Educational Development Corporation (NASDAQ: EDUC) – Q2 2026 Earnings

Educational Development Corporation (NASDAQ: EDUC) – Q2 2026 Earnings

Earnings Release Date: Oct. 09, 2025

Stock Price: $1.52

Market Cap: $13.0 million

Q2 2026 sales of $4.6 million vs $6.5 million in the prior year

Q2 2026 EPS of $-0.15 vs $-0.22 in the prior year

Press Release vs Call Transcript Comparison

Earnings Call Much More Transparent: The call gave raw, actionable detail on operational stress, banking relationships, and timelines for recovery. Investors reliant solely on the press release would miss acute short-term risks.

Management Candor: The call showed management realism—they admit setbacks, detail causes, and set measured expectations for turnaround.

Building Sale is Binary Catalyst: If successful, risk profile changes drastically (from potentially insolvent to viable turnaround). If unsuccessful or delayed, default risk majorly elevated.

Restructuring Story: There’s clear progress—costs down, retail channel steady, actionable marketing moves to rebuild the brand partner channel, but execution is everything.

Event-driven Speculation vs. Long-term Hold: In near-term, stock is driven by sale completion. Long-term investors need confidence in management’s ability to recruit/re-engage sales force and execute a sustained multi-channel strategy.

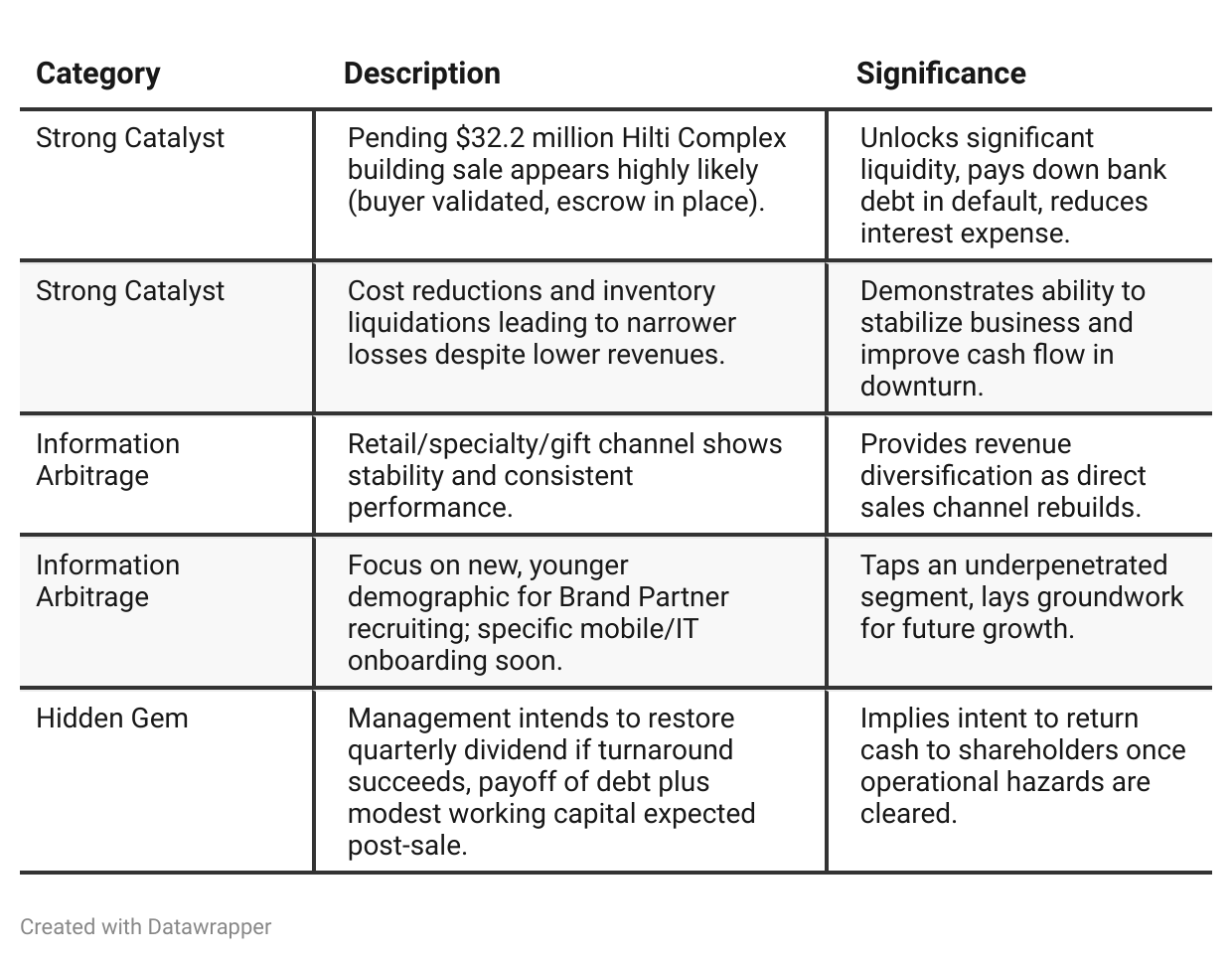

Positive Insights

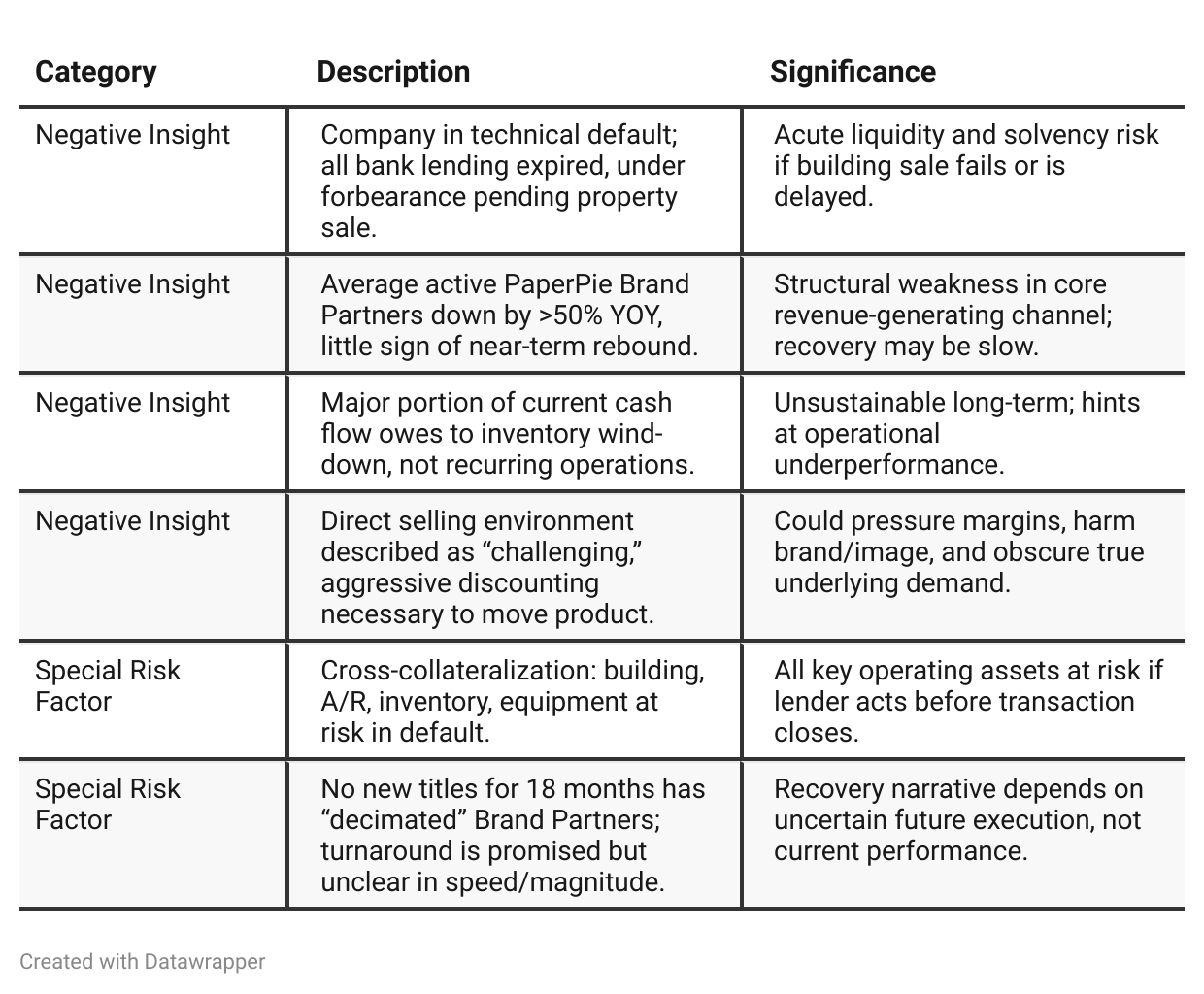

Negative Insights

Tariff Risk

Transcript Review: There are no explicit mentions of U.S. tariffs, trade policies, or related supply chain risks in the transcript.

Implied Position: EDUC’s business is primarily U.S.-centric (children’s books, direct selling, retail/partner channel), and no word is given about import dependencies, tariffs on components, or cross-border cost pressures.

Actions Taken: No strategies disclosed for mitigating tariff-related risks, such as supplier shifts, contract renegotiations, or price changes.

