Crexendo, Inc. (NASDAQ: CXDO) – Q2 2025 Earnings

Crexendo, Inc. (NASDAQ: CXDO) – Q2 2025 Earnings

Earnings Release Date: Aug. 5, 2025

Stock Price: $5.81

Market Cap: $171.0 million

Q2 2025 sales of $16.6 million vs $14.7 million in the prior year

Q2 2025 adjusted EPS of $0.09 vs $0.07 in the prior year

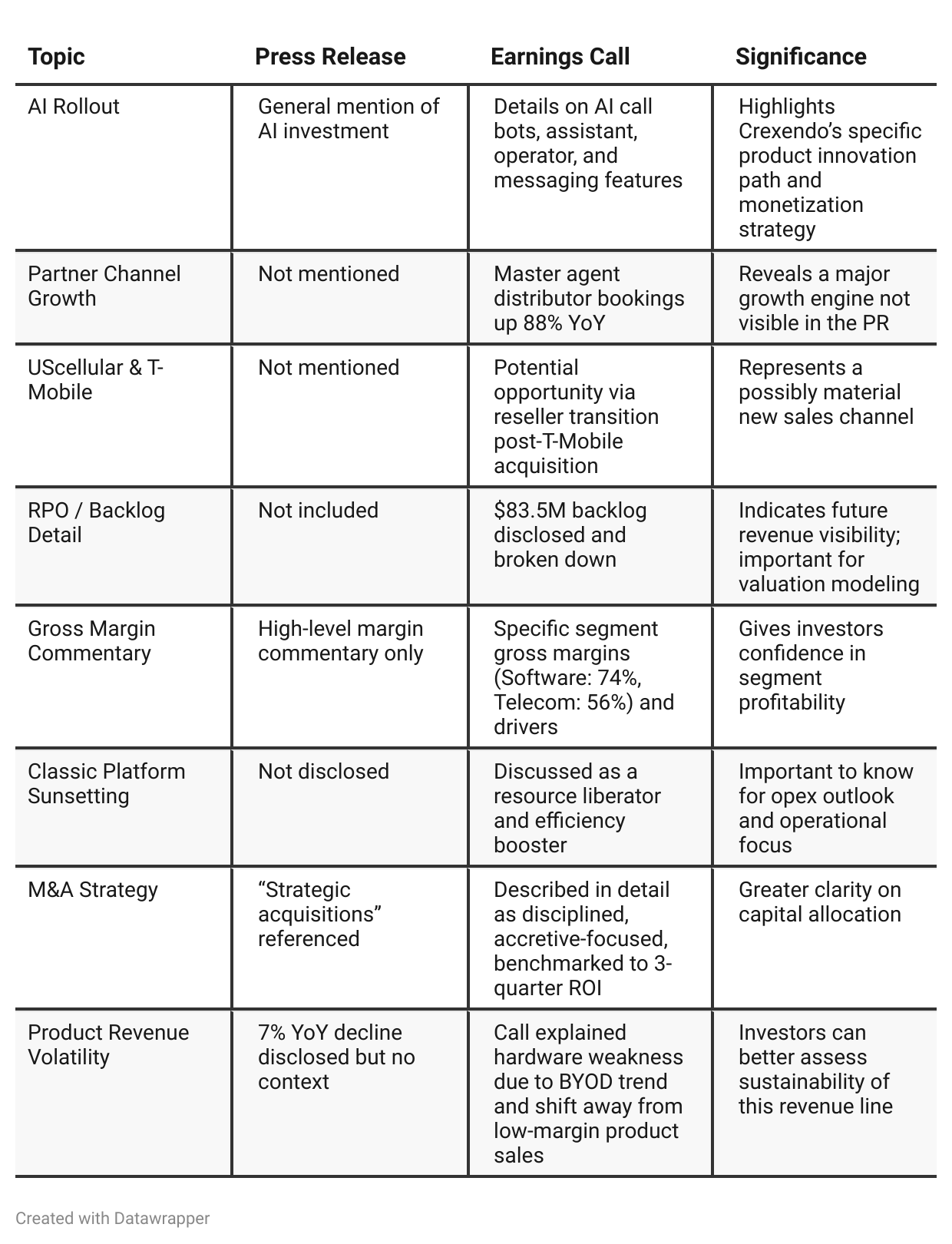

Press Release vs Call Transcript Comparison

The press release paints a strong but high-level picture of Crexendo’s Q2 2025 performance, emphasizing growth and profitability. However, the earnings call adds critical layers of depth that sharpen the investment narrative—especially around margin drivers, AI monetization, reseller channel momentum, and tactical shifts in product mix and infrastructure.

The most material investment insight not found in the press release is the ongoing shift in growth dynamics—from reactive hardware sales to proactive software, licensee, and AI-led strategies—underscored by improving unit economics and disciplined capital deployment. These differences give long-term investors a clearer lens into how Crexendo plans to scale profitably.

