustaining outperformance.

Verdict: BUY, with strong upside as execution continues and margin stability is preserved. Future reporting/filings should be monitored for guidance clarity and early signs of competitive or reimbursement risk.