ClearPoint Neuro, Inc. (NASDAQ: CLPT) – Q2 2025 Earnings

ClearPoint Neuro, Inc. (NASDAQ: CLPT) – Q2 2025 Earnings

Earnings Release Date: Aug. 12, 2025

Stock Price: $10.60

Market Cap: $299.5 million

Q2 2025 sales of $9.2 million vs $7.9 million in the prior year

Q2 2025 EPS of ($0.21) vs ($0.16) in the prior year

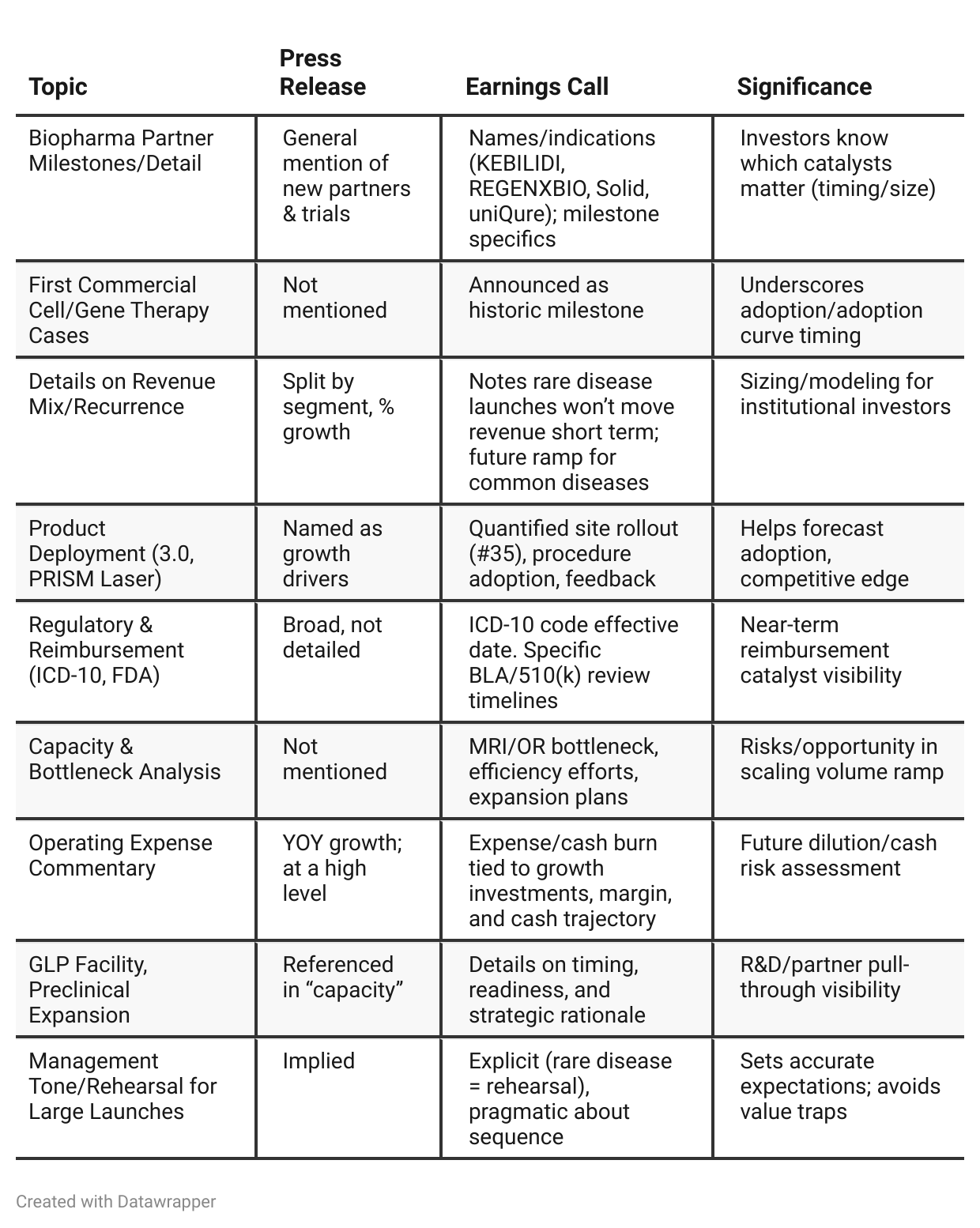

Press Release vs Call Transcript Comparison

Press Release is advantageous for retail or quick-glance investors: it promotes the “record revenue” and “Fast. Forward.” narrative, but skips granular risk and milestone context.

