DAVIDsTEA Inc. (TSXV:DTEA) (OTC:DTEAF) – Q2 2025 Earnings

DAVIDsTEA Inc. (TSXV:DTEA) (OTC:DTEAF) – Q2 2025 Earnings

Earnings Release Date: Sep. 16, 2025 (all figures in Canadian dollars)

Stock Price: $1.09

Market Cap: $29.4 million

Q2 2025 sales of $11.1 million vs $11.1 million in the prior year

Q2 2025 adjusted loss per share of ($0.06) vs ($0.04) in the prior year

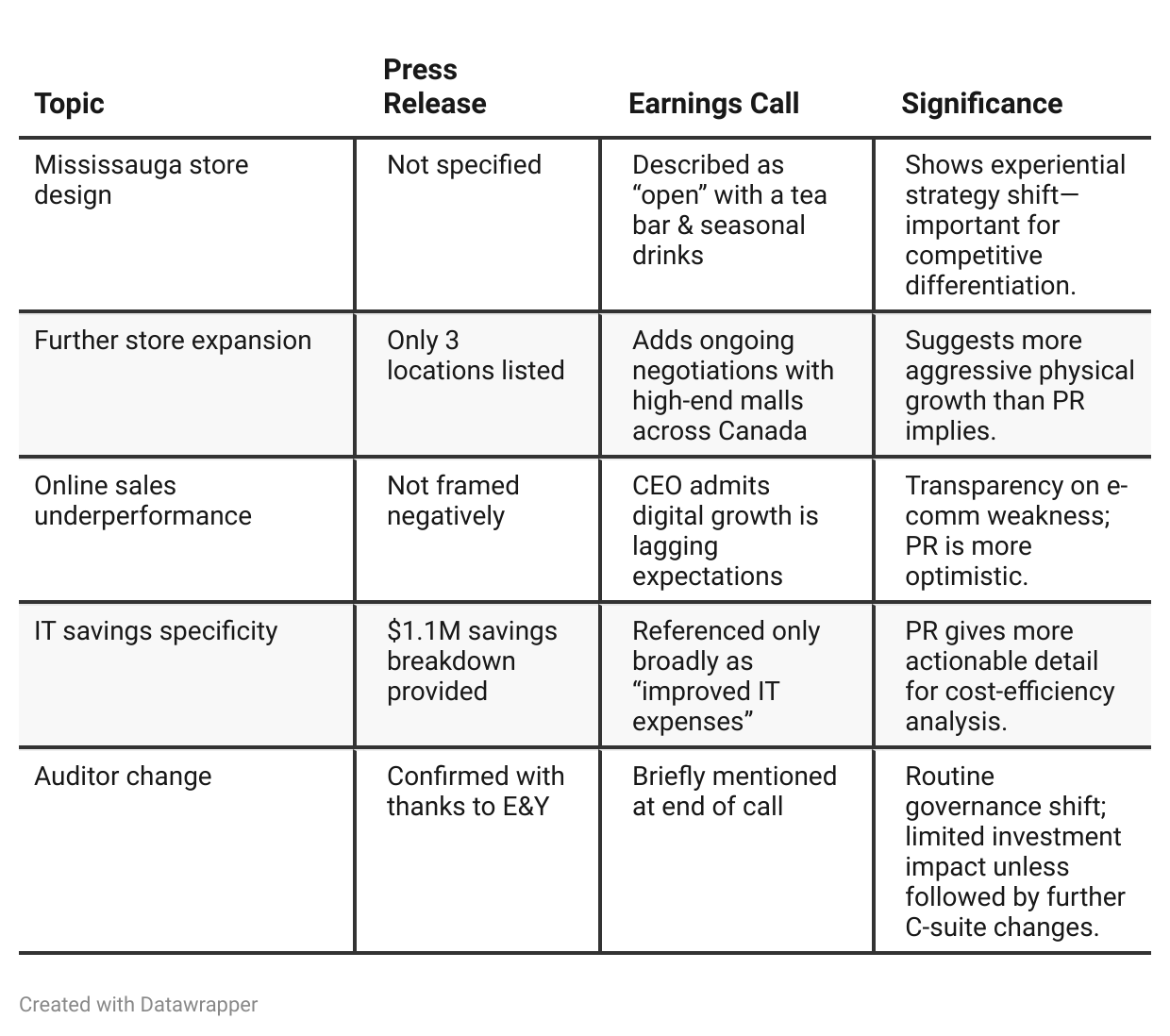

Press Release vs Call Transcript Comparison

While the press release presents a stable, cautiously optimistic snapshot of Q2, the earnings call adds critical strategic texture — including more aggressive store expansion plans, deeper commentary on underwhelming online performance, and a clear experiential pivot with the new Mississauga location.

