Dirtt Environmental Solutions Ltd (OTCQX: DRTTF/DRT.TO) – Q2 2025 Earnings

Dirtt Environmental Solutions Ltd (OTCQX: DRTTF/DRT.TO) – Q2 2025 Earnings

Earnings Release Date: Jul. 30, 2025

Stock Price: $0.87

Market Cap: $166.6 million

Q2 2025 sales of $38.9 million vs $41.2 million in the prior year

Q2 2025 EPS of $(0.03) vs $0.00 in the prior year

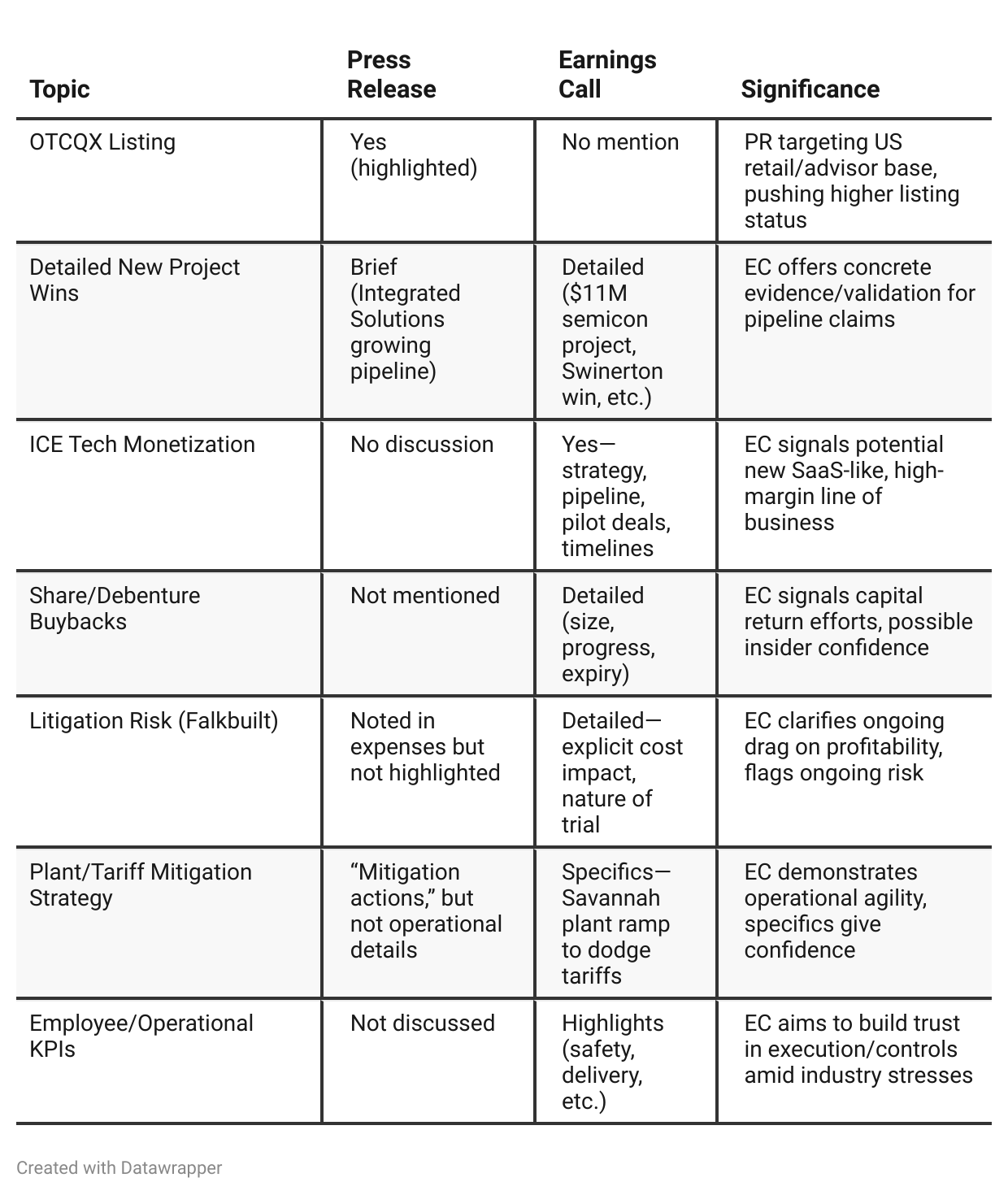

Press Release vs Call Transcript Comparison

Forward-Looking Statements: The PR contains extended forward-looking caveats and references to risk sections in SEC filings—standard but underscores DIRTT’s awareness of litigation, tariff, and macro risk.

