Journey Medical Corporation (NASDAQ: DERM) – Q3 2025 Earnings

Journey Medical Corporation (NASDAQ: DERM) – Q3 2025 Earnings

Press release and earnings call link

Earnings Release Date: Nov. 12, 2025

Stock Price: $9.05

Market Cap: $210.7 million

Q3 2025 sales of $17.6 million vs $14.6 million in the prior year

Q3 2025 EPS of ($0.09) vs ($0.12) in the prior year

Journey Medical Corporation (NASDAQ: DERM) is a commercial-stage dermatology pharmaceutical company focused on marketing and selling FDA-approved prescription drugs that treat common skin disorders. Its flagship product, Emrosi™ (minocycline HCl MR capsules), is a next-generation oral treatment for rosacea, launched in April 2025.

Revenue Drivers: Primarily driven by Emrosi and Qbrexza® (hyperhidrosis treatment). Legacy brands include Accutane, Amzeeq, and Zilxi, which are now declining due to generic competition.

Customer Base: U.S. dermatologists and their patients; largely a specialty pharma commercial model with targeted physician engagement.

Market Position: An emerging mid-tier dermatology player, leveraging a focused salesforce and a lean commercial infrastructure (low R&D exposure, high marketing efficiency).

Recent Trajectory: Revenue growth of 21% YoY (to $17.6M), led by Emrosi’s accelerating adoption. Despite continued net losses, Adjusted EBITDA turned positive ($1.7M).

Strategic Focus: Driving Emrosi adoption through payer access expansion and prescriber conversion, stabilizing legacy product revenues, and achieving sustainable EBITDA positivity by Q4 2025.