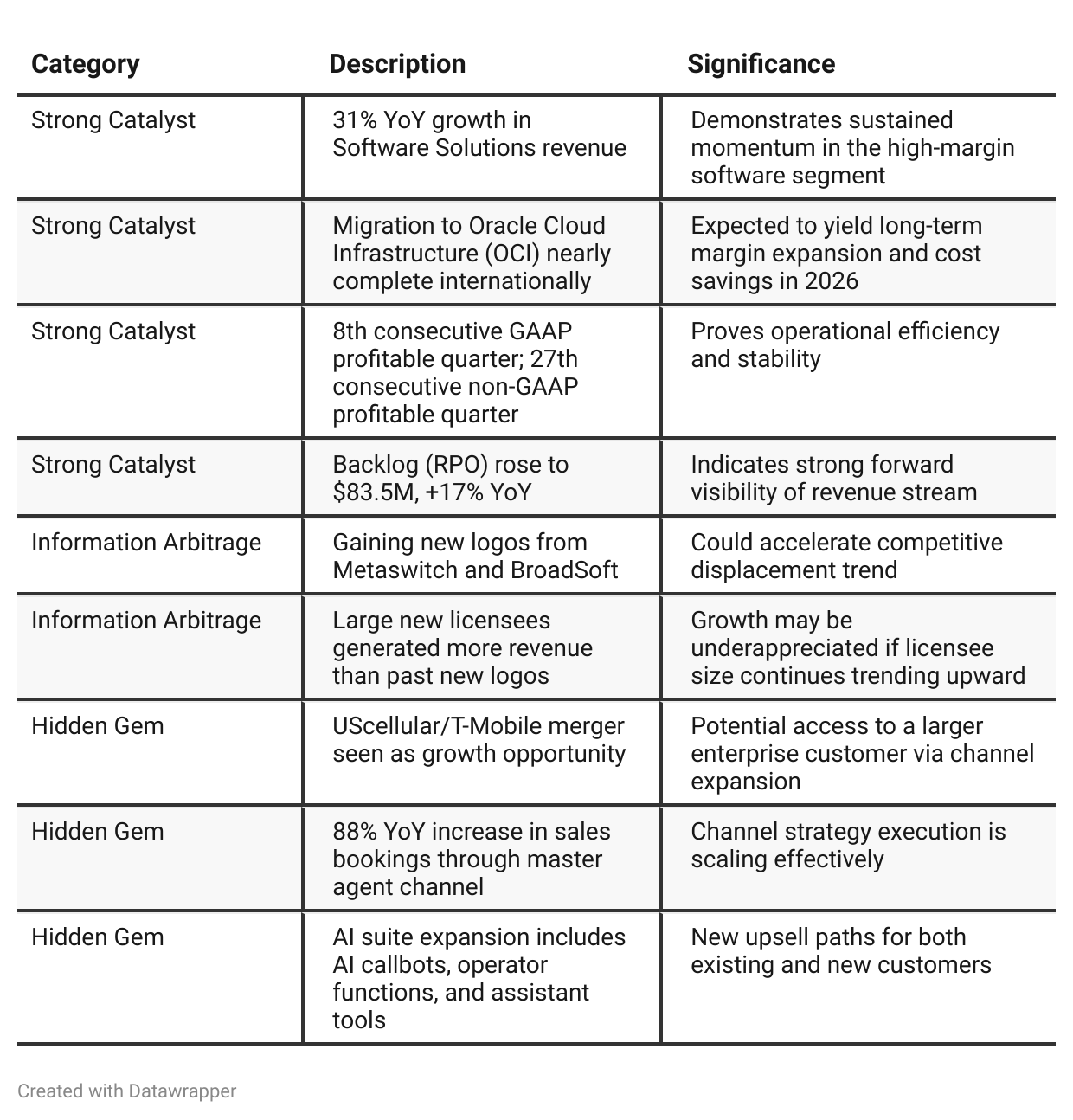

Positive Insights

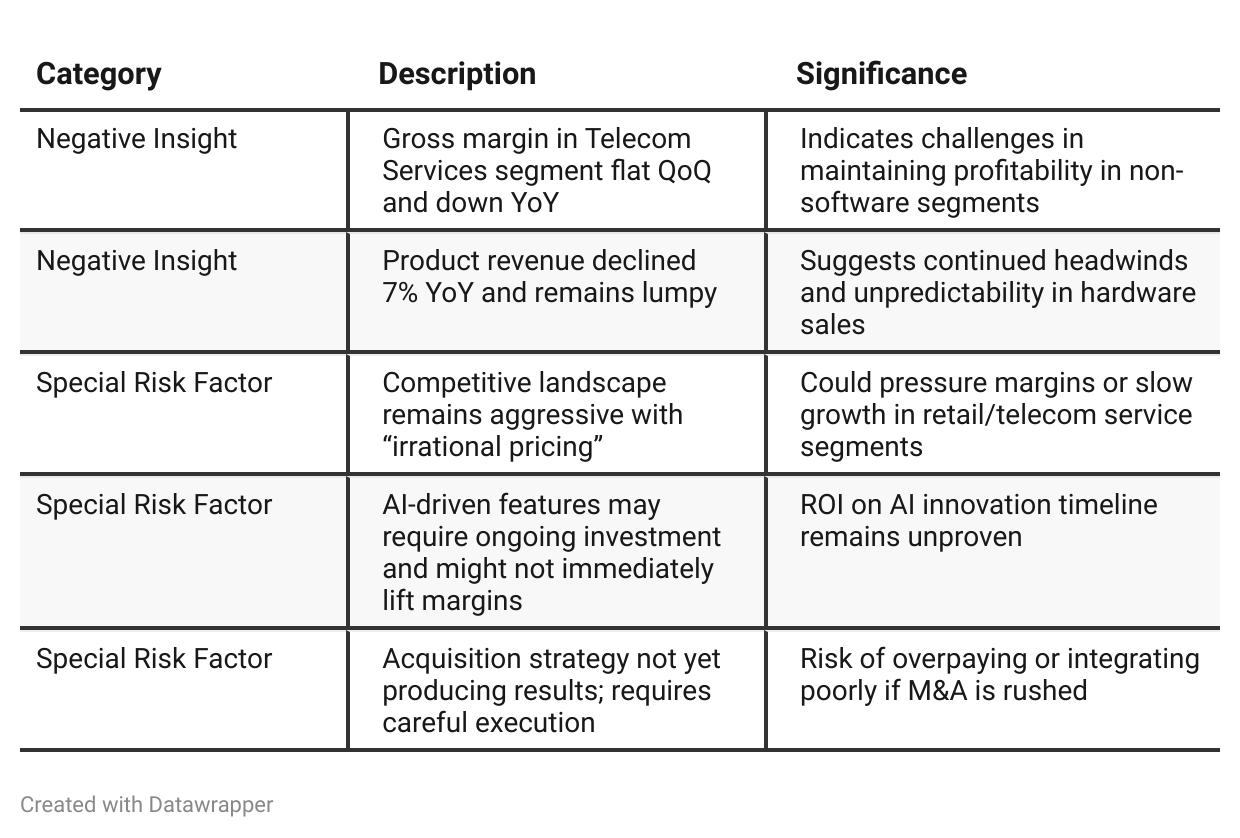

Negative Insights

Tariff Risk

There were no mentions of U.S. tariffs, trade policy, or supply chain issues related to import/export regulation. Hardware sales are down, but declines are driven by strategic deprioritization of low-margin products—not geopolitical trade constraints. No mitigation strategies, reshoring, or tariff exposures were referenced. Tariff risk is currently immaterial.

Previous Earnings Call

Quarter-over-quarter comparison

From Q1 to Q2 2025, Crexendo has maintained a consistent theme of disciplined growth through innovation, but its narrative is becoming more execution-focused.

In Q1, the company leaned heavily on platform differentiation, margin expansion, and internal transformation (e.g., cloud migration, restructuring classic platforms). By Q2, the tone shifted to highlight successful execution of those plans—e.g., OCI international migration completed, strong software margins maintained, and licensee wins converting from Cisco and Metaswitch.The AI messaging also matured from general enthusiasm (Q1) to concrete roadmap items (Q2), while M&A commentary moved from cautious interest to active evaluation of tuck-ins and larger deals. Overall, the company is portraying itself as a maturing, high-margin software infrastructure player, increasingly benefitting from channel momentum and competitor disorder.

Year-over-year comparison

Crexendo’s narrative has evolved from a high-performing VoIP provider executing on GAAP profitability and internal optimization, to a focused, scalable SaaS platform executing a transformation rooted in AI, cloud infrastructure, and licensee growth.

In Q2 2024, the company emphasized GAAP profitability, internal operational efficiency, and margin discipline. By Q2 2025, it leaned more heavily into its identity as a high-growth software company, with AI-powered enhancements, open architecture/API expansion, and strategic OCI migration taking center stage.

The tone has shifted from reactive (operational improvement) to proactive (building the future of telecom). There is also greater transparency on long-term backlog monetization and revenue mix visibility, positioning the company as not just a solid executor, but a strategic consolidator in a disrupted industry.

Final Takeaway

Crexendo is in a growth phase, focusing on software scalability, AI integration, and cloud infrastructure efficiencies.

While the software business is rapidly expanding and highly profitable, the telecom segment remains competitive and volatile. Execution on U.S. data center migration, AI monetization, and disciplined acquisitions will be critical.

Verdict: Buy, with meaningful upside if AI adoption and licensee expansion materialize as expected.