Financial Disclosures: PR is more formal and SEC/TSX-compliant, with explicit non-GAAP reconciliations; EC is more narrative, focusing on management’s thought process and tactical moves.

Product Innovation: Both documents emphasize the new one-hour fire-rated wall, but the EC gives richer insight on new office pods and product “unbundling,” demonstrating more flexible/savvy product strategy matched to demand trends.

Cash Cushion vs. Debt Maturity: Both sources note cash burn and upcoming debt maturity; PR is slightly more direct about potential need to refinance, signaling a watch item for investors.

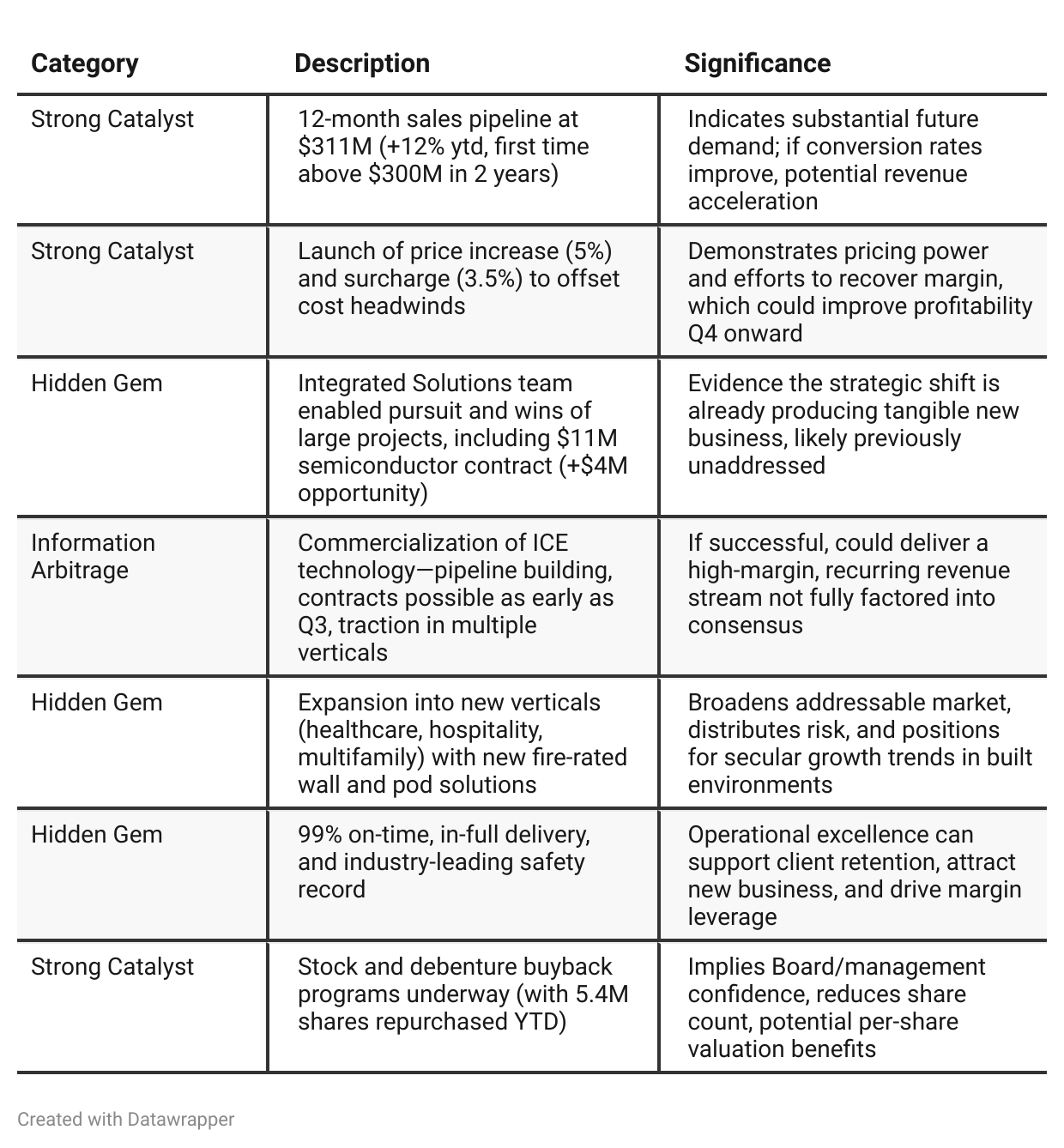

Positive Insights

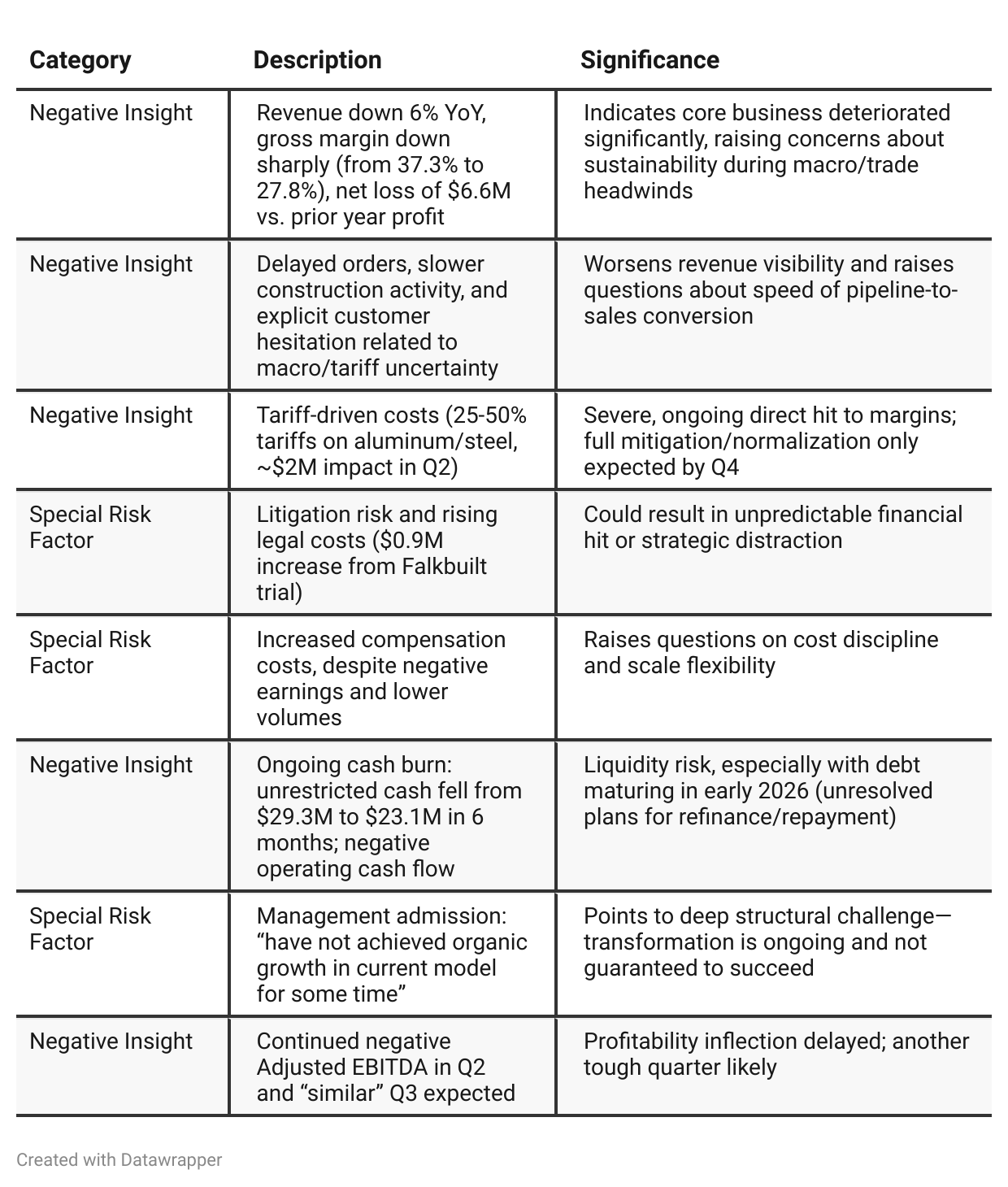

Negative Insights

Tariff Risk

Material Margin Impact: Newly increased U.S. tariffs on Canadian aluminum and steel (~50%) directly reduced gross margins by over 5% of revenue, with ~$2 million in quarterly costs.

Pipeline Delay & Revenue Deferral: Customers hesitated to place orders and delayed projects because of tariff uncertainty, causing both revenue and pipeline conversion to slow.

Mitigation Efforts: DIRTT is shifting more aluminum processing to its U.S.-based Savannah plant, raising prices by 5%, and adding a 3.5% tariff surcharge. Benefits of these actions should be realized gradually into Q4.

Ongoing Headwind: Tariff pressures are expected to persist through Q3, with management targeting full mitigation and margin recovery by Q4 2025.

