Emergent BioSolutions Inc. (NYSE: EBS) – Q3 2025 Earnings

Emergent BioSolutions Inc. (NYSE: EBS) – Q3 2025 Earnings

Earnings Release Date: Oct. 29, 2025

Stock Price: $9.47

Market Cap: $503.8 million

Q3 2025 sales of $231.1 million vs $293.8 million in the prior year

Q3 2025 EPS of $0.91 vs $2.06 in the prior year

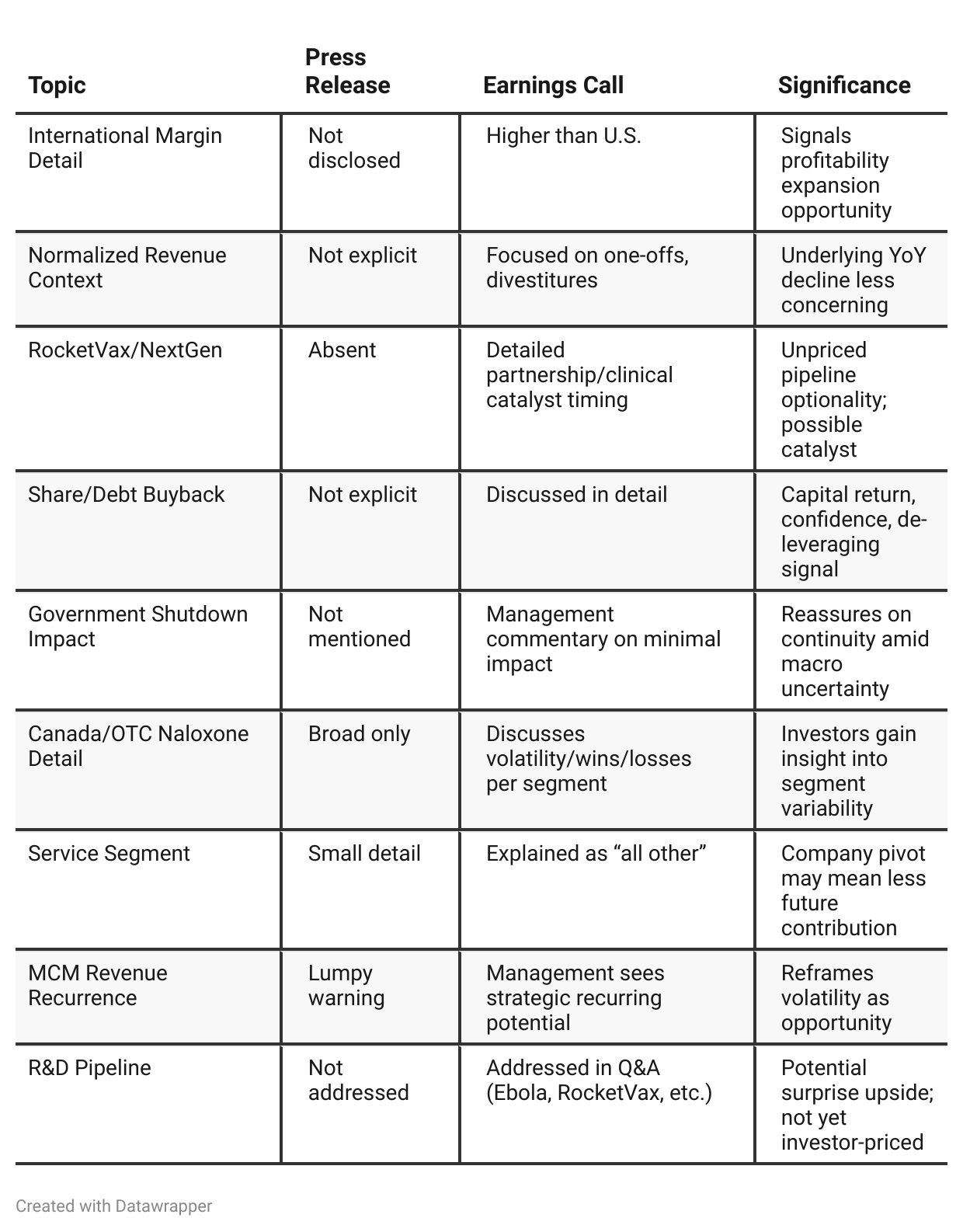

Press Release vs Call Transcript Comparison

Core Biodefense Focus Remains: Company reiterates “public health crisis” positioning, which is a unique moat.

