DHI Group, Inc. (NYSE: DHX) – Q2 2025 Earnings

DHI Group, Inc. (NYSE: DHX) – Q2 2025 Earnings

Earnings Release Date: Aug. 6, 2025

Stock Price: $2.81

Market Cap: $127.4 million

Q2 2025 sales of $32.0 million vs $35.8 million in the prior year

Q2 2025 EPS of $0.07 vs $0.06 in the prior year

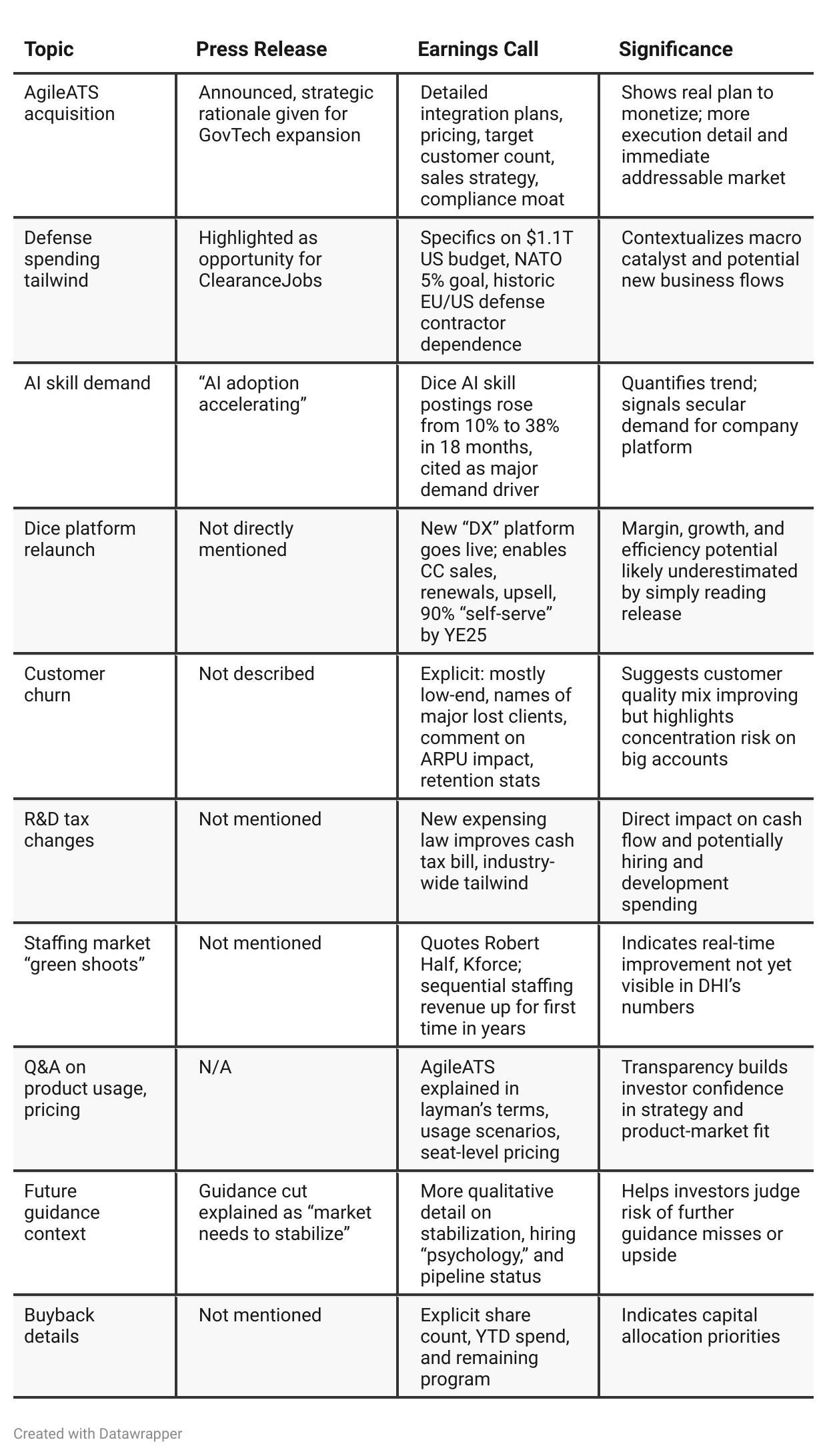

Press Release vs Call Transcript Comparison

Call provides strategy/tactical depth: The earnings call offers much more granular detail on customer churn, mix, new product launches, and actual execution steps, which are glossed over in the press release.

