Educational Development Corporation (NASDAQ: EDUC) – Q1 2026 Earnings

Educational Development Corporation (NASDAQ: EDUC) – Q1 2026 Earnings

Earnings Release Date: Jul. 7, 2025

Stock Price: $1.12

Market Cap: $9.7 million

Q1 2026 sales of $7.1 million vs $10.0 million in the prior year

Q1 2026 EPS of ($0.13) vs ($0.15) in the prior year

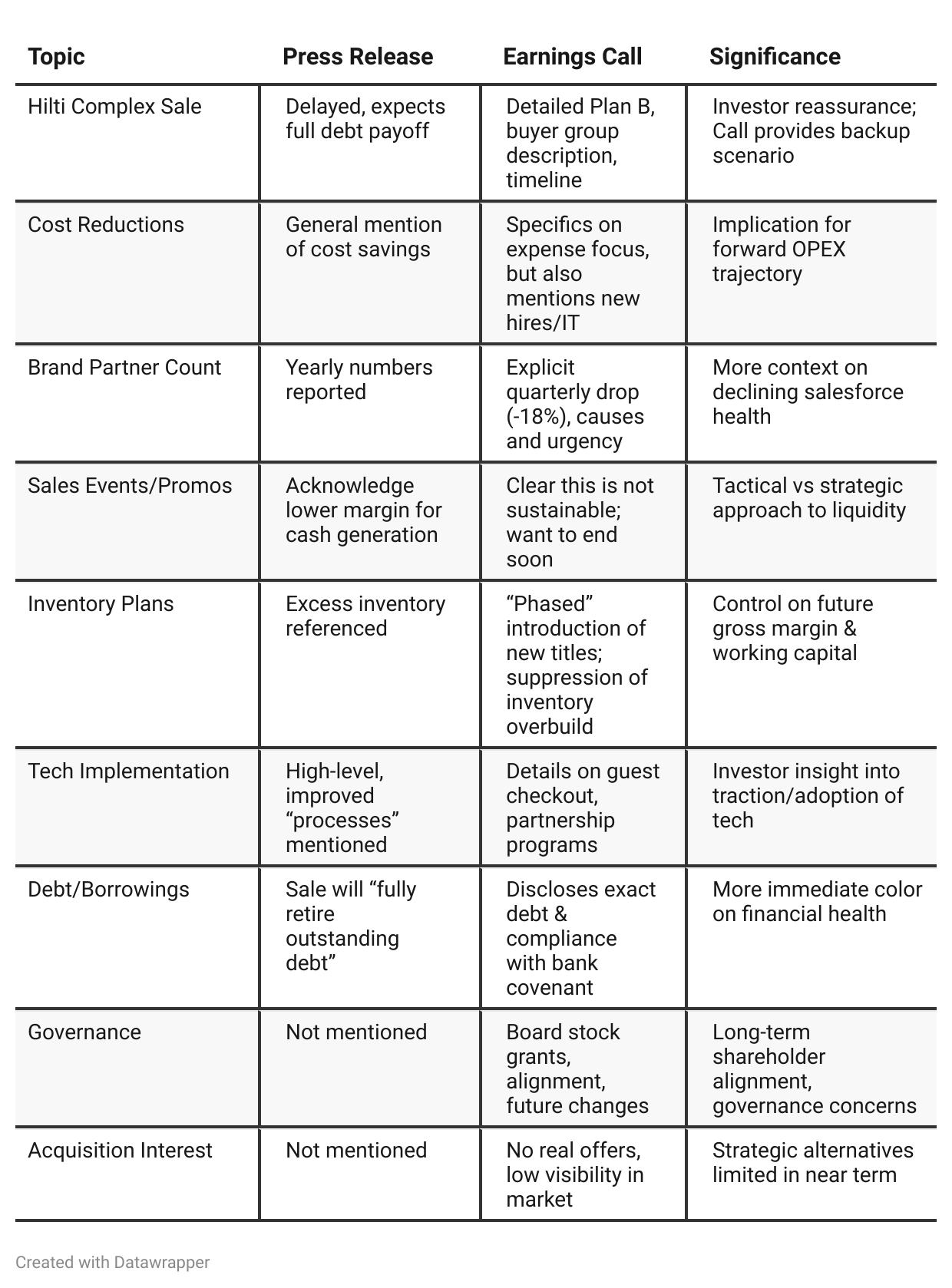

Press Release vs Call Transcript Comparison

Strategic Refocus: Management sees business normalization only after asset sale—signaling nothing will improve operationally until leverage is dealt with.

Shareholder Communication: Much more transparency about actions/alternatives in the call than in the release.

Operational Timeline: Key event—Hilti Complex sale—has an explicit target (end of September); investors should watch for updates closely.

Bank Relationship: Currently supportive, but clearly time-boxed and will shrink after repayment—future liquidity could be a constraint.

No Dividend: Not unexpected, but confirmed in data.

Cultural Signals: CEO now more engaged in industry, suggests possible culture shift or future openness to external influence.

