DATA Communications Management Corp. (OTCQX: DCMDF) – Q1 2025 Earnings

DATA Communications Management Corp. (OTCQX: DCMDF) – Q1 2025 Earnings

Earnings Release Date: May 12, 2025 (all figures in Canadian dollars)

Stock Price: $1.86

Market Cap: $102.9 million

Q1 2025 sales of $123.7 million vs $129.3 million in the prior year

Q1 2025 adjusted EPS of $0.09 vs $0.08 in the prior year

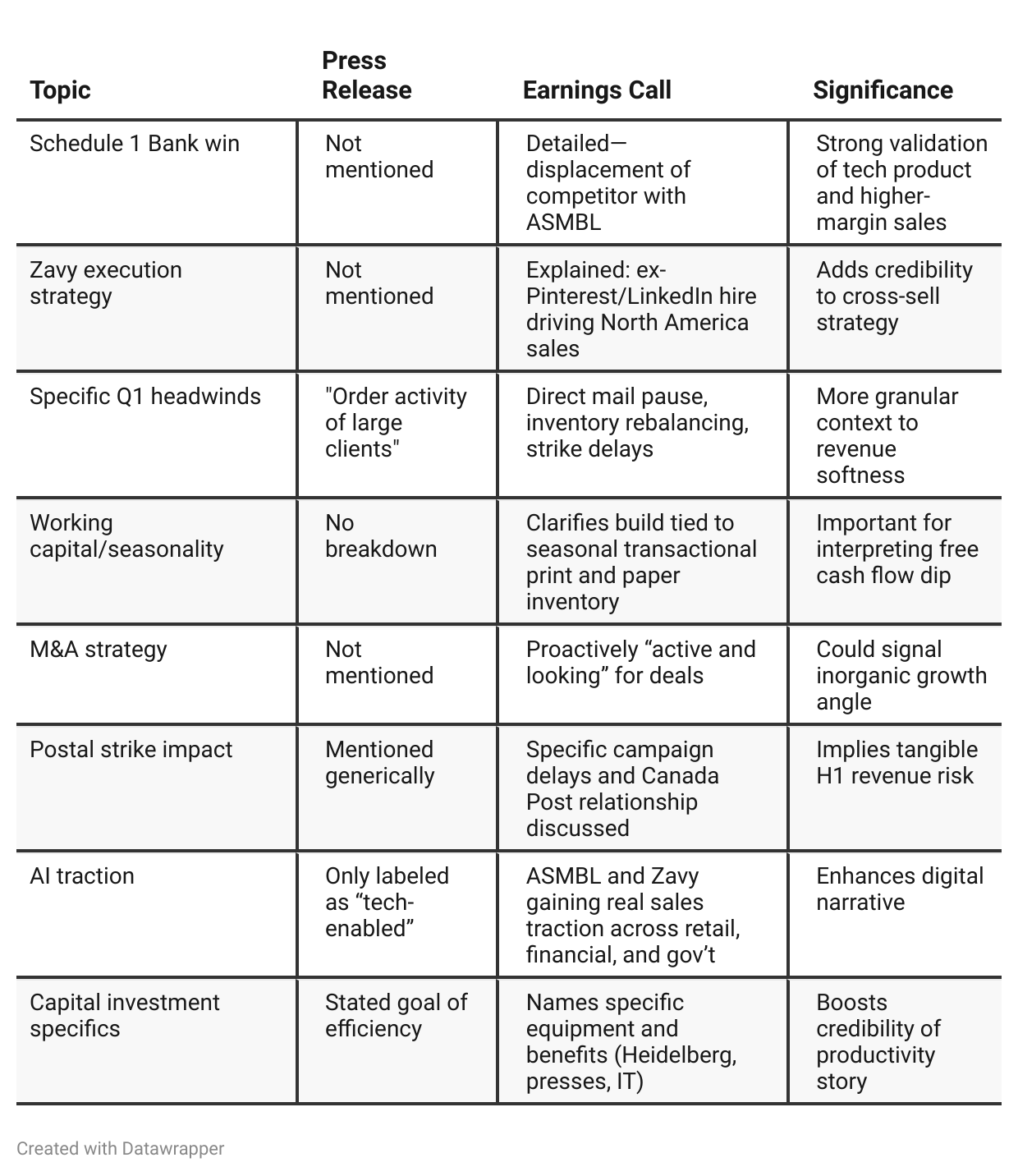

Press Release vs Call Transcript Comparison

While the press release delivers a clean, margin-focused story, the earnings call reveals both the fragility of short-term revenue and the underlying execution strength in tech-led solutions. Investors should weigh the risk of H1 softness against the medium-term upside from new business wins, digital scaling, and operational leverage.