For investors, the call reveals both the conviction and risk behind DAVIDsTEA’s retail-centric rebound thesis. The divergence between omnichannel challenges (particularly in e-commerce) and capital commitments (new stores, marketing) means execution in Q3/Q4 is make-or-break.

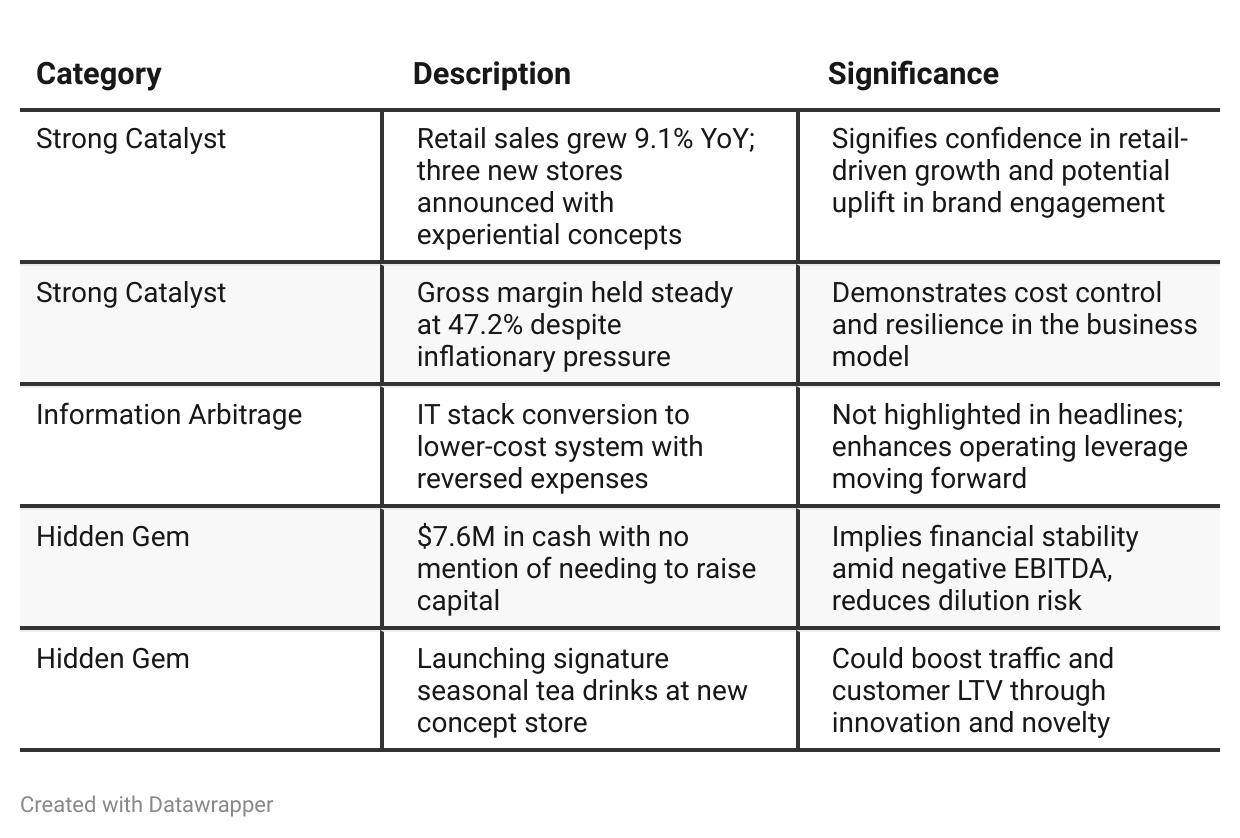

Positive Insights

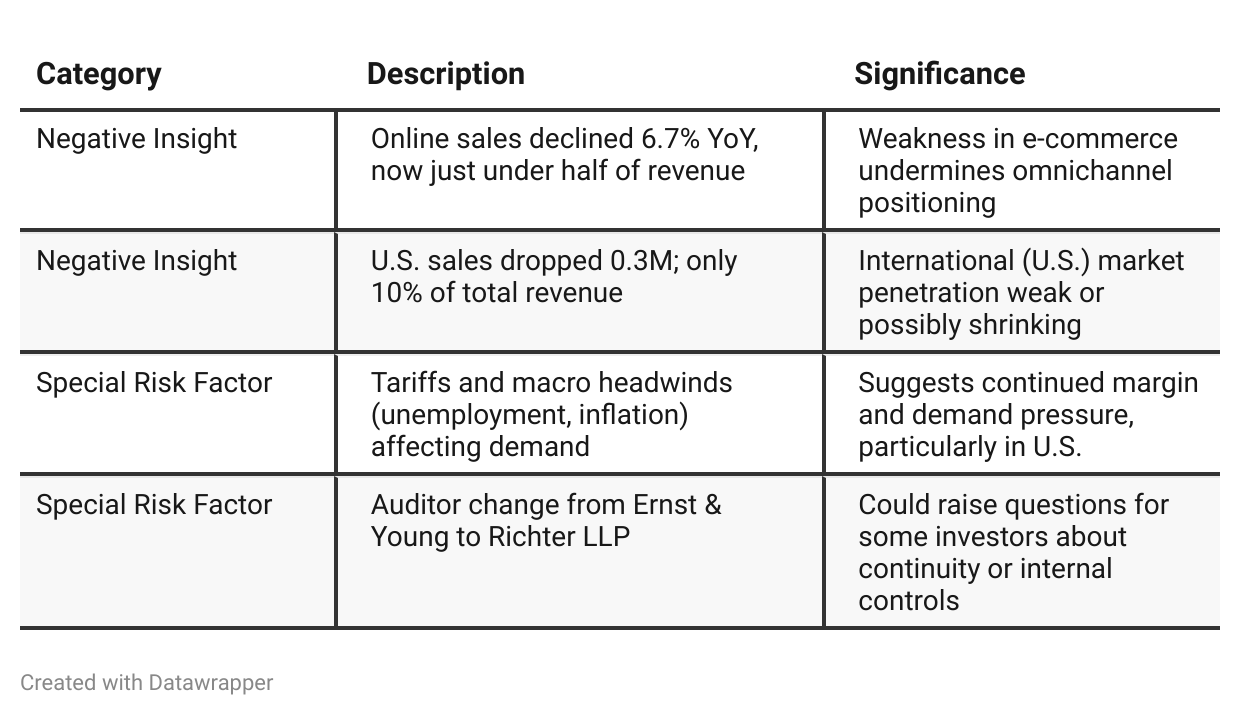

Negative Insights

Tariff Risk

Mention: Management highlighted that U.S. tariffs are part of the macro headwinds affecting business, especially e-commerce sales.

Impact: Cited as a drag on online revenues, particularly in the U.S., where sales fell 0.3M YoY.

Mitigation: No specific mitigation steps (e.g., supply chain shifts, pricing changes) were disclosed in the call.

Forward-Looking View: Management framed the impact as external and temporary but did not provide projections or strategies to offset future tariff-related costs.

Tariff Takeaway: Tariff headwinds are pressuring U.S. performance, especially online. Lack of mitigation details introduces risk. Investors should monitor future disclosures for adaptation strategies.