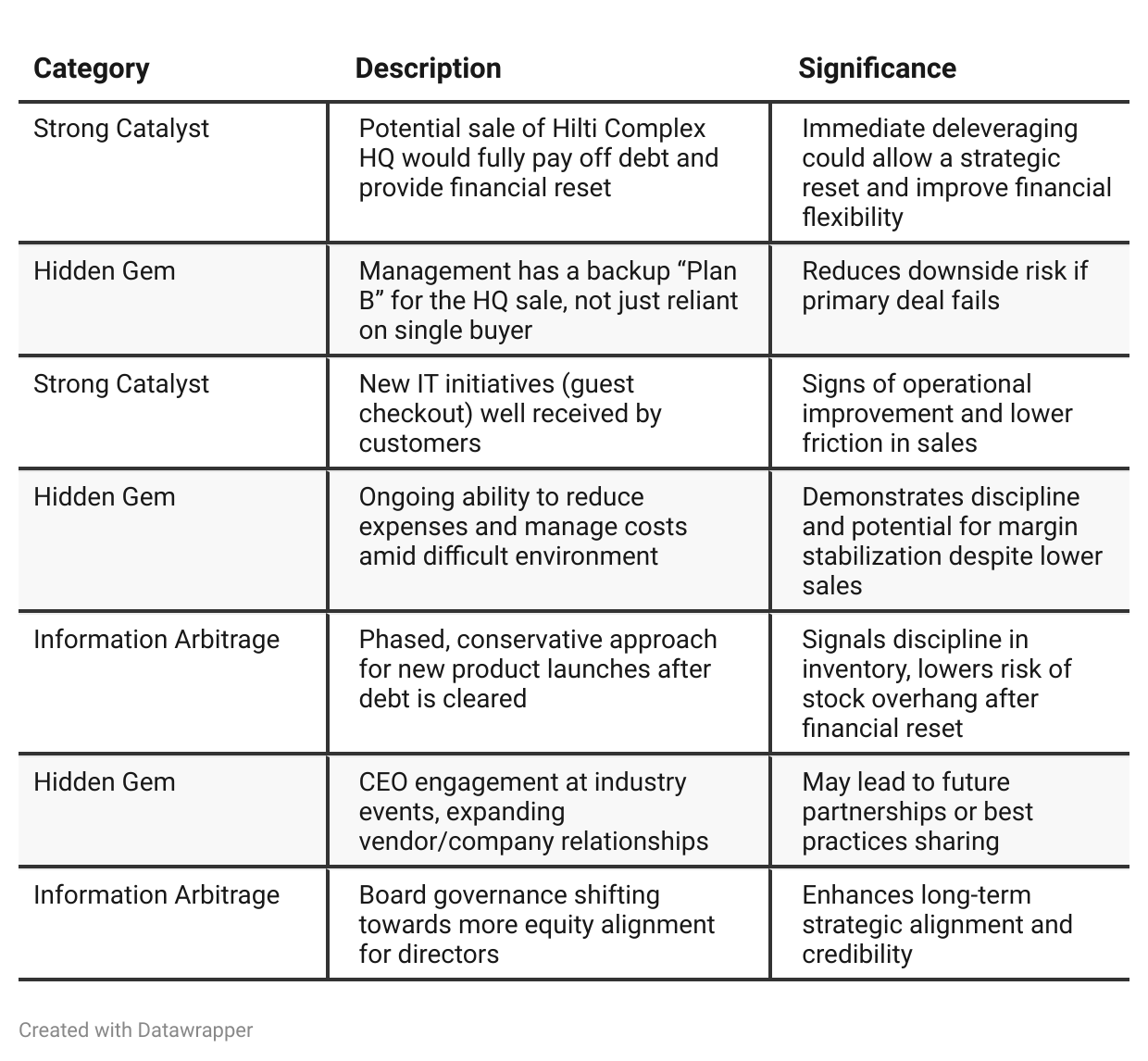

Positive Insights

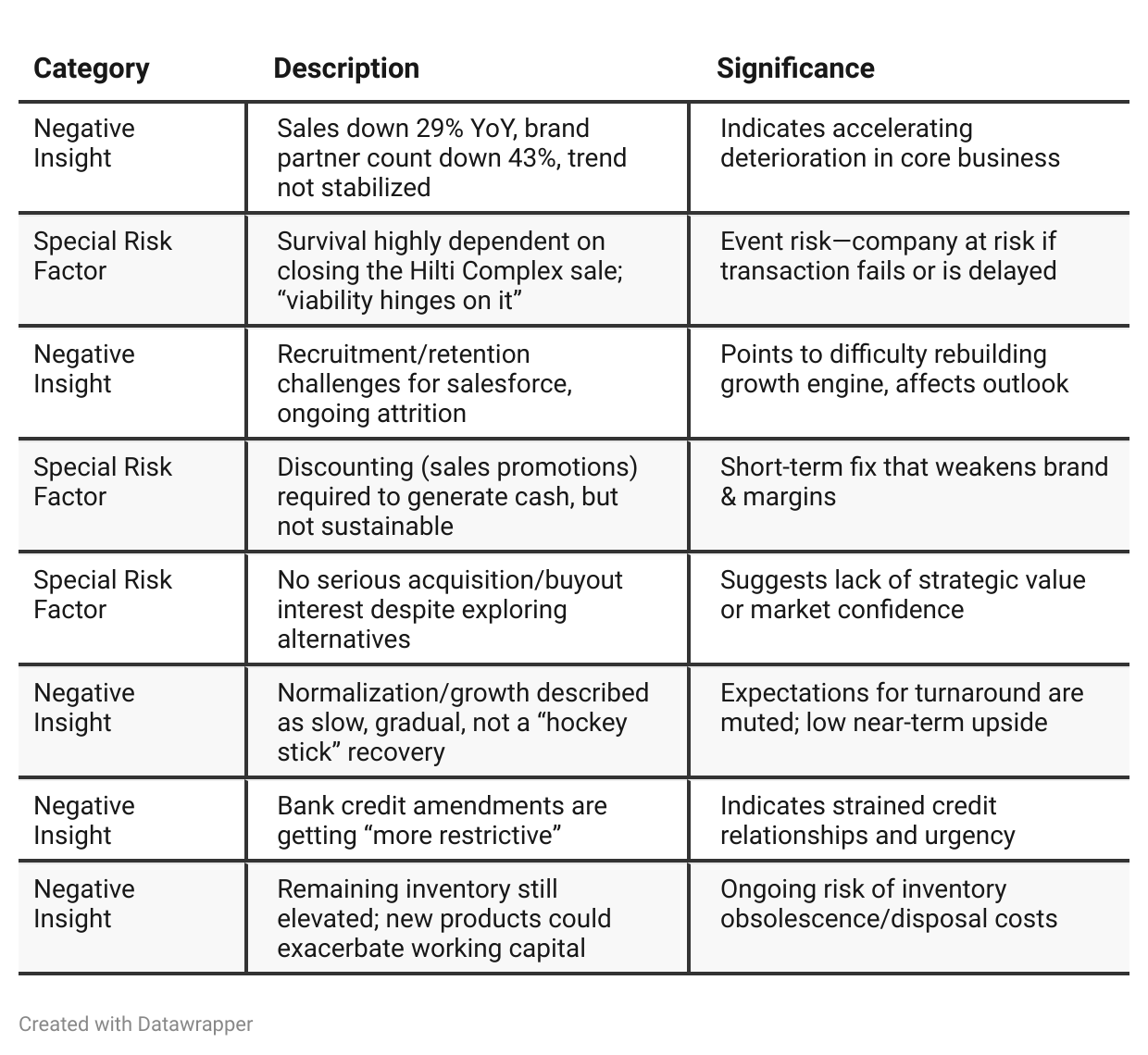

Negative Insights

Tariff Risk

No mention of U.S. tariffs or trade policy impact in this earnings call transcript. No discussion about tariffs affecting revenue, supply chain, competitiveness, or profitability. No stated mitigation or forward-looking projections specifically referencing tariffs.

Previous Earnings Call

Quarter-over-quarter comparison

Q4 FY25: Management tries to balance transparency about deteriorating top-line and brand partner metrics with optimism around customer initiatives, the shipping subscription, and future new title launches. Discounting is acknowledged as a cash tactic, but the message is one of adaptability, stakeholder support, and excitement for what’s next—provided the HQ sale closes.Q1 FY26: Narrative becomes starker: The company’s future is now explicitly tied to executing the building sale. Analyst skepticism rises (“viability hinges on getting that done”). Management walks through contingency planning, acknowledges prolonged challenges, and dampens any expectation of a quick rebound. The priority is strictly financial survival and risk mitigation; customer and sales excitement is severely diminished. There’s new talk of “Plan B,” board governance improvement, and a more disciplined, even defensive, stance.

Year-over-year comparison

Q1 2025 EDUC was facing operational and sales headwinds, but communicated hope and agency: management believed the sale of the Hilti Complex would provide a clean slate to cut debt, gain flexibility, reinvest in new products and growth, and ultimately even return value to shareholders through potential buybacks or dividends. Brand partner numbers were shaky but showed signs of stabilization due to recent recruiting contests and promotions. Forward-looking plans assumed that, with the key transaction, normal operations and optimism would return.

Q1 2026 The company’s story has shifted fundamentally to one of crisis management. Optimism has been replaced by realism and a defensive posture: both management and investors are laser-focused on immediate existential risks—mainly whether the “make-or-break” building sale will close and, if not, what the backup plan is. The brand partner base is eroding much faster than before, and there is less confidence that stabilization is near. Financial messaging is about limiting downside rather than striving for upside. Management is now answering questions about governance alignment and what happens in failure scenarios, rather than painting an aspirational picture. The future is contingent, uncertain, and largely in the hands of external events.

Final Takeaway

Educational Development Corporation is in a restructuring/stabilization phase, highly dependent on executing an asset sale to reset its balance sheet. Management has tactical plans in place if the sale falters, but organic growth challenges and salesforce attrition are notable drags. The business model faces headwinds from a shrinking sales base and operational uncertainties, while management signals a measured, slow turnaround at best. Investors should closely track the sale process and look for proof of revenue and partner stabilization before repositioning. Verdict: Hold, pending key catalyst and evidence of sustainable recovery.