Risks Remain: Prolonged or further increases in tariffs, or weak customer adaptation, could result in longer-term earnings pressure and continued unpredictability in project flow.

Bottom line: Tariffs are significantly hurting DIRTT’s profitability and revenue timing. Management is actively mitigating, but investors should monitor Q4 results and evidence of margin recovery to gauge true effectiveness.

Previous Earnings Call

Quarter-over-quarter comparison

Q1 2025: DIRTT is restructuring against a backdrop of macro and tariff uncertainty. Management is upbeat about innovation, customer wins, lean process rollout, and a healthier pipeline. The major message: we’re tightening the ship, diversifying, and laying the groundwork for scalable growth, even as we withdraw guidance in light of volatility.Q2 2025: The tariffs bite hard. Financial performance deteriorates—revenue falls, margins erode, the company posts a sizable loss and negative cash flow. There’s realism about industry-wide challenges and the stickiness of order delays. However, the narrative turns tactical: DIRTT is not only describing new product launches and expanding its pipeline, but also naming individual large project wins and outlining concrete steps to offset tariff pain and keep the turnaround alive. The pipeline is at a two-year high, and ICE tech may soon add new SaaS-style revenue, but getting to profitability will require execution and improved macro.

Year-over-year comparison

2024: DIRTT paints a picture of turnaround success. The company moves from struggle into a period of stability, outperformance (positive earnings, free cash flow, reduced debt), improved operating metrics, and growing relevance for large clients and new partners. Strategy is working, producing both short- and long-term improvements. Optimism is palpable.

2025: That narrative is sharply interrupted by macro and tariff shock. Even with a record sales pipeline and ongoing product/technology advances, DIRTT is forced onto the defensive: revenues and profits fall, margins are squeezed, and visibility is clouded. Management pivots to tactical survival—cost actions, operational adjustments, and a more granular narrative on pipeline specifics and ICE monetization. The story becomes one of endurance and adaptation: “hold on through headwinds; mitigate, don’t just grow; and set up for a hopefully stronger post-shock recovery.”

Final Takeaway

DIRTT Environmental Solutions is executing a turnaround in the face of intense macro and industry challenges, led by new products, integrated solutions, and a major commercial push around ICE technology. Tariff headwinds, negative cash flow, and litigation risk continue to weigh heavily, but a record sales pipeline and early strategic wins suggest underlying business momentum. Execution on tariff recovery, pipeline conversion, and balance sheet stabilization will define outcomes over the next two quarters. Hold (negative bias), watch closely for Q4 inflection.