Earnings Call is far more useful for institutional and sophisticated investors: it clarifies that while growth is real, most near-term impact is either symbolic or preparatory for much larger, uncertain future commercial waves.

The call’s granularity (especially around operational efficiency, bottlenecks, and pipeline prioritization) lets investors model the ramp and potential disappointment if major indications are delayed, not approved, or partners choose to go in-house.

The large capital raise covers cash needs for now, but highlights risk of ongoing losses and future dilution should ramp timelines slip.

Major upcoming binary events (FDA decisions, partner commercialization, reimbursement code activation) are more visible post-call.

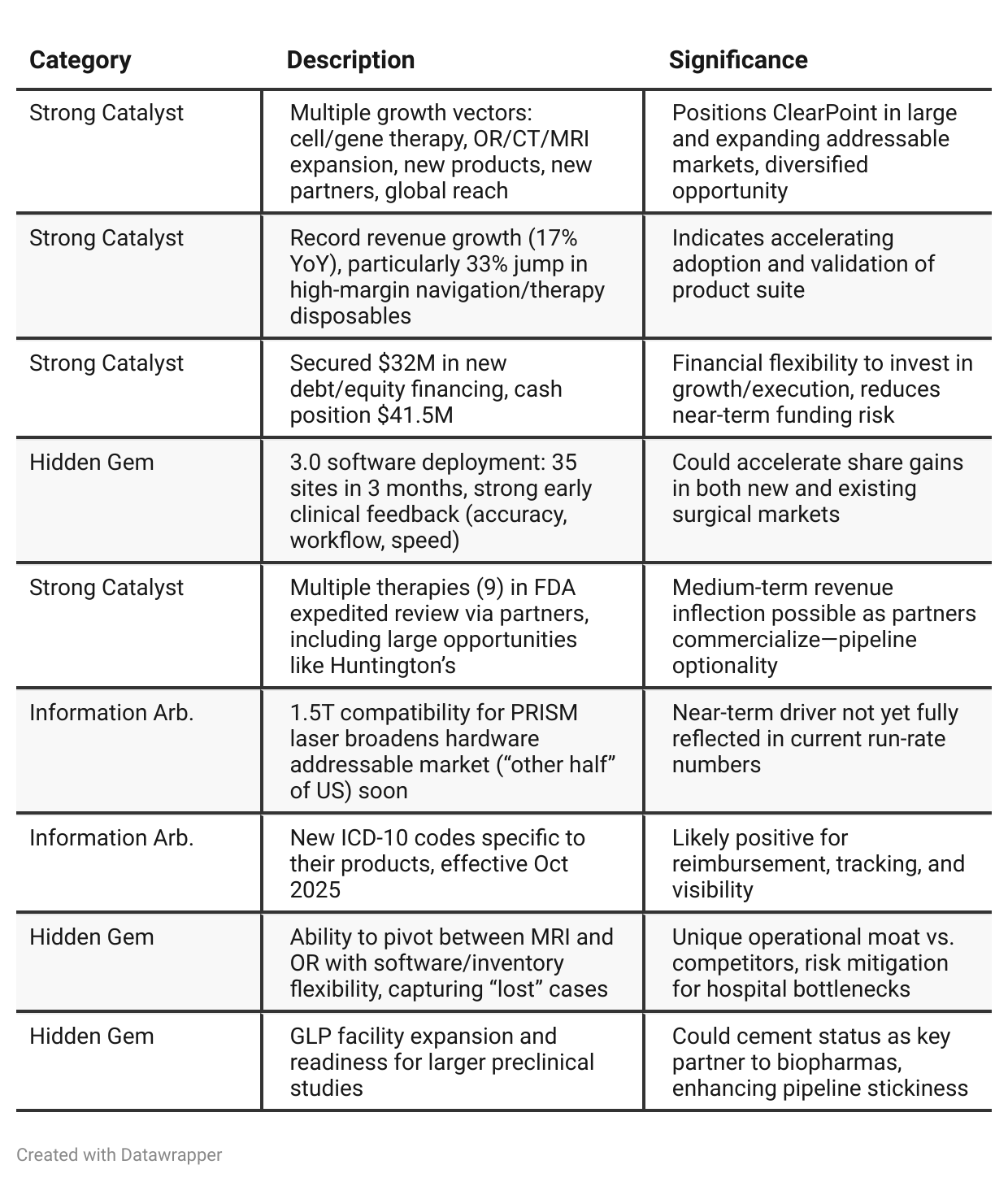

Positive Insights

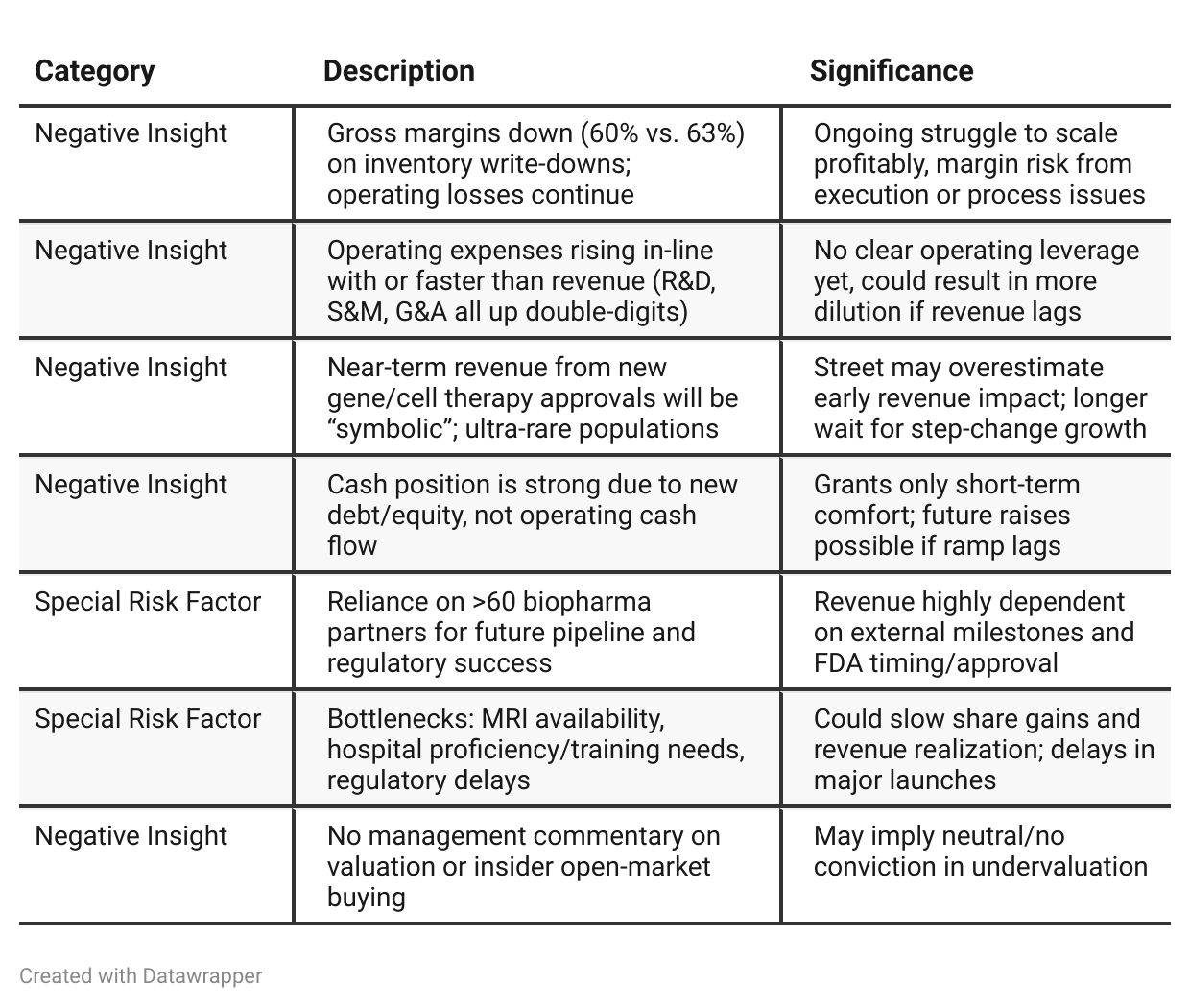

Negative Insights

Tariff Risk

Mentions: No direct mention of tariffs, trade policies, or geopolitical risk on this call.