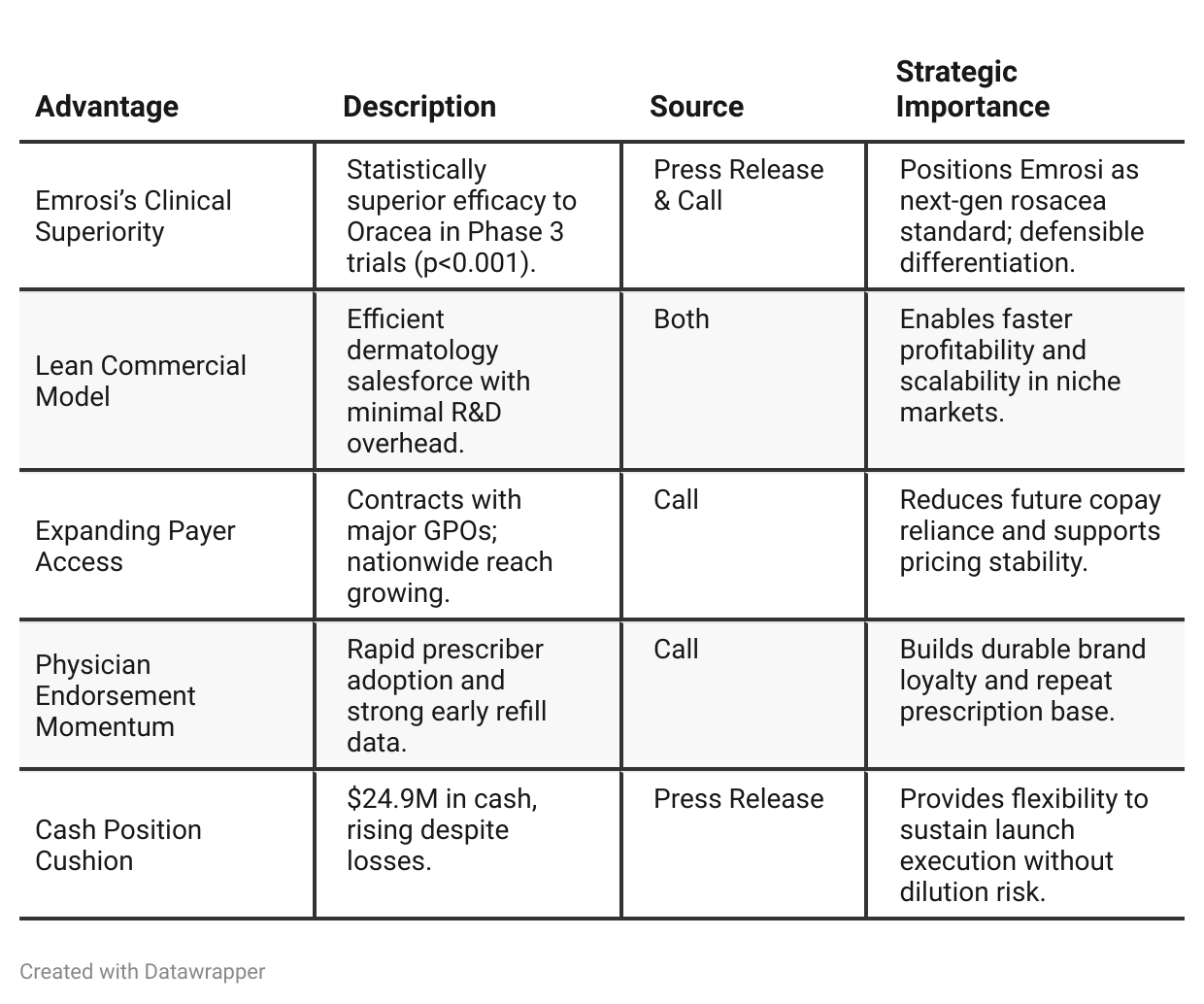

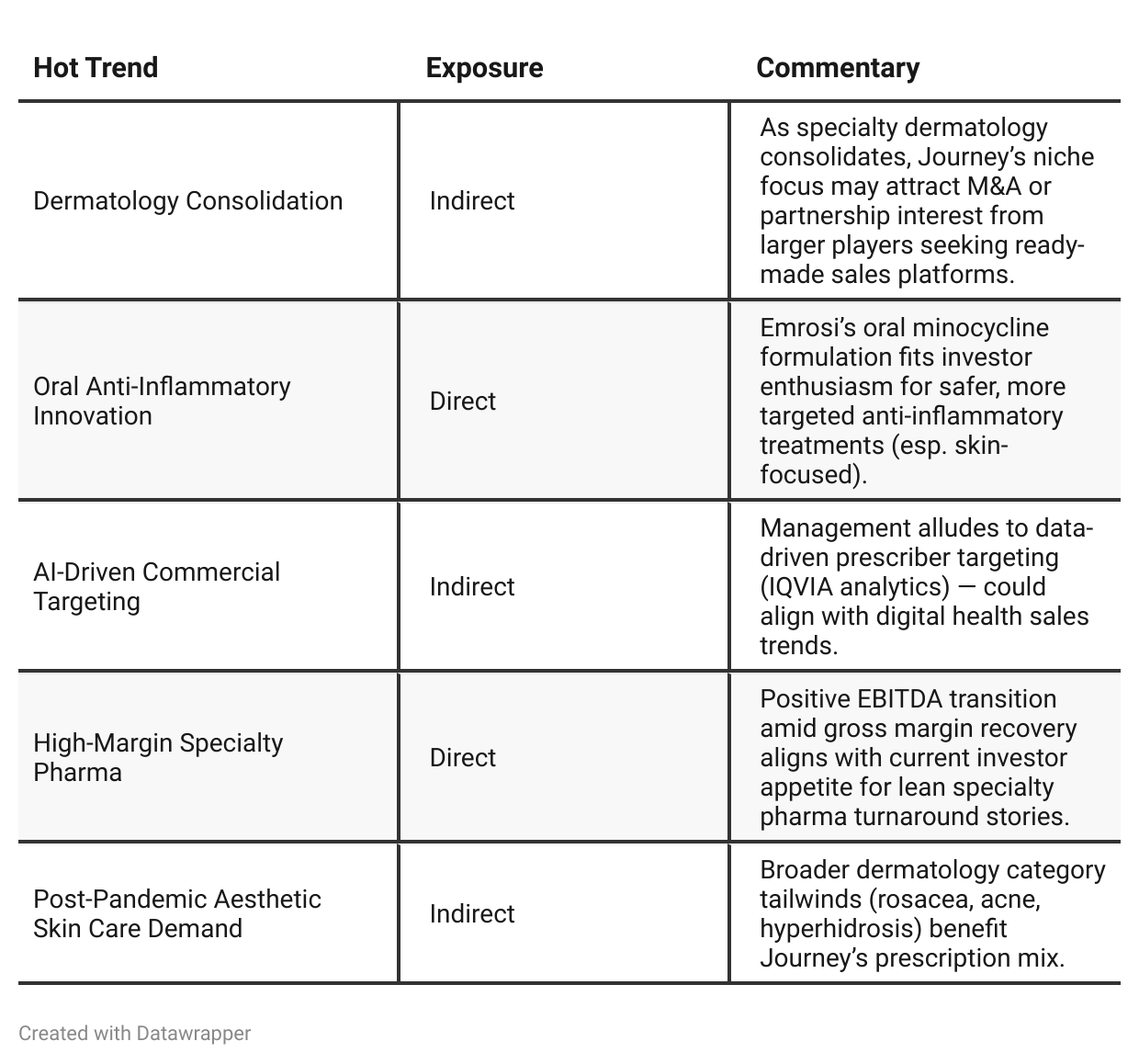

Competitive Advantage Insights

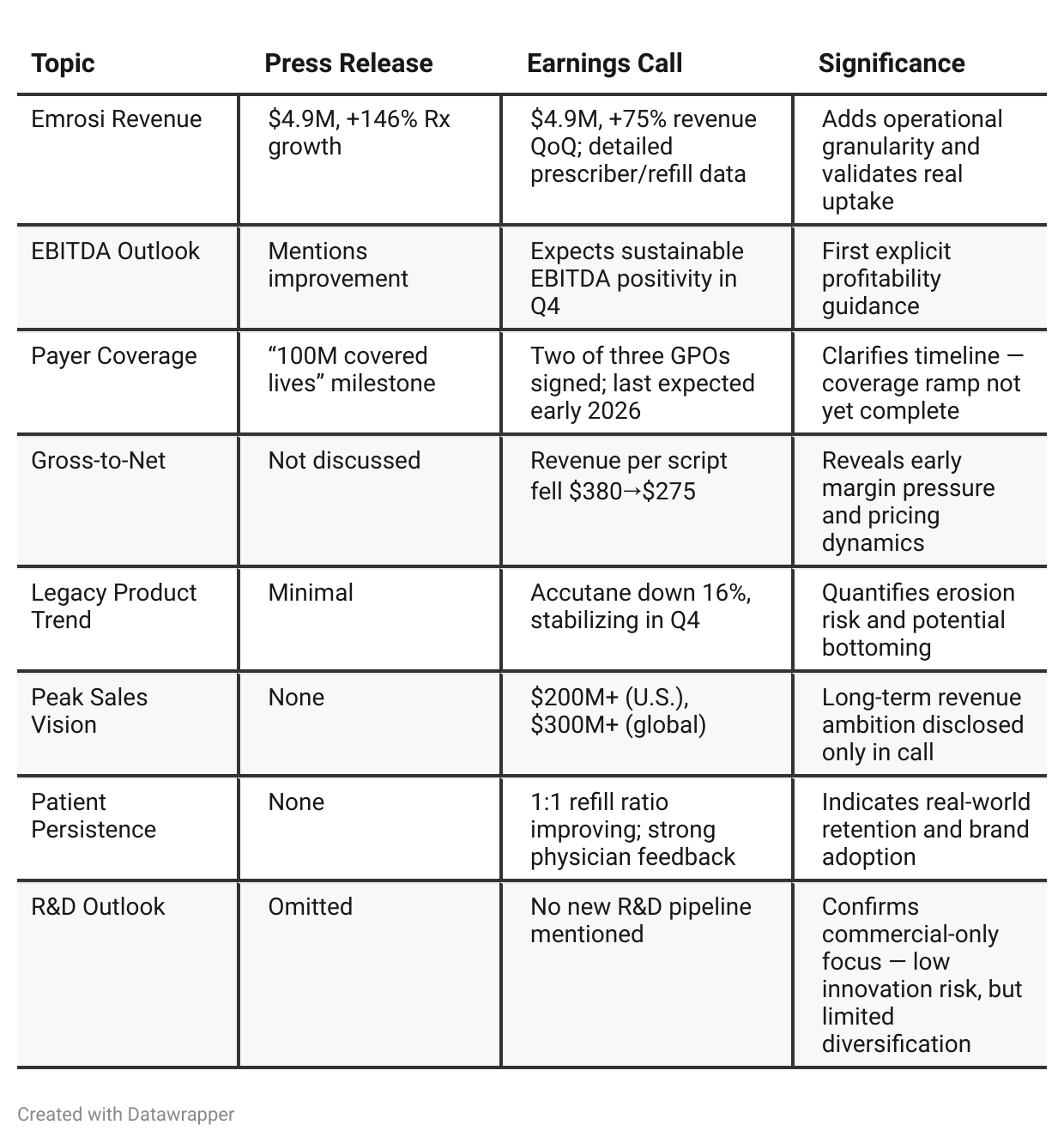

Press Release vs Call Transcript Comparison

The call’s Q&A segment surfaces early payer friction and net price dilution — essential for cash flow modeling.

Management’s tone implies measured optimism: execution confidence without over-promising, which may build credibility after earlier “turnaround” quarters.

The absence of new product pipeline discussion signals full reliance on Emrosi for growth — both a focus strength and concentration risk.

Conference visibility (1,800 prescribers at Fall Clinical) hints at effective brand awareness among key decision-makers — underappreciated in the press release.