MCM Orders Are Increasingly International: Validates global biothreat and outbreak concern as a long-term tailwind.

Cost Structure Now Rightsized: SG&A and overall opex materially improved post-restructuring/divestitures.

Balance Sheet Strengthening, but Not Yet Optimal: Moving in the right direction; further net debt reduction would be a key future catalyst.

Seasonality/Lumpiness Remain: No structural solution to the “timing” issue, but international multi-year contracts may help smooth cadence.

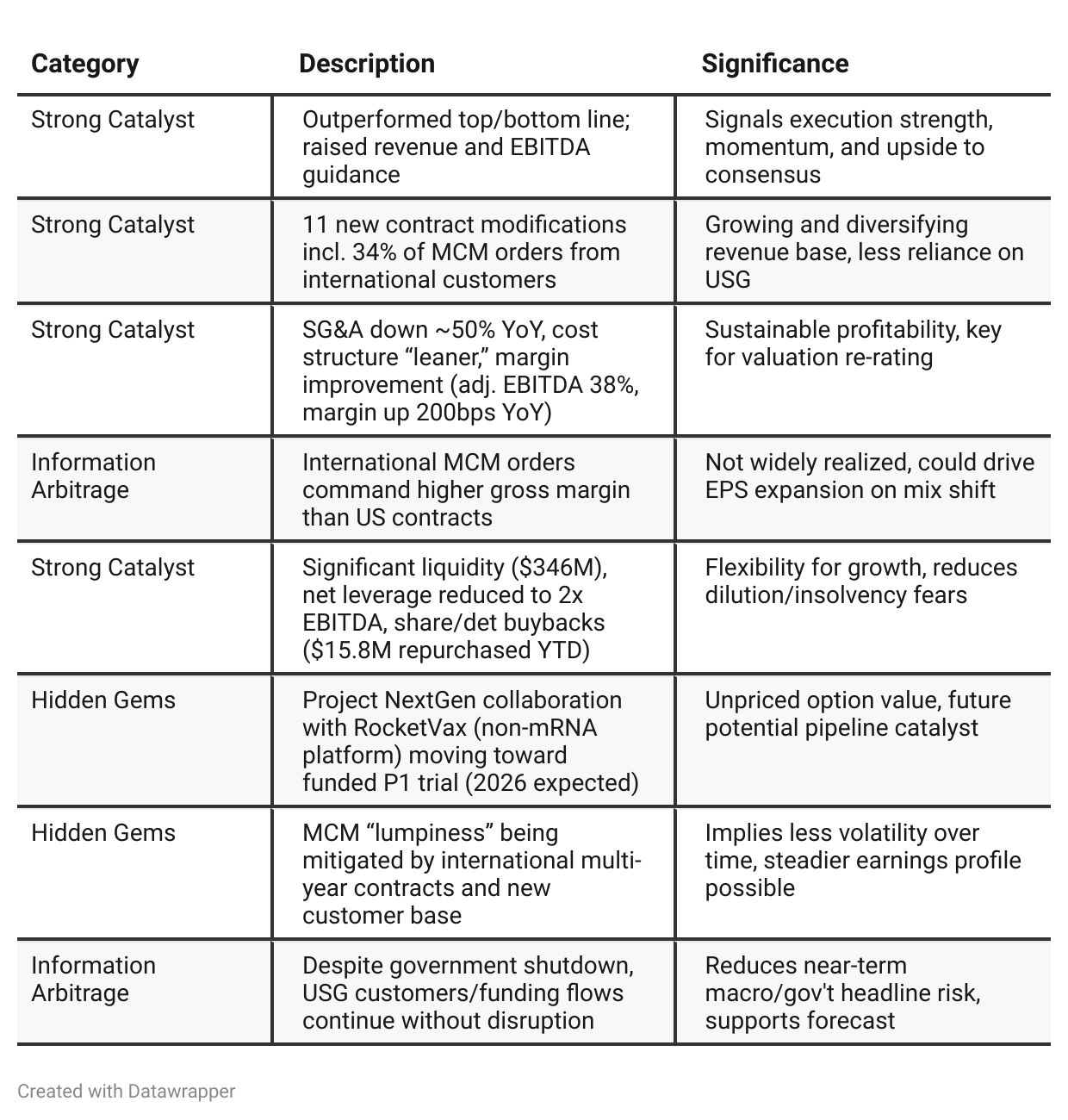

Positive Insights

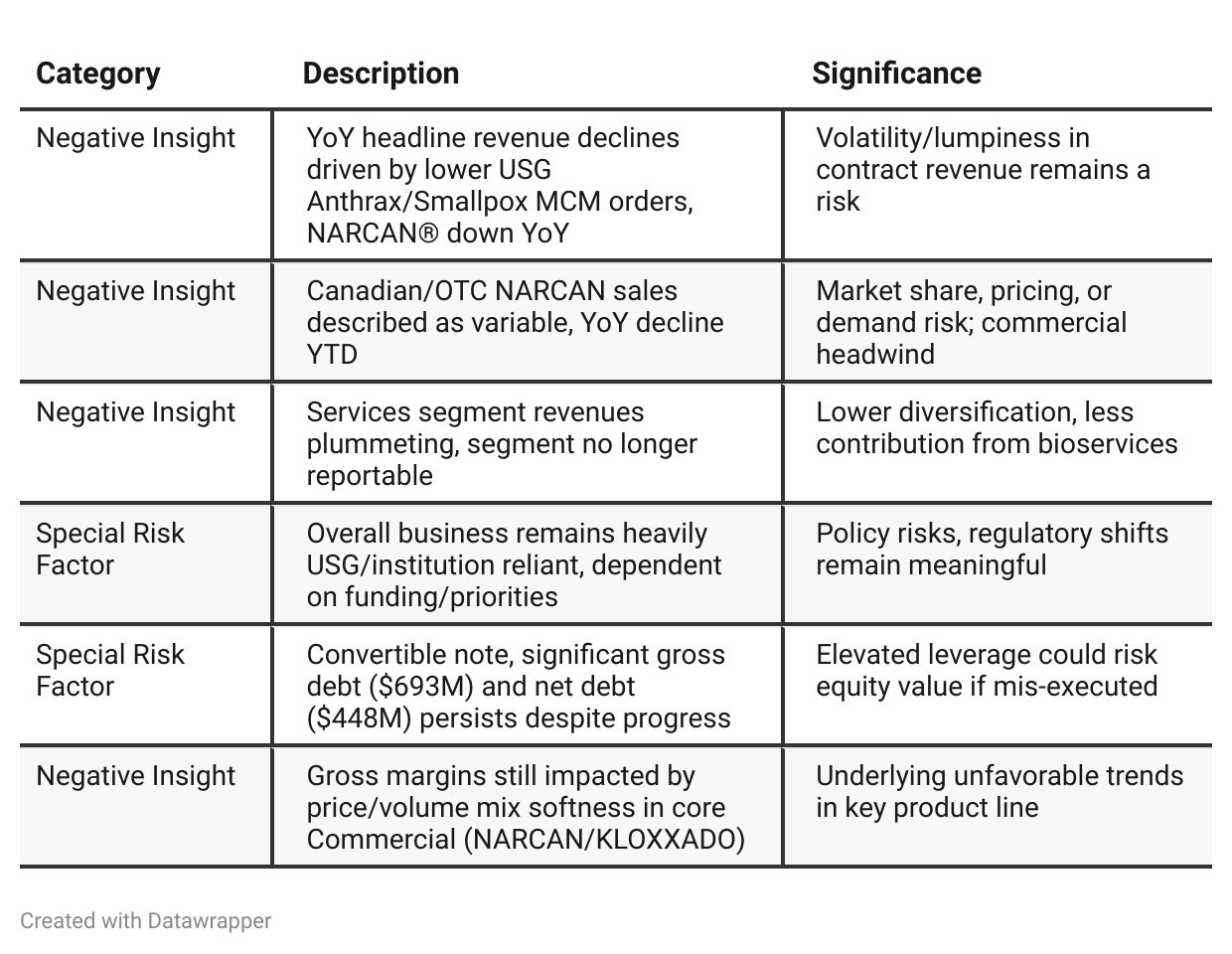

Negative Insights

Tariff Risk

Transcript Coverage: No mention of tariffs, trade wars, or related trade policies in the Q3 2025 call. The closest relevant risk references are:

A North America-based supply chain, US manufacturing, and USMCA-compliant facilities.

No indication of direct supply chain disruption or increased input costs due to tariffs.

No mention of actions to shift production or change sourcing strategies due to tariffs.

International revenue is discussed as a growth vector, not a risk factor related to tariffs.

Conclusion on Tariffs: At present, tariffs or trade policy shifts are not a stated risk or operational hurdle for EBS. If trade policy tensions rise—especially impacting pharmaceutical exports/imports or supply chain inputs—investors should monitor for updates in future disclosures. The company’s focus on US-based manufacturing may be a strategic advantage, providing insulation from some international supply chain/trade policy risks.

