BluMetric Environmental Inc. (OTCQX: BLMWF/BLM.V) – Q2 2025 Earnings

BluMetric Environmental Inc. (OTCQX: BLMWF/BLM.V) – Q2 2025 Earnings

Earnings Release Date: May 28, 2025

Stock Price: $1.63

Market Cap: $53.8 million

Q2 2025 sales of $15.9 million vs $7.1 million in the prior year

Q2 2025 EPS of $0.00 vs $0.00 in the prior year

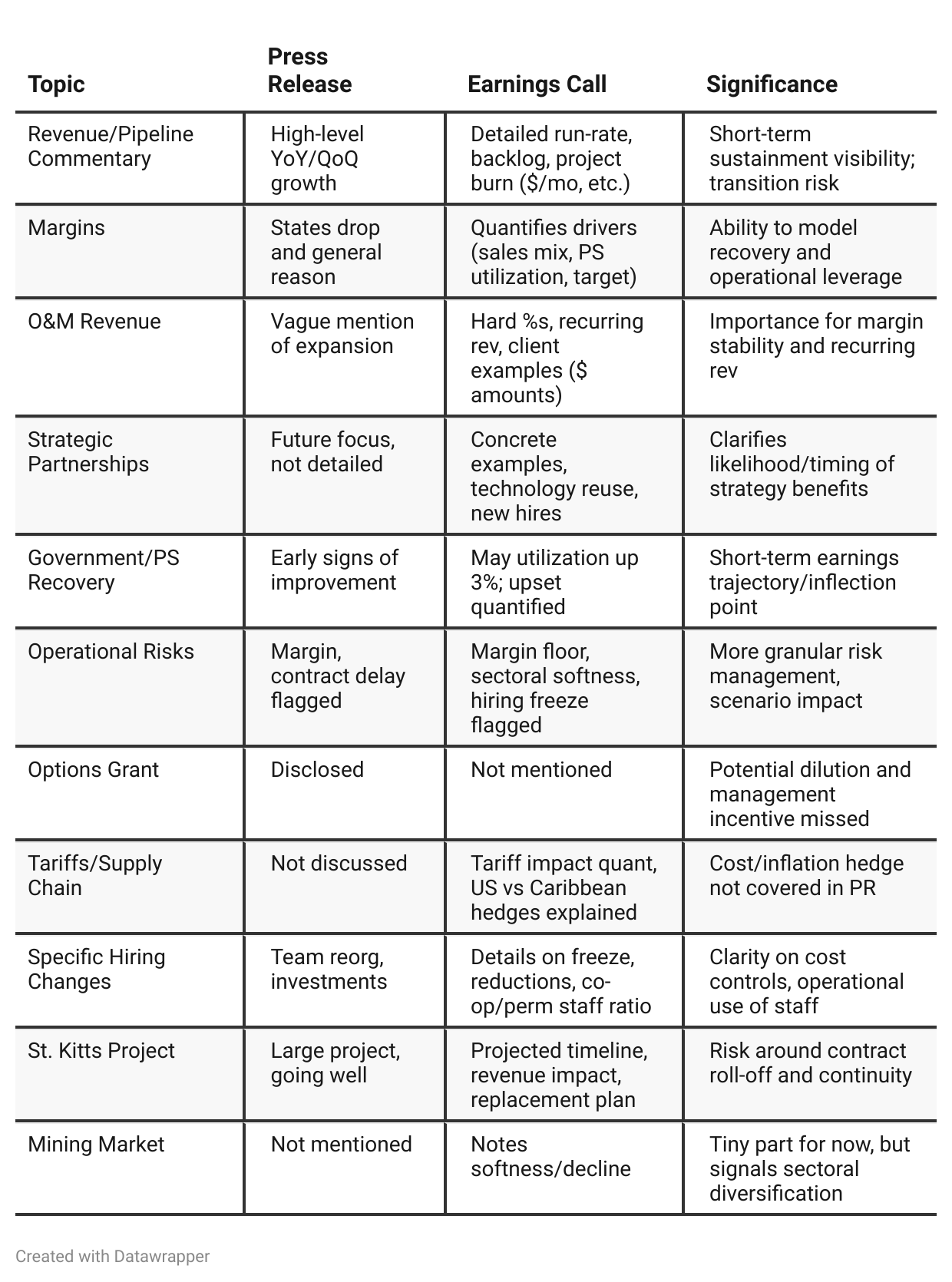

Press Release vs Call Transcript Comparison

Investor Sentiment: The call provides far greater transparency and accessible performance targets (e.g., 10% EBITDA at $100M revenue), which the press release omits.

Execution Focus: Management repeatedly emphasizes “execution” and “one foot on the brake, one on the gas,” conveying prudent capital management during rapid growth and cyclical setbacks.

Staff Strategy: Detailed rationale for retaining key personnel despite utilization dips signals a focus on long-term capability over short-term cost.

Recurring Revenue: Earnestly promoted in the call; next step in Company’s business evolution toward higher-value, steadier margins (O&M, US municipal market).