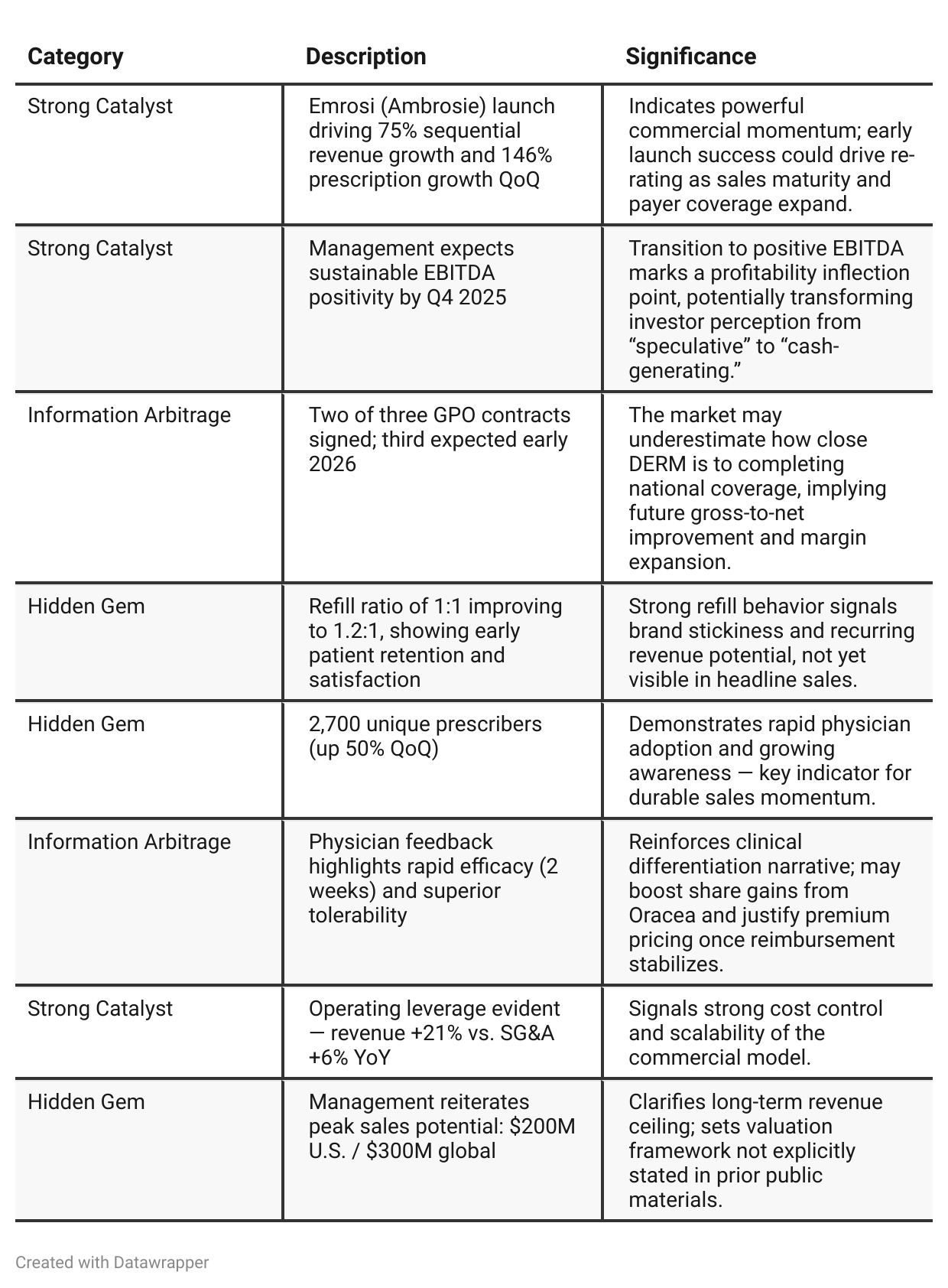

Positive Insights

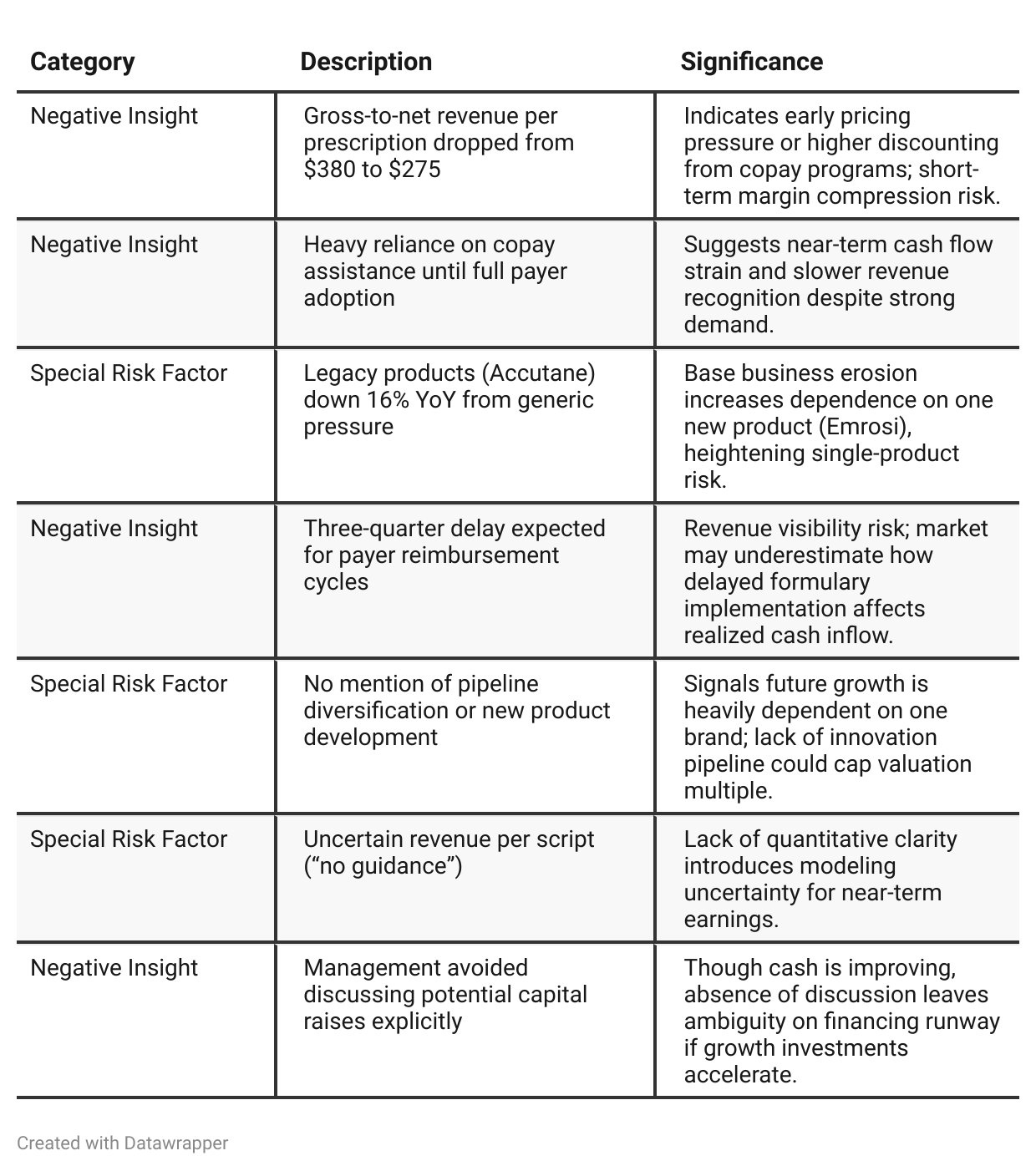

Negative Insights

Investor Underappreciation Signals

✅ Prescription Refill Momentum — Early data showing a 1:1 refill-to-new Rx ratio improving to 1.2:1 indicates real patient retention; investors may overlook this as a leading indicator of recurring revenue once payer coverage stabilizes.

✅ Operating Leverage Inflection — SG&A up only 6% YoY while revenue grew 21%; this structural cost discipline could drive sharp EBITDA upside once Emrosi reaches scale, a fact buried under GAAP losses.

✅ Delayed Payer Impact = Deferred Margin Upside — Investors may misread current gross-to-net compression as pricing weakness, but management expects normalization within three quarters as coverage expands to all GPOs.

✅ Prescriber Base Expansion Momentum — Growing from 1,800 to 2,700 unique prescribers within one quarter is unusually fast for dermatology; the snowball effect in Q1–Q2 2026 could meaningfully re-rate growth expectations.

✅ Legacy Product Stability — Despite competition, Accutane’s stabilization in early Q4 and Qbrexza’s modest sequential growth suggest the base business may support positive EBITDA even before full Emrosi maturity.

Tariff Risk

No references to tariffs or U.S. trade policies appear in the transcript. The company’s operations are domestically focused on dermatology pharmaceuticals with U.S.-based commercialization, suggesting minimal direct tariff exposure.

However, investors should remain aware of potential indirect impacts (e.g., API or packaging materials sourced abroad). No mitigation measures or concerns about trade policy were mentioned.

