Cellebrite DI Ltd. (NASDAQ: CLBT) – Q2 2025 Earnings

Cellebrite DI Ltd. (NASDAQ: CLBT) – Q2 2025 Earnings

Earnings Release Date: Aug. 14, 2025

Stock Price: $13.99

Market Cap: $3477.5 million

Q2 2025 sales of $113.3 million vs $96.0 million in the prior year

Q2 2025 EPS of $0.08 vs $0.12 in the prior year

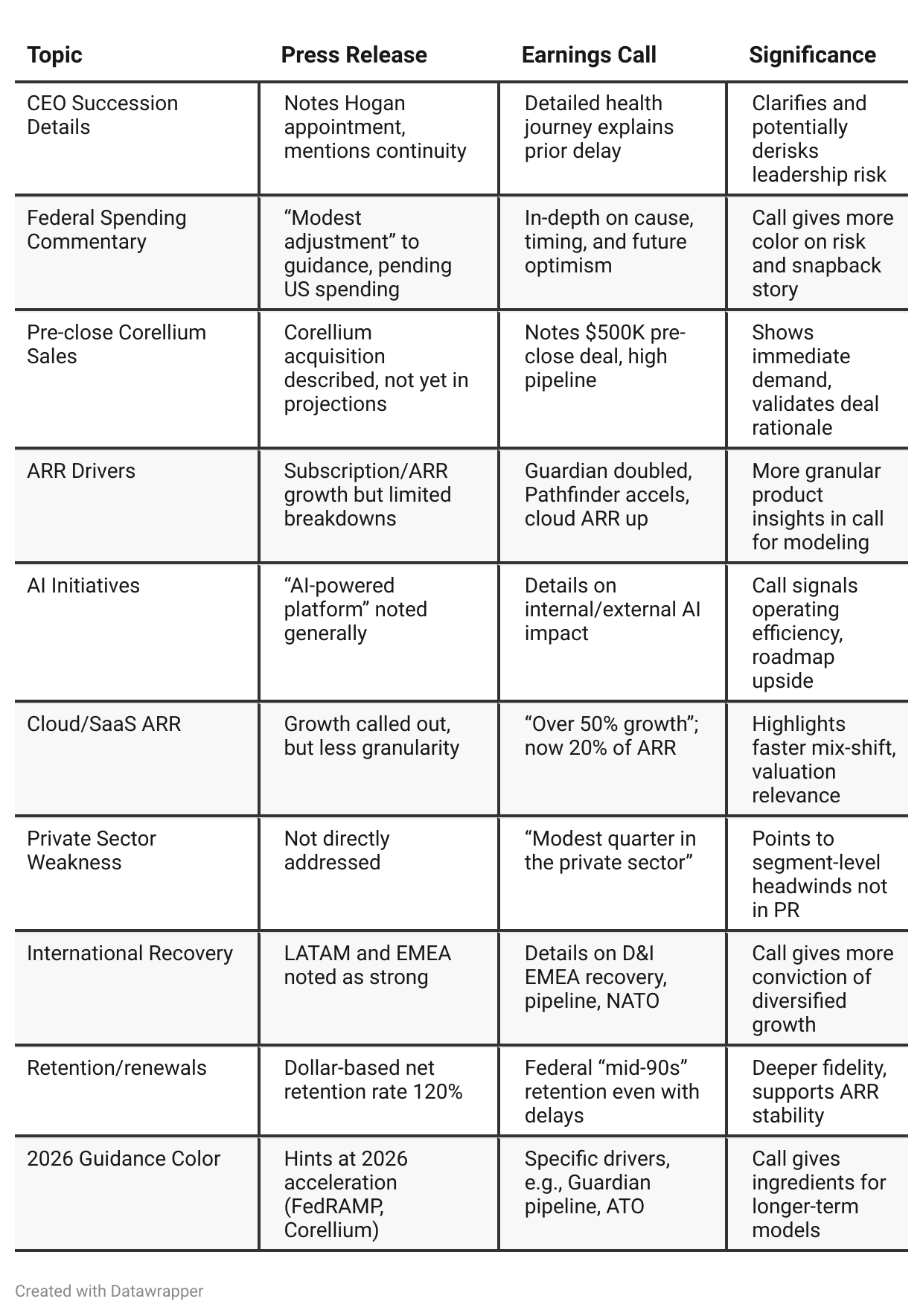

Press Release vs Call Transcript Comparison

Management Transition: Call provides assurance on seamless CFO handoff, consistent “bottoms-up” financial process.

M&A/Margin Philosophy: CFO and CEO reiterate desire for “thoughtful” capital allocation, suggesting disciplined M&A, reinvestment, and headcount management.

AI Not Just Hype: Emphasize not just “putting an LLM in front” but integrating into products and workflows—reduces risk of fad-based spending, offers true competitive advantage.

Q&A Validates Narrative: Analysts probe federal risks, product adoption, AI, and management transitions; management responses reflect transparency and credible, not just marketing-anchored, answers.

Strategic Vision: Several allusions (especially call) to near-term (cloud/FedRAMP, Corellium) and long-term (AI, new R&D, partnerships, additional M&A) levers for growth.