Underlying Caution: Management avoids overpromising—states what is and isn’t in the backlog, and expresses non-specific optimism about partnership opportunities rather than announcing them prematurely.

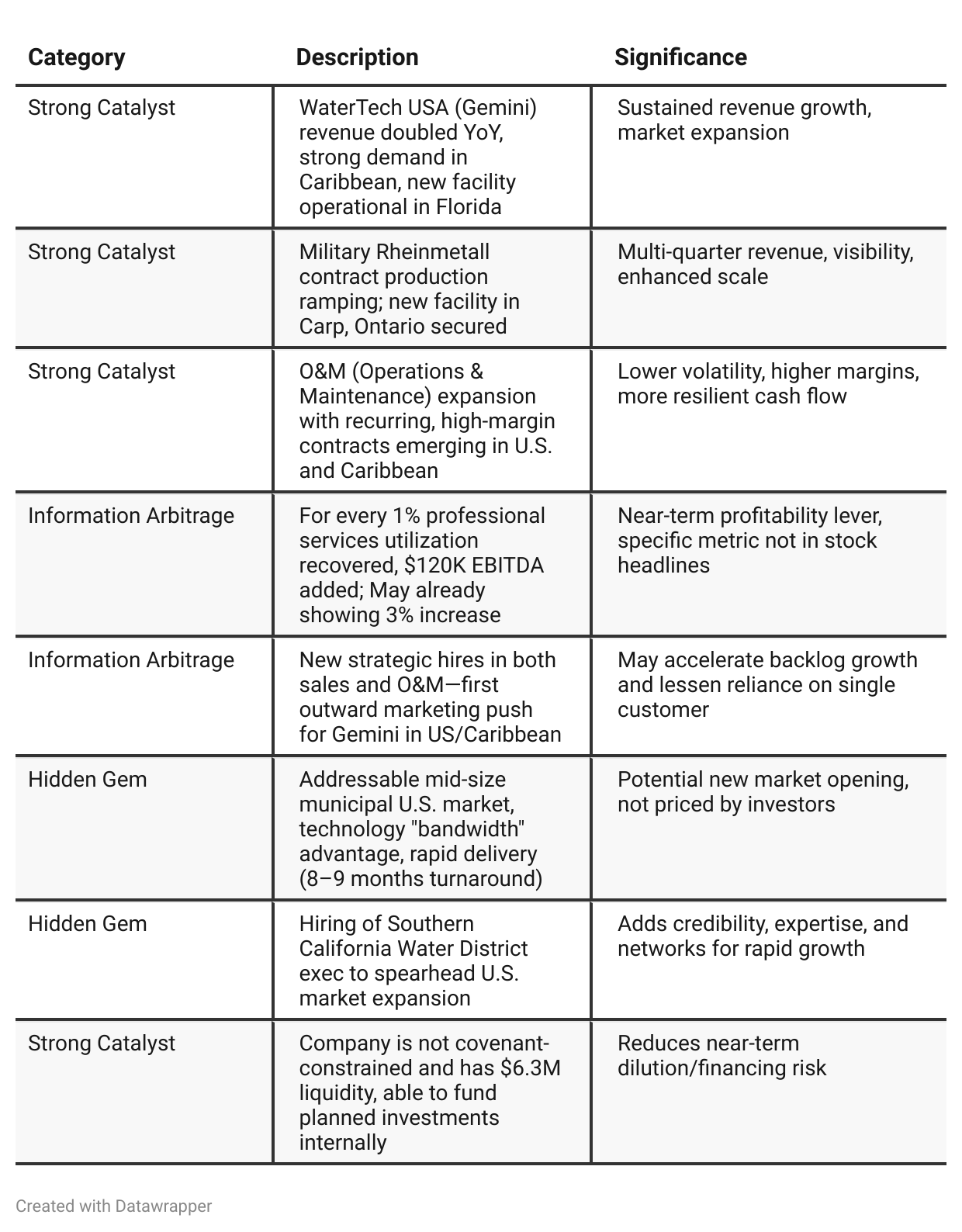

Positive Insights

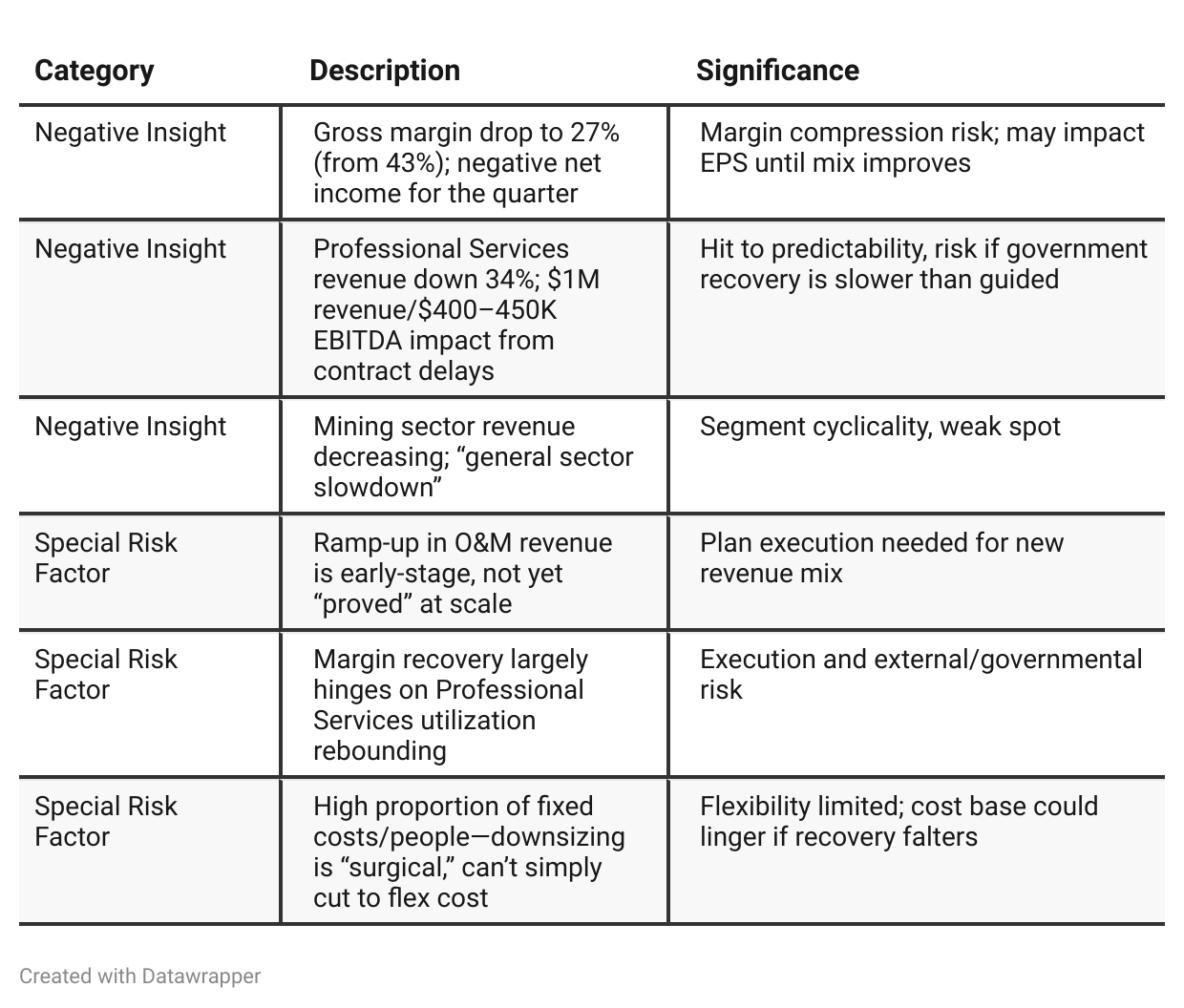

Negative Insights

Tariff Risk

Mentions & Impact

In Q1, preemptively purchased materials to “stay ahead of tariffs”—but did not need to do so in Q2.

Tariff risk on U.S. sales (~13% cost impact) is being passed to customers; Caribbean sales “hedged” by exporting directly from Canada, thus bypassing U.S. procurement/tariff requirements.

Management does not expect material earnings impact from tariffs presently, as clients are absorbing costs.

Mitigation Actions

Strategic supply chain routing (Canada for Caribbean) to avoid tariffs.

Customers in the U.S. are, so far, absorbing higher costs.

No indication that tariffs are significantly affecting competitive position or innovation at present.

Management has set a “baseline” for supply chain operations, not buying in advance now.

Forward-Looking Commentary

No expectation of material profitability impacts from current tariff regime.

Competitive advantage may exist for Caribbean market (due to logistics flexibility), but is minor in broader context.

No warning for 2H’25; continues to monitor for new developments.