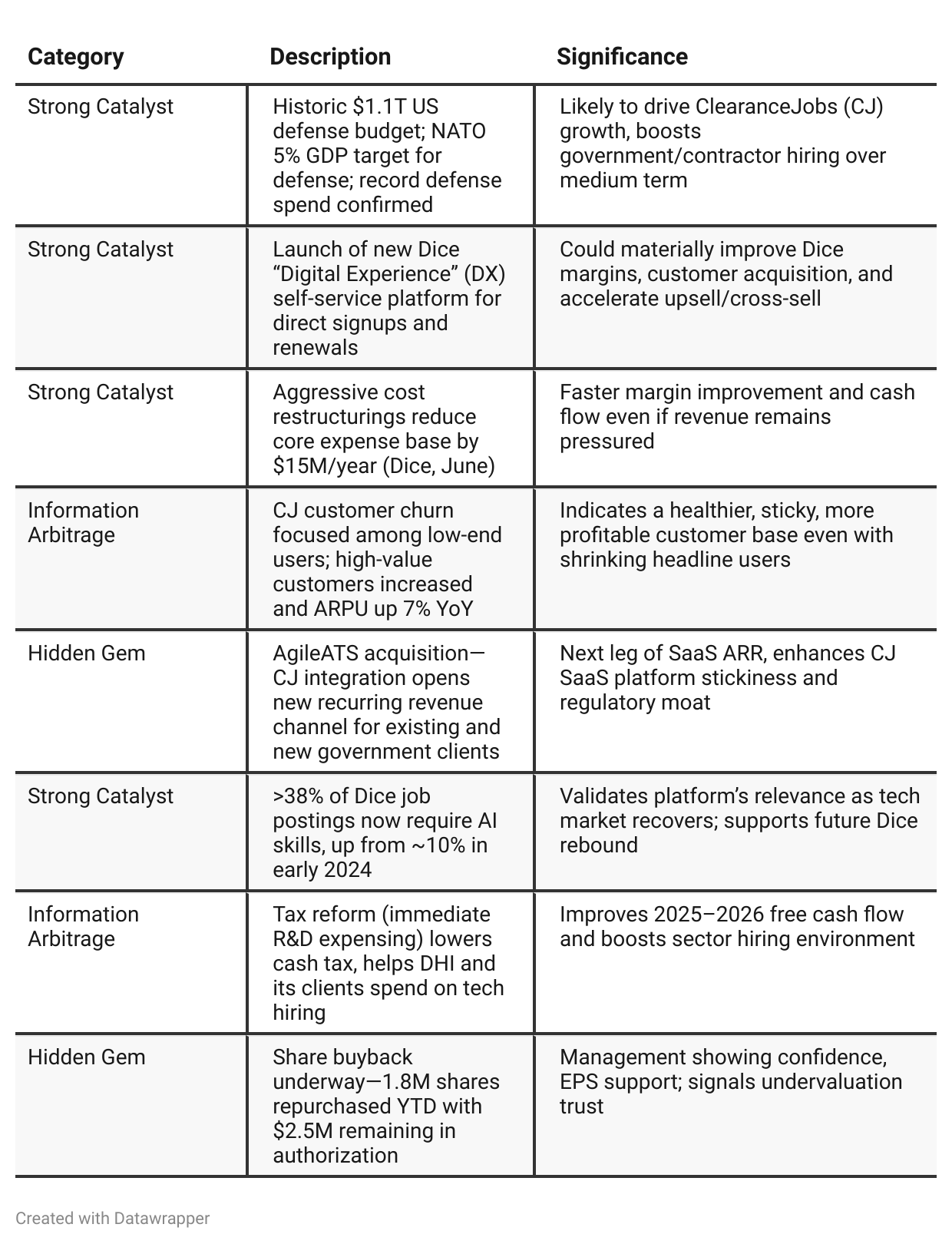

ClearanceJobs is the engine: It remains highly profitable and resilient, while Dice continues to face headwinds and concentration risk.