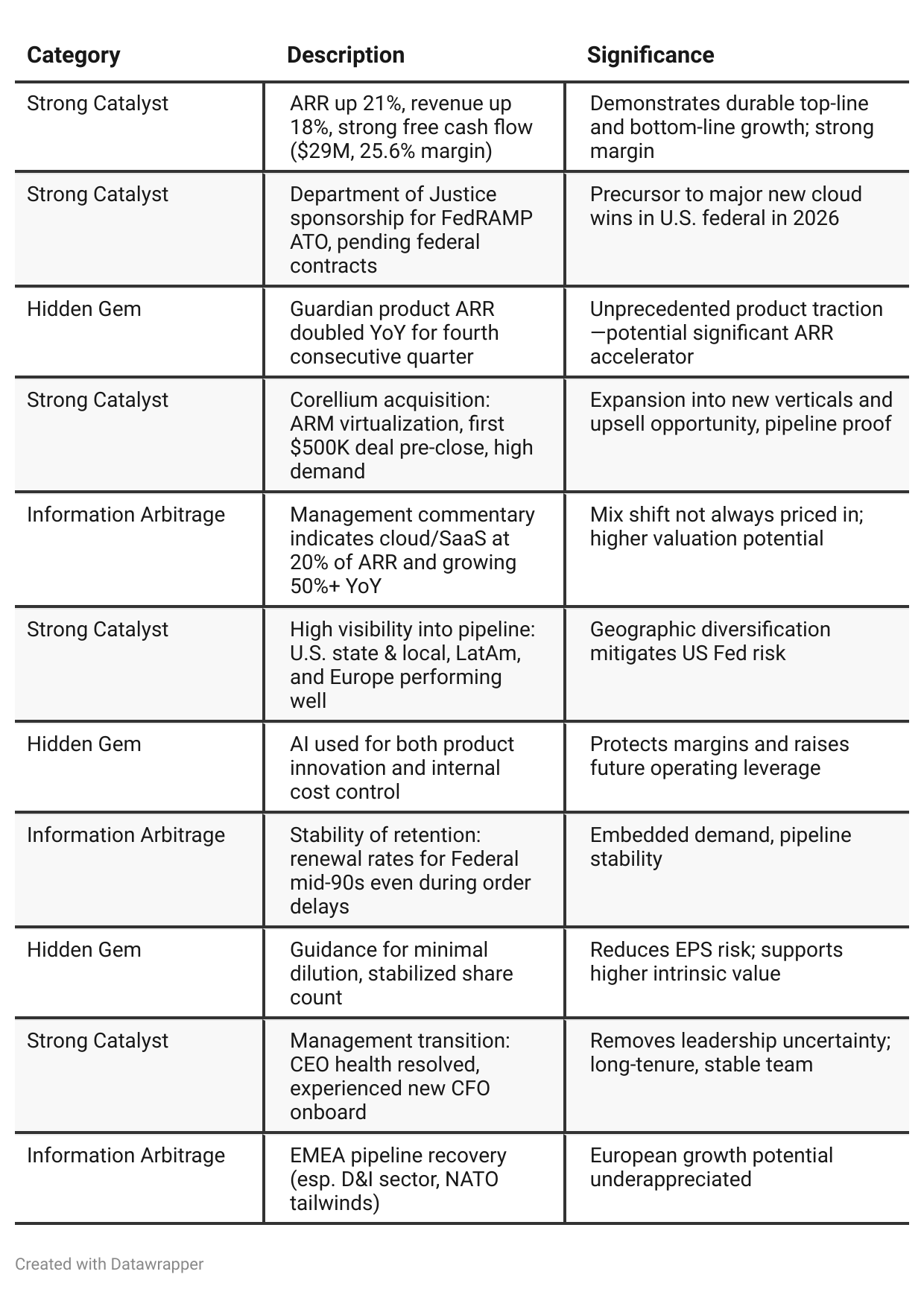

Positive Insights

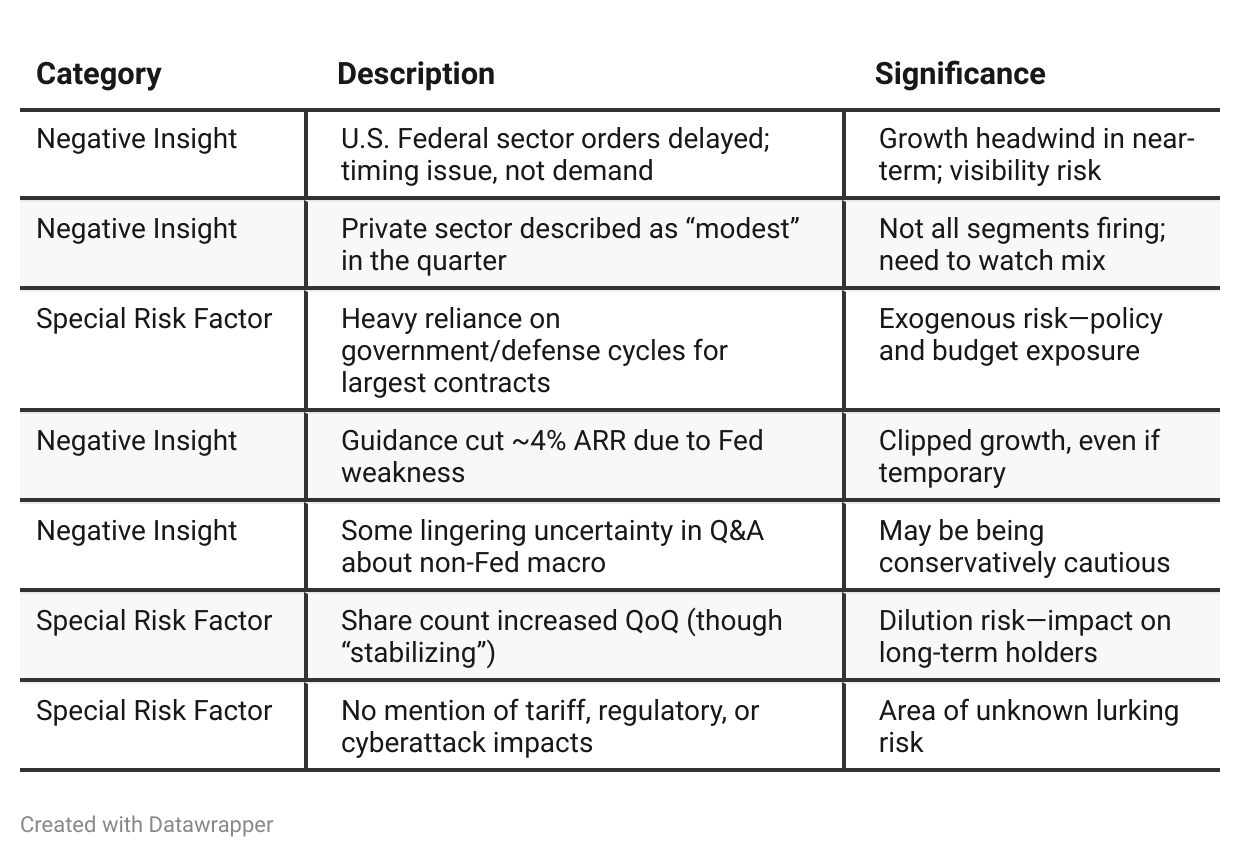

Negative Insights

Tariff Risk

No mention of tariffs, trade policy, or supply chain impacts was made during the Q2 2025 Cellebrite earnings call. Management did not discuss any risks or mitigation actions related to tariffs, nor did analysts raise these issues.

Current Impact: None identified on revenue or margins.

Mitigation Actions: No supply chain or pricing changes noted.

Forward-Looking Risk: Not addressed in this call; monitor future filings or updates for changes.

Bottom line: Tariffs are not currently a risk factor for Cellebrite based on this transcript, but investors should stay alert for future developments in regulatory filings or subsequent calls.

Previous Earnings Call

Quarter-over-quarter comparison

Q1 2025: Cellebrite’s management struck a pragmatic, steady tone—direct about US federal order delays, optimistic on pipeline, and keen to illustrate global and product diversification, but still in interim leadership mode. Macro risk (“timing not demand”) was the key theme, and operational discipline was stressed as the means to both offset volatility and maintain growth aspirations. Product innovation and International/Defense pivots were underway, but the narrative was “wait and see”.Q2 2025: The company’s narrative grows more energized, poised, and confident. Leadership uncertainty is resolved with a poignant CEO story. The tone is “ready for resurgence”: product and federal cloud milestones accelerate growth visibility into 2026 and beyond. Corellium acquisition and FedRAMP sponsorship are cornerstones of the future vision. Margins and FCF are highlighted as proof points for disciplined execution. Management acknowledges risks but frames them as transitory within a strengthening growth story, making the Q2 call feel less defensive and more forward-driving than Q1.

Year-over-year comparison

Q2 2024 illustrates a company at the “scaling and unlocking” phase—leveraging acquisitions for the federal market, investing in sales and R&D, and raising guidance on the back of strong platform and cloud expansion. Focused, optimistic, and a bit celebratory, with clear goals for platform migration, cross-sell, and cloud transition.

Q2 2025 demonstrates a transition to resilience and long-term positioning. The company is more experienced, leading through turbulence (federal timing, CEO health), transparent, and focused on executional discipline and upcoming catalysts (FedRAMP, Corellium, further AI). The story is less about short-term beats and more about reliability, high retention, operational strength, and inevitability of outcome given macro and policy drivers.

Final Takeaway

Cellebrite is in a clear growth phase, leveraging innovation in digital investigation, cloud/SaaS expansion, and strategic M&A (Corellium) to drive robust ARR and profitability gains. While delayed U.S. federal contracts present a temporary headwind, strong retention, pipeline visibility, and upcoming catalysts (FedRAMP ATO, budget release) support a positive outlook. Margin discipline and operational efficiency via AI further strengthen the investment case. Execution on Corellium integration and securing federal wins will be critical. Verdict: Buy, with significant upside as federal tailwinds resume and product initiatives scale.