BluMetric Environmental Inc. (TSXV: BLM) (OTCQX: BLMWF) – Q3 2025 Earnings

BluMetric Environmental Inc. (TSXV: BLM) (OTCQX: BLMWF) – Q3 2025 Earnings

Earnings Release Date: Aug. 27, 2025 (all figures in Canadian dollars)

Stock Price: $1.18

Market Cap: $43.4 million

Q3 2025 sales of $14.7 million vs $8.1 million in the prior year

Q3 2025 loss per share of ($0.01) vs EPS of $0.00 in the prior year

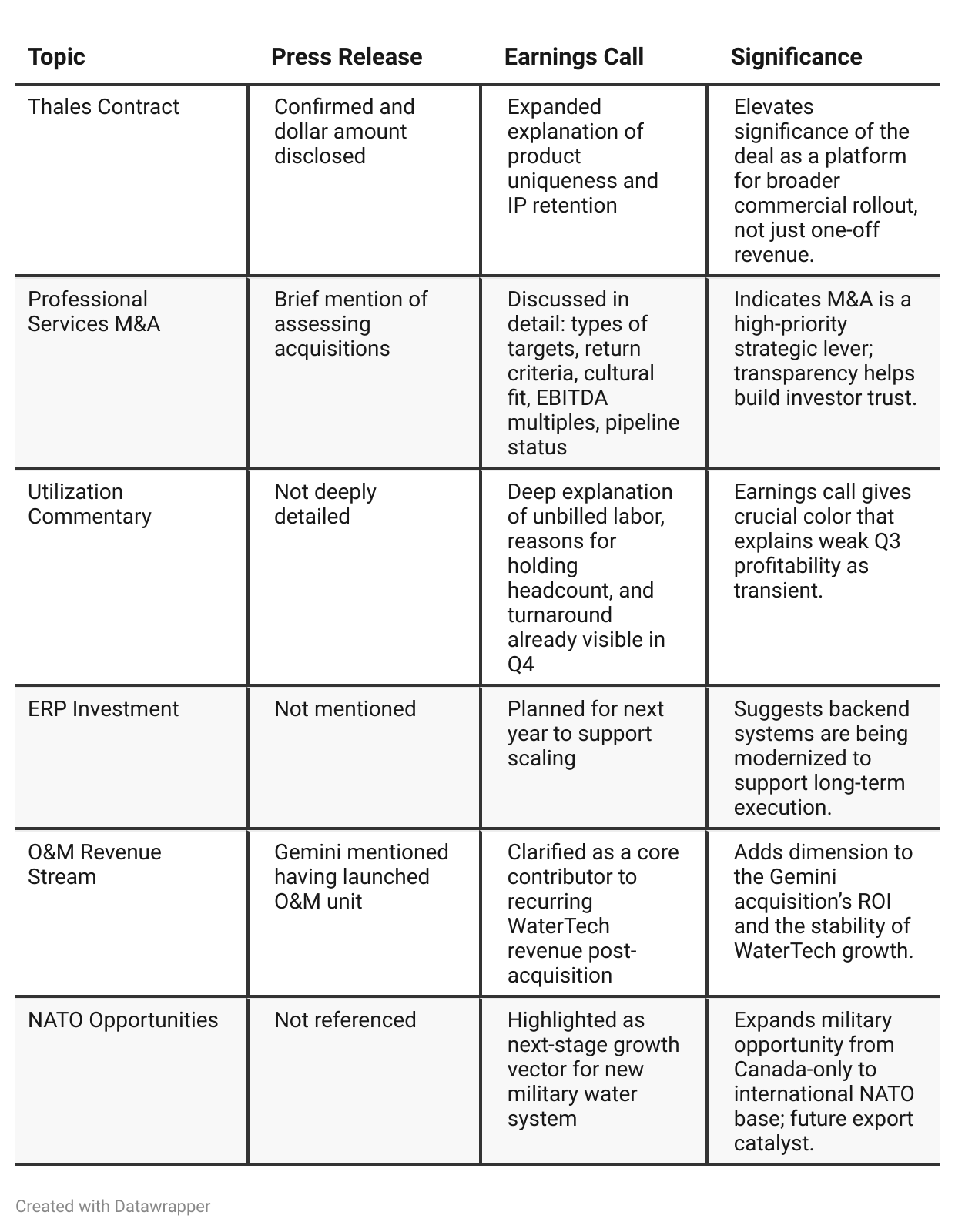

Press Release vs Call Transcript Comparison

The press release highlights strong top-line growth and new contract wins but leaves important context unspoken—particularly regarding the transitory nature of Q3 margin pressures and the strategic rationale behind retained headcount and upcoming operational improvements.

The earnings call fills these gaps, offering detailed insights into cost structures, utilization recovery, and forward-looking initiatives like ERP rollout and NATO/commercial maritime product expansion.