Customer base quality is improving: Churn is mostly among lower-value clients; ARPU and retention are better among remaining clients.

Cost actions meaningful but ongoing: Savings from restructurings are crucial for maintaining margins but repeated restructurings indicate past operational misalignment.

New catalysts (AgileATS, Dice DX platform): Both appear as long-term growth/margin opportunities but need sound execution.

Liquidity manageable but not flush: Cash balance is low but offset by low leverage; watch for further deterioration if revenue misses persist.

Positive Insights

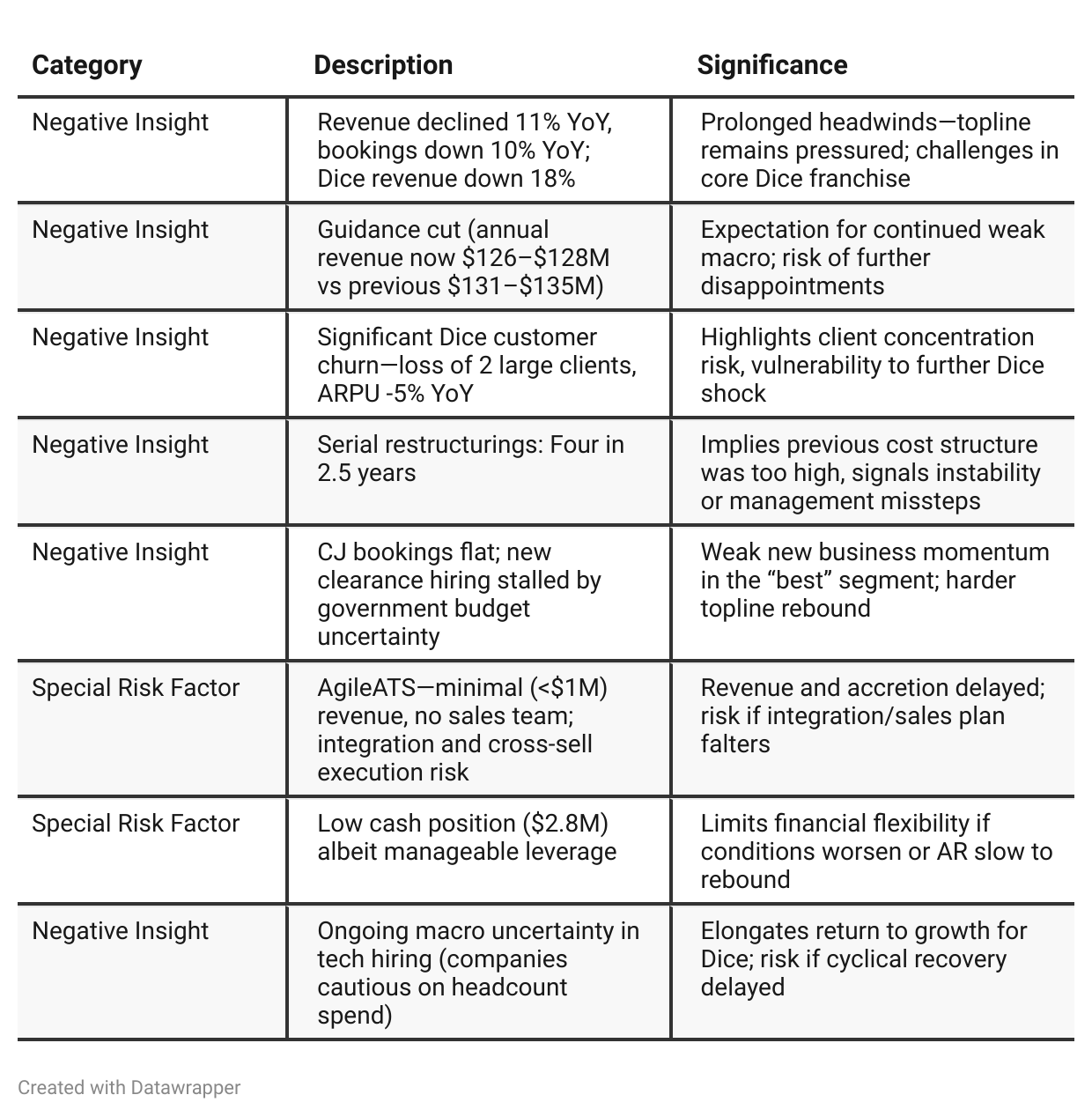

Negative Insights

Tariff Risk

No mention of U.S. tariffs or trade policy impacts was found in the transcript. There is no direct discussion of supply chain costs, market access, or competitive challenges from tariffs. Investors should monitor future calls for any change related to government contracting supply chains or global defense developments that could introduce trade friction or tariff risk.

Sentiment Analysis

The overall sentiment toward $DHX is bullish. Multiple investors highlight recent upward momentum and brand strength, with some mentioning successful trading strategies that capitalized on both downward and upward moves. Positive remarks note DHX’s market leadership, reputation in tech and security recruiting, and growth potential driven by strategic acquisitions. Projected gains and confidence in the company’s business model further reinforce optimism. There is some technical trading caution, but the prevailing sentiment is confidence in future upside.

Previous Earnings Call

Quarter-over-quarter comparison

At the start of 2025, DHI Group’s narrative was defensive and operationally focused—cost controls, restructurings, and segment alignment were at the forefront, while management waited for uncertain macro and government budget dynamics to clear. As the year progressed to Q2, with several quarters of cost actions taken, the company’s message evolved to highlight stabilization in tech hiring, more actionable green shoots in staffing, and—most notably—a shift toward product and growth initiatives. New