Conclusion: Tariff risk negligible for DERM’s investment case at this stage.

Hot Stock Trends Analysis

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Earlier Narrative (Q2 2025):

Journey Medical positioned itself as an emerging dermatology player proving product-market fit with Amrosi. The tone was highly promotional — highlighting rapid uptake, growing awareness, and impressive coverage wins. The call centered on momentum, visibility, and early success metrics like prescriber growth and gross margin expansion. Investors were encouraged by optimism but lacked operational visibility or financial clarity.Current Narrative (Q3 2025):

The story matured into one of execution discipline and scaling confidence. Management’s tone is steadier, providing more tangible data on refill ratios, payer timelines, and profitability milestones. The focus is now on converting breadth to depth, refining payer integration, and sustaining EBITDA-positive operations.Year-over-year comparison

(No earnings call)

Final Takeaway

Journey Medical (NASDAQ: DERM) is in a growth transition phase, pivoting from launch investment toward sustainable profitability. While Emrosi’s market traction, prescriber expansion, and refill rates highlight accelerating fundamentals, the timing lag in payer adoption and gross-to-net pressure temper near-term optimism. Execution on coverage expansion and cost discipline will define the company’s valuation trajectory through 2026.

Verdict: BUY (with near-term volatility) — upside tied to execution and confirmation of Q4 EBITDA-positive guidance.