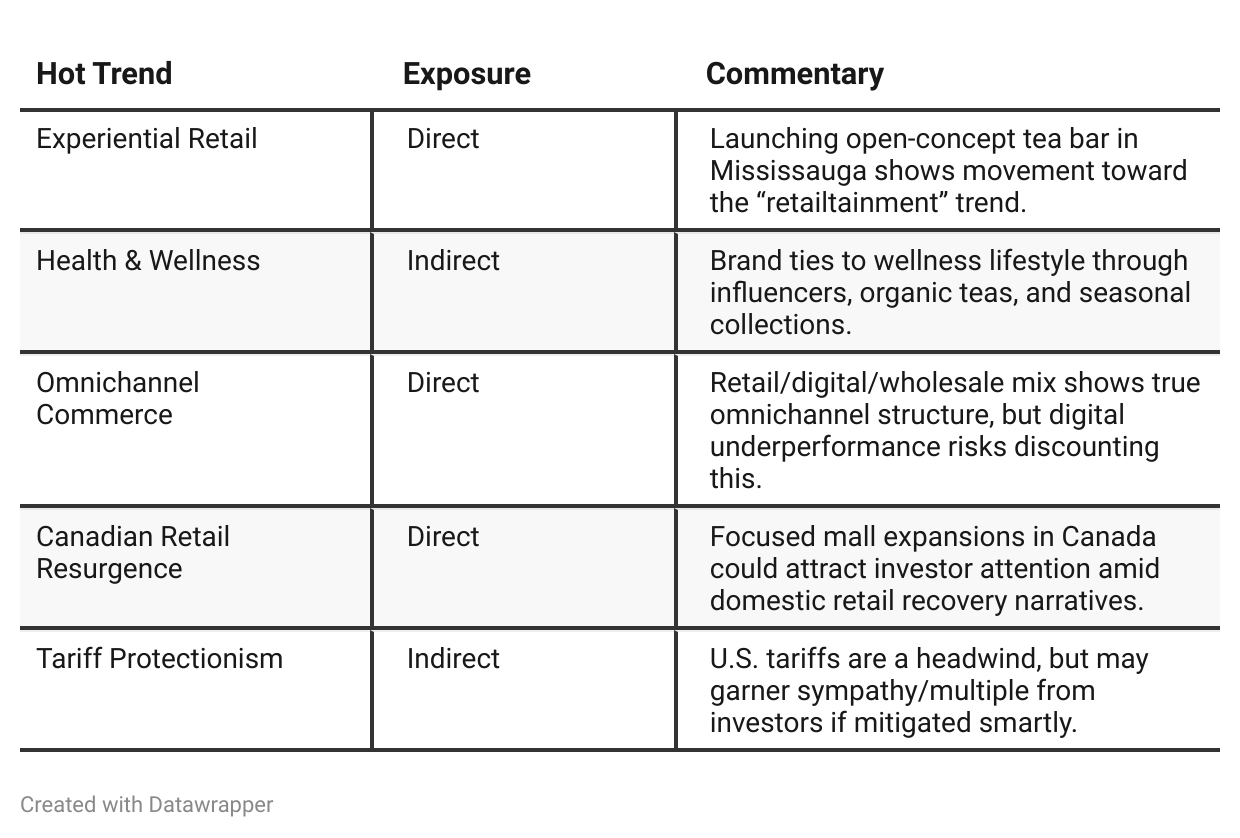

Hot Stock Trends Analysis

Previous Earnings Call

Quarter-over-quarter comparison

Between Q1 and Q2 2025, DAVIDsTEA shifted its tone from celebrating turnaround milestones to preparing for the next growth phase. In Q1, the company emphasized margin recovery, cost control, and early signs of sustainable profitability driven by operational discipline.

By Q2, the narrative matured into a forward-looking strategy centered on experiential retail expansion, brand marketing, and optimizing the peak holiday season.

While challenges like sluggish e-commerce and macro pressures remain, DAVIDsTEA appears committed to leveraging its physical stores and branding efforts to deepen customer loyalty and drive long-term profitability.Year-over-year comparison

From Q2 2024 to Q2 2025, DAVIDsTEA shifted from a cost-cutting and operational recovery story to a retail-led brand marketing and expansion narrative. In 2024, the company was focused on preserving cash, boosting gross margins, and surviving through lean operations.

By 2025, while sales growth had plateaued, the company emphasized long-term growth via flagship store investments, a refreshed brand presence, and experiential consumer engagement. The optimism remained, but it was tempered by slower online growth and a more complex macro environment.

Overall, the narrative evolved from “back on track” to “building for the future.”

Final Takeaway

DAVIDsTEA is in a stabilization phase, focusing on retail footprint growth and brand marketing to drive an omnichannel turnaround.

While store-level momentum and cost discipline offer upside, e-commerce weakness and U.S. softness present headwinds. Execution on store expansion ROI and margin leverage will be critical for future performance.

Verdict: HOLD, with potential upside if retail expansion proves accretive and online trends reverse.