strategic investments (AgileATS, Dice DX) now take center stage as bets on future growth and margin leverage. Although revenue growth remains elusive and guidance is lowered, there’s increased confidence in margin sustainability, free cash flow, and the structural positioning of CJ within the defense hiring supercycle. Management is less focused on survival and more on capturing upside as market conditions improve, with the execution of new technology platforms as the next litmus test.Year-over-year comparison

Between Q2 2024 and Q2 2025, DHI Group’s narrative evolved from cautious stabilization and product improvement amid macro headwinds, to one of structural boldness, margin-first execution, and proactive adaptation. In 2024, the message was about hunkering down—retaining clients, launching new packages, improving product stickiness, and waiting for tech hiring to normalize. By 2025, the company is taking more aggressive steps: acquiring and integrating new platforms (AgileATS), transforming customer onboarding and upsell (Dice DX), and explicitly aiming for higher-value, more resilient clients. While revenue has remained pressured by a persistent macro malaise, cost discipline and strategic repositioning are yielding stronger margins and preparing DHI to capitalize on the recovery in AI and defense-driven hiring. The company is moving from “optimizing to survive” toward “architecting for the upswing,” with a sharper focus on proactive strategy, execution, and profit resilience.

Final Takeaway

DHI Group is in a restructuring-and-repositioning phase, leaning on strong profitability and retention in ClearanceJobs while absorbing top-line and customer churn pain in Dice. Management is executing deep cost cuts and launching product innovations to return to growth, but a material rebound hinges on defense spending roll-out, macro tech hiring normalization, and successful AgileATS integration. Investors should focus on Dice stability, defense-driven CJ growth, and actual recurring revenue delivery from new initiatives. Verdict: Hold—potential upside on execution and macro recovery, but risks remain if recovery stalls or new plays disappoint.