Investor Note: While no tariff exposure is raised, investors should verify future disclosures for any policy shifts or indirect risks (increased material costs, changes in partner sourcing, etc.) in upcoming filings or management commentary.

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Q1: EDUC is in “survival mode,” with management singularly focused on completing the Hilti Complex sale to avoid insolvency. Brand partner losses and industry weakness are biting revenues, while management juggles contingency plans, tight bank oversight, and governance tweaks. The mood is circumspect—acknowledging severe headwinds but still searching for optimism through cost controls, stakeholder loyalty, and a potentially viable fallback plan.Q2: By the next quarter, EDUC’s narrative has become more transparent and operationally focused. The company openly admits its credit default, but now presents detailed, credible steps to exit crisis mode via the impending building sale—naming the buyer and laying out post-paydown options. Instead of relying on generic turnaround rhetoric, the management team articulates concrete IT, marketing, and recruitment strategies aimed at reversing the decline in its core sales force. Yet, the existential risk remains—everything depends on closing the real estate transaction. Execution risk is high, but now paired with a clearer, more reality-based roadmap for recovery.

Year-over-year comparison

—

Final Takeaway

Educational Development Corporation is in a high-stakes restructuring phase, with its short-term future essentially riding on the successful close of a $32.2M real estate sale—a binary event. While management has a clear cost-reduction plan and an articulated growth strategy to rebuild its sales force and stabilize revenue, core metrics (Brand Partners, sales) remain pressured and liquidity is exhausted if the sale falters. Execution risk is high, but so is post-event optionality if the catalyst goes through. Verdict: HOLD, pending finality of the building transaction; investors should track liquidity, turnaround execution, and near-term financing updates closely.