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Between Q1 and Q2 2025, BluMetric’s narrative developed from a stance of “cautious operational optimism” to one of “confidence in scalable execution and recovery.” In Q1, management’s focus was on de-risking—accelerating shipments, buffering against political/macroeconomic shocks, and strengthening the company’s liquidity through a well-timed equity raise. Growth was emphasized, but always alongside prudence and an acute awareness of macro uncertainties.By Q2, that caution gave way to a firmer conviction in the company’s business model and capacity for sustainable growth. Management highlighted not just revenue growth, but tangible milestones: an operational U.S. facility, the long-awaited military contract moving to production, and the beginnings of a sticky, recurring O&M business. There was more candor regarding the negative impacts from external shocks—especially government spending pauses—and clear communication of the levers available to restore profitability.

Year-over-year comparison

—

Final Takeaway

BluMetric Environmental Inc. is in a growth and business-mix transformation phase. Key growth drivers are WaterTech/Gemini’s U.S./Caribbean outperformance and a ramping multi-year military contract, with the expansion of high-margin recurring O&M business as an emerging upside lever. Critical risks revolve around margin pressure from sales mix, Professional Services underutilization, and execution on new contract types. Execution on O&M ramp and Professional Services recovery will determine re-rating potential. Verdict: Hold, with upside potential as profitability signals materialize.