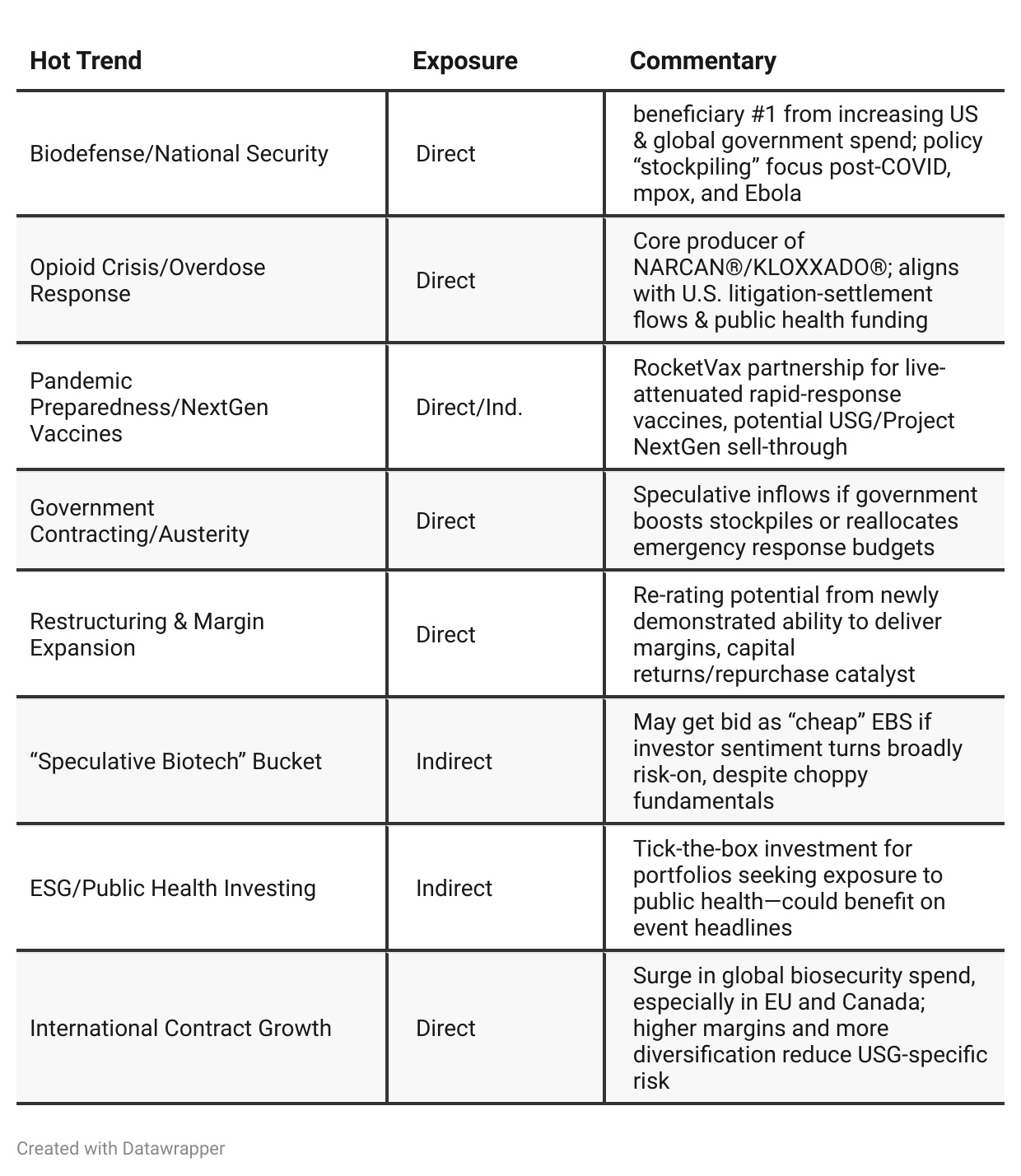

Hot Stock Trends Analysis

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Q2 2025Emergent BioSolutions spent much of Q2 on defense: reporting stabilization and rebound from a tough Q1, stressing liquidity, cost-cutting, and executing a turnaround after prior headwinds. Key topics included regaining market leadership in Narcan after short-term setbacks, demonstrating improving margins, deleveraging, and strategically investing for growth. International expansion appeared, but as an emerging strategy.

Q3 2025

By Q3, EBS’s narrative is much more forward-looking. The company is now exceeding expectations, not just meeting them, and raises both revenue and margin guidance. International expansion is not just a possibility, but a current growth engine—now nearly a third of MCM revenue, delivering higher margins, and positioned as repeatable. The company is proactively buying back shares and paying down debt, emphasizing financial strength. Management’s tone is less defensive, more confident, and the storyline has shifted from repair/recovery to outperformance, growth, and value creation. All this while maintaining mission focus and preparing to capitalize on pipeline/inorganic opportunities.

Year-over-year comparison

Q3 2024 was about stabilization and laying the groundwork for a genuine turnaround. The company defended its necessity, highlighted debt refinancing and asset sales, and stressed its mission in public health and defense. Caution was palpable, but optimism was building as cost-cutting and new contracts hinted at a foundation for future growth.

By Q3 2025, the narrative is one of execution and emerging outperformance. EBS is now confidently raising guidance, deploying capital to buy back shares and debt, and leveraging international expansion and new product partnerships to secure future growth. Margin expansion and cash flow are at the forefront, and macro or political risks are minimized by delivering results through uncertainty. Management’s messaging is assertive, customer base and profitability are broader and more robust, and the company is signaling it’s moved from “survive and stabilize” to “grow and lead.”

Final Takeaway

Emergent BioSolutions (EBS) is in a turnaround/restructuring phase with improving financial discipline, strong international MCM growth, and visible margin expansion. Execution risk and contract volatility remain, but the company is better positioned than in prior years. Key drivers to watch: repeat international orders, commercial portfolio recovery, and pipeline developments. Verdict: HOLD—upside if momentum continues, but risks from contract lumpiness and commercial mix require more proof before upgrading.