For investors, the call significantly strengthens the bullish case, painting a clearer picture of how BluMetric intends to sustain its growth while improving profitability. The differences between the documents underscore the importance of listening to management’s voice for true color behind the numbers.

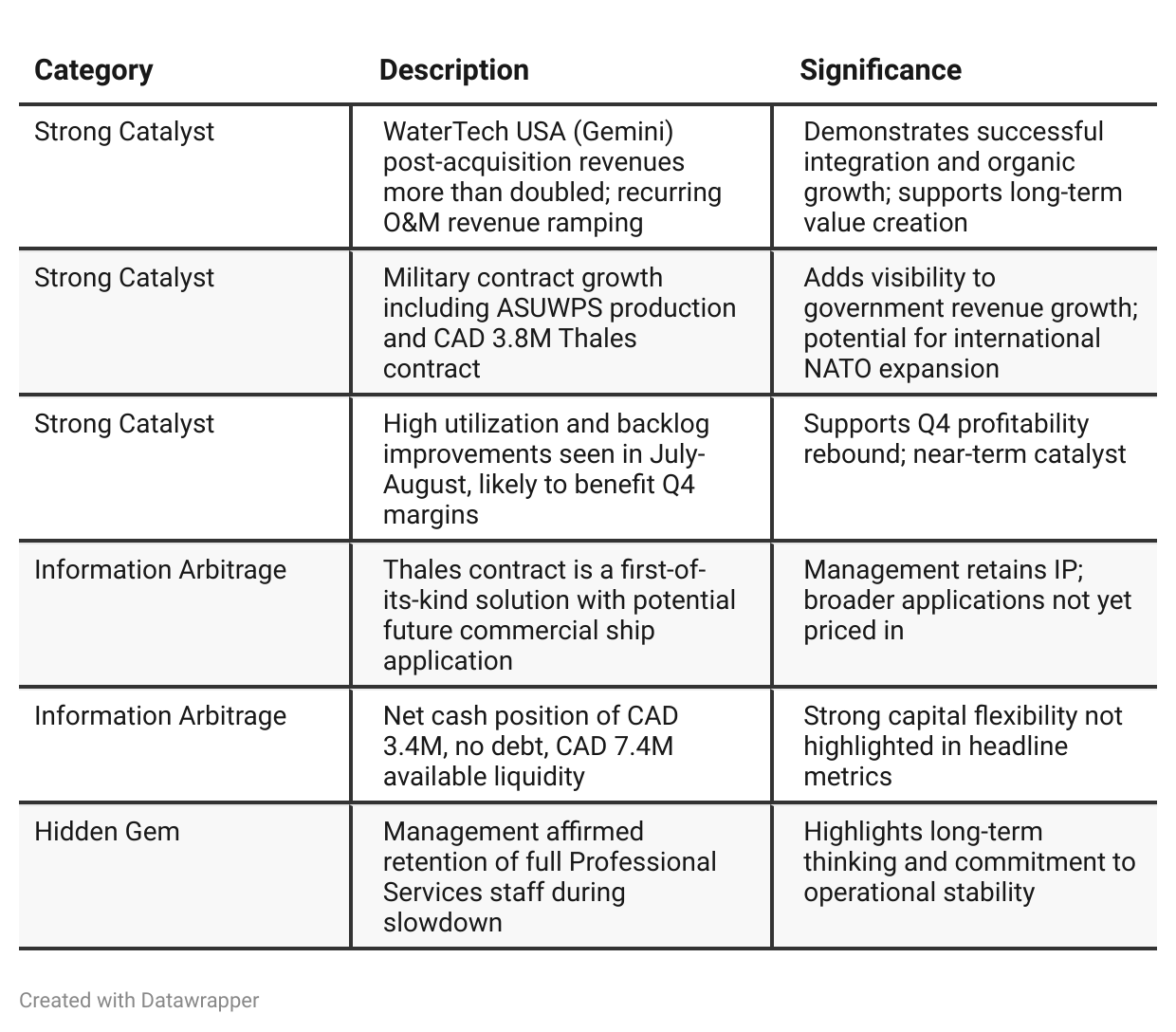

Positive Insights

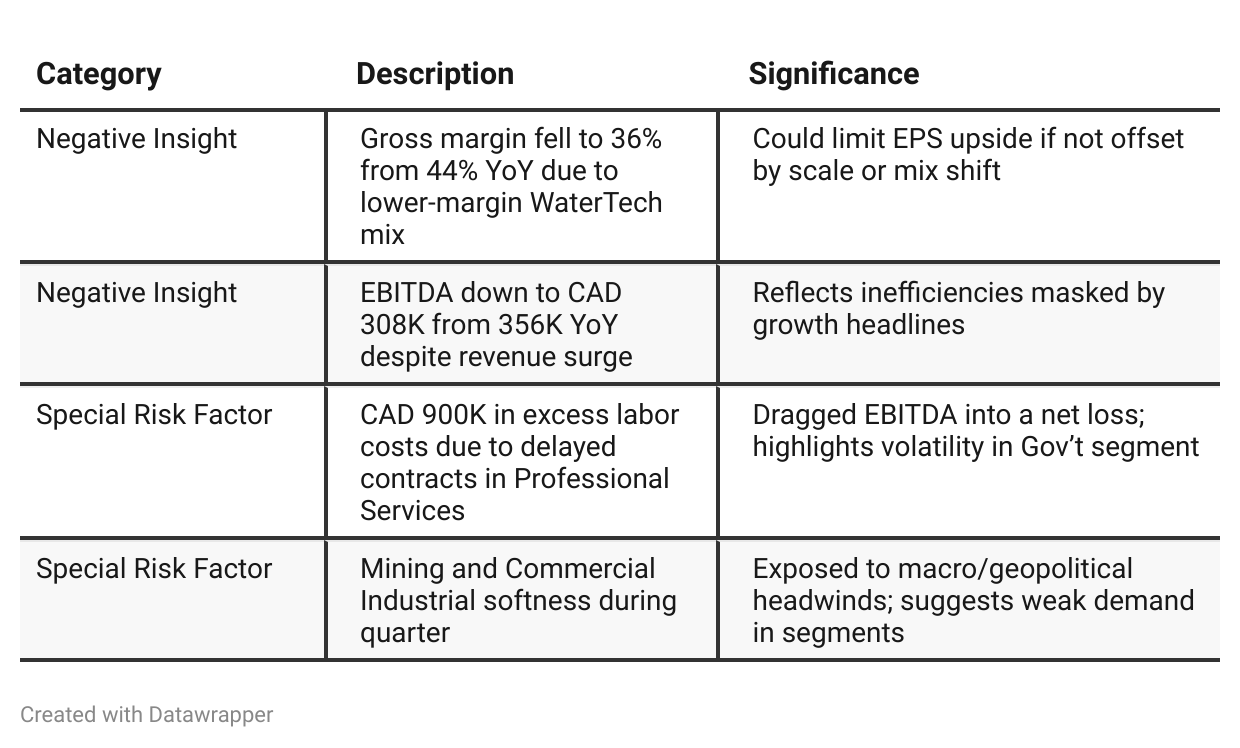

Negative Insights

Tariff Risk

Mentions of Tariffs or Trade Policies:

Indirect: Professional Services segment cited “market uncertainty stemming from U.S. trade uncertainties” as contributing to delays in government and industrial project starts.

Mitigation Actions or Commentary:

No detailed strategy provided for tariff mitigation.

Management expects recovery due to seasonality and contract awards, not structural changes.

Conclusion:

While tariff risks are not central to the business, they remain an indirect contributor to project delays. No forward-looking discussion on supply chain adjustments, sourcing changes, or pricing strategies in response to tariffs was provided.

Previous Earnings Call

Quarter-over-quarter comparison

Between Q2 and Q3 2025, BluMetric’s narrative evolved from execution under strain to strategic expansion and recovery. In Q2, management leaned on WaterTech USA’s growth to offset Professional Services weakness from Canadian election delays. The message was about resilience, holding staff, and waiting for utilization recovery.

By Q3, management was more confident, pointing to rebound in Professional Services utilization, a major Thales military contract with commercial IP potential, and actively exploring Professional Services acquisitions.

Financially, margins improved, and tone shifted from defensive (protecting capacity) to offensive—leveraging investments, diversifying revenue streams, and positioning for scale in WaterTech, Military, and Professional Services.Year-over-year comparison

Between Q3 2024 and Q3 2025, BluMetric’s narrative evolved from incremental, preparatory growth to a transformative scaling phase. In 2024, management stressed investing ahead of revenues, building manufacturing capacity, and securing credibility through initial contracts.

By 2025, the company had executed a major US acquisition, significantly increased revenues, and landed strategic military and naval contracts. However, while topline growth accelerated, margins compressed and profitability dipped, reflecting integration costs and Professional Services underutilization.

The story transitioned from “building the foundation for cleantech growth” to “leveraging acquisitions and contracts for scale, international expansion, and recurring revenues.”

Final Takeaway

BluMetric is in a growth and margin recovery phase, leveraging its WaterTech acquisition and military contracts to scale revenues.

While recurring O&M revenue and geographic expansion (Caribbean, NATO) offer strong upside, margin pressure from delayed contracts and segment mix still weigh on near-term results. Execution in Q4 will be critical to prove the operating model is scalable and margins are stabilizing.

Verdict: Hold, with upside potential if Q4 confirms utilization rebound and military growth trajectory.