Implication: No commentary on revenue, supply chain, or cost structure impacts from U.S./global tariffs. No mitigation/hedging strategies discussed.

Conclusion: Investors should independently monitor for any impacts from U.S. trade/tariff policy, especially as ClearPoint expands internationally. If manufacturing is global or if components are sourced from tariff-impacted regions, risk could potentially rise—but management did not address it on this call.

Sentiment Analysis

The overall sentiment toward $CLPT is neutral to cautiously bullish. Many investors express ongoing interest and incremental buying on weakness, reflecting underlying optimism about potential upside, especially around new product approvals and expanded market opportunities. However, several posts highlight skepticism or frustration about near-term commercialization, lackluster price action, and operational challenges. While some individuals are bullish about technical signals and growth milestones, others express hesitation, boredom, or prefer alternative investments in the near term. The tone indicates patient optimism but with tempered expectations and some uncertainty about immediate returns.

Previous Earnings Call

Quarter-over-quarter comparison

Q1 2025: ClearPoint Neuro began the year by unveiling the ‘Fast Forward’ phase, with a strong focus on building operational capacity, securing strategic funding, and laying the groundwork (hiring, infrastructure, regulatory investments) for expected partner-driven revenue inflection. The messaging was one of patience, readiness, and conviction—OpEx growth was justified by the need to “prepay” for market readiness, and Q1 was explained as foundational rather than a period for near-term payback. Management spent significant time clarifying that sequential revenue growth might be uneven due to accounting changes (Pathfinder program) but that the real story was one of under-the-hood momentum.Q2 2025: In Q2, the tone shifts subtly toward results and early execution. The company starts to see tangible evidence of its strategy with “record revenue,” increased product adoption, and first-ever commercial CGT cases. Management’s messaging is one of “validation”: not just building, but now demonstrating progress across several fronts (clinical, market access, regulatory). While the CEO remains realistic about near-term revenue from new platforms being “symbolic,” there is more detail and substance behind growth vectors, and measurable proof points of adoption. The core narrative evolves from “preparing for the future” to “showing it’s starting to work,” albeit still early and with full profitability/profit inflection pushed out to future periods.

Year-over-year comparison

From Q2 2024 to Q2 2025, ClearPoint Neuro’s narrative noticeably matures. In 2024, management painted a vision of transformation, focusing on upgrading internal structures and product breadth, signing a diversity of long-lived pharma contracts, and building a global base—an “engine” ready for sustainable growth. By 2025, the tone is more operational and reflective, spotlighting the shift from foundational preparation to early realization: commercial cases are being completed, multiple partners’ therapies are nearing or passing regulatory milestones, customer installs are shifting from anecdotal to quantifiable scale, and the company is emphasizing speed, capacity, and readiness for much larger future demand.

The strategy is the same, but Q2 2025 is about execution against it—converting projections and plans into tangible events, managing through logistics and bottlenecks, and focusing on both resilience and readiness for mass-market gene therapy delivery. Risk management is also more transparent, with management acknowledging that initial commercial impacts from new launches will be moderate, and the “big ramp” is still ahead but now more believable given early success metrics.

Final Takeaway

ClearPoint Neuro is in a growth and platform expansion phase, focused on leveraging its technology suite across cell/gene therapy delivery, operating room navigation, and global market access. While recent results highlight product momentum, rising cash/equivalents, and partner validation, the translation of these milestones into material, sustained revenue and margin leverage remains ahead, and depends on both internal execution and external clinical/regulatory events. Investors should watch for execution on large-market launches, site expansion rate, reimbursement wins, and cost/margin discipline in upcoming quarters. Verdict: Hold, with significant upside if operational and external catalysts break in the company’s favor.