Valuation

Trailing EPS (TTM) : $0.20

Forward EPS Estimate : $0.34

Run-Rate EPS (annualized Q) : $0.36

25× TTM EPS : $5.00

15× Forward EPS : $5.10

Debt/Equity : 6.35

Current Ratio : 1.43

Insider Ownership : —

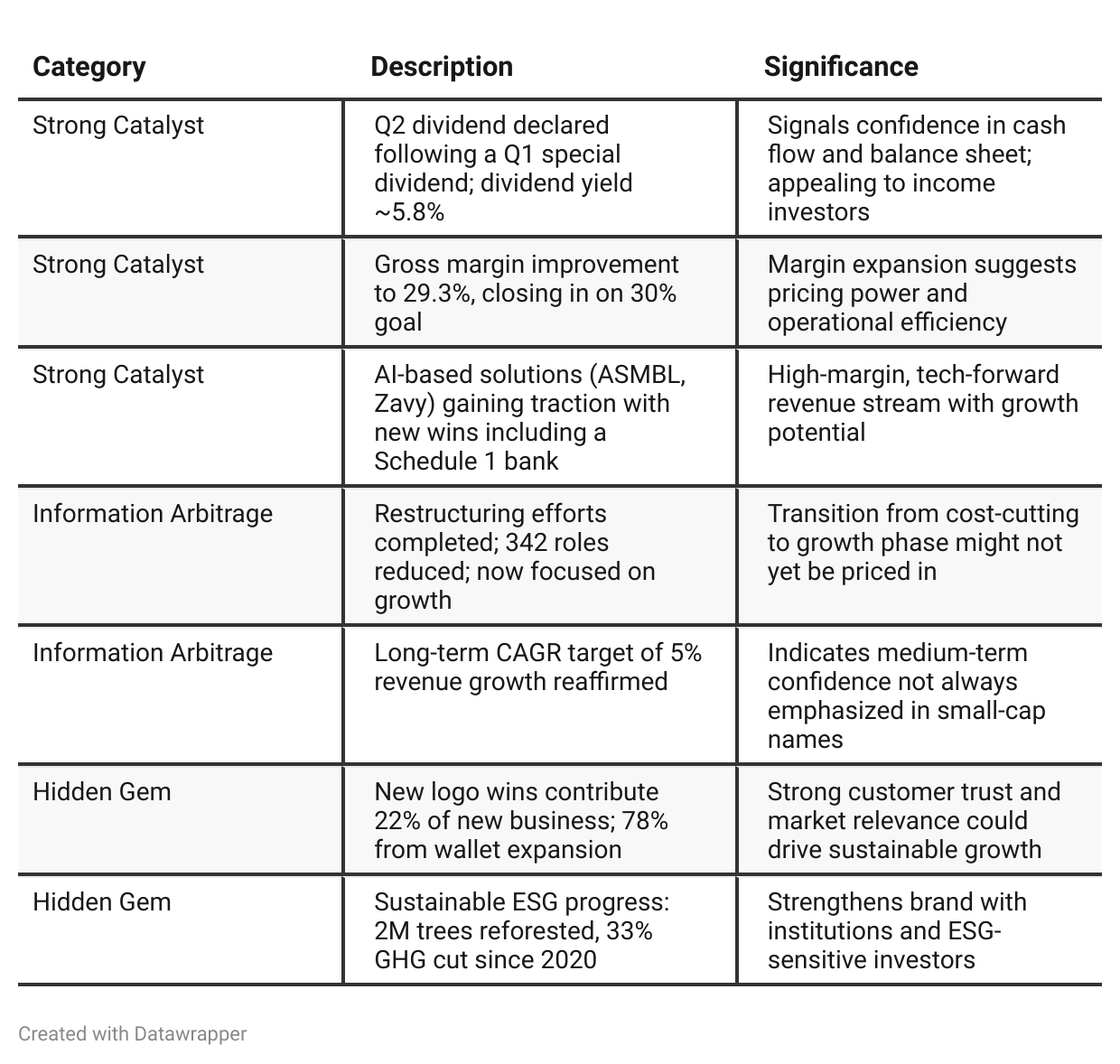

Positive Insights

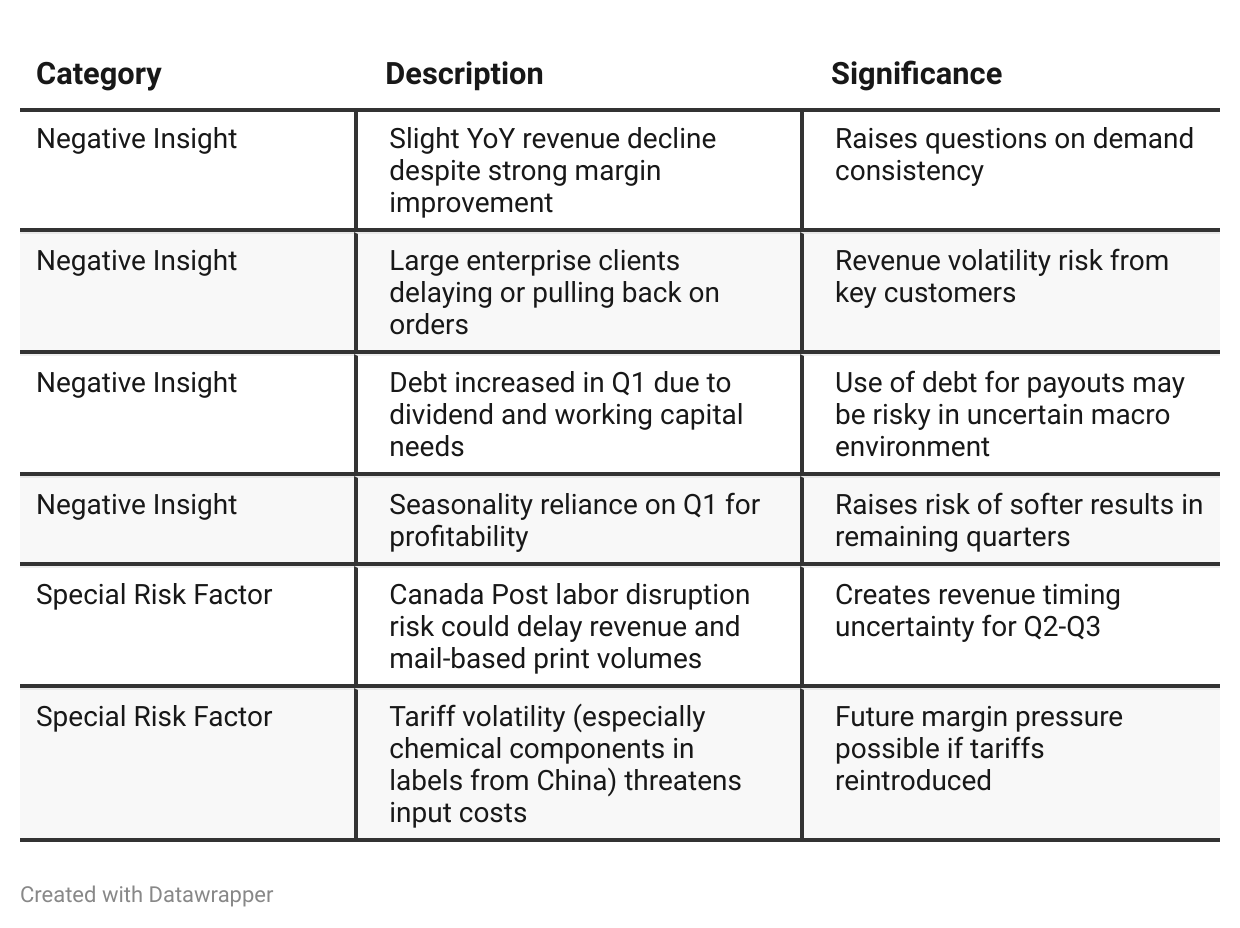

Negative Insights

Tariff Risks

Management flagged tariffs on China-imported chemicals affecting thermal paper and label stock.

Previously spiking to 145%, recently reduced to 30%, temporarily mitigating risk.

DCM sources some components via U.S. intermediaries but still exposed to Chinese origin materials.

Exploring offshore diversification; early traction noted but not fully de-risked.

If tariffs re-rise or U.S.-China tension escalates, margin compression likely unless pass-through is feasible.

Company claims ability to pass cost through, but elasticity of customer response remains untested.

Sentiment Analysis

No tweets expressed sentiment about $DCMDF. The overall sentiment classification is neutral due to lack of investor opinion.

Previous Analysis

Quarter-over-quarter comparison (Q4 2024 Analysis)

DCMDF has transitioned from a company focused on internal consolidation and synergy capture in 2024 to one that is actively pursuing growth through technology, operational leverage, and new business wins in 2025. The Q4 2024 call marked the end of a multi-quarter transformation and integration phase, proudly highlighting restructuring completion, ERP unification, and cost synergies. In contrast, the Q1 2025 call signals the beginning of a new phase—executing on growth, expanding SaaS offerings, and navigating a choppier macro environment with agility. While the company maintains disciplined margin goals and balance sheet prudence, its narrative now centers around capitalizing on new verticals, tech-enabled solutions, and reinvigorated business development efforts.

Year-over-year comparison

—

Final Takeaway

DATA Communications Management is in a growth transition phase, shifting from post-merger restructuring to active new business development. Margin expansion and AI-driven wins are promising, but Q1 revenue softness, debt build from dividends, and external risks like tariffs and postal strikes temper near-term upside. Execution in H2 2025 and macro stability will be critical to re-rating the stock.

Verdict: Hold, with upside if enterprise order flow and digital product growth accelerate as projected.