BuildDirect.com Technologies Inc. (OTCQB: BDCTF) – Q2 2025 Earnings

BuildDirect.com Technologies Inc. (OTCQB: BDCTF) – Q2 2025 Earnings

Earnings Release Date: Aug. 28, 2025

Stock Price: $1.81

Market Cap: $87.0 million

Q2 2025 sales of $16.9 million vs $16.2 million in the prior year

Q2 2025 EPS of $0.01 vs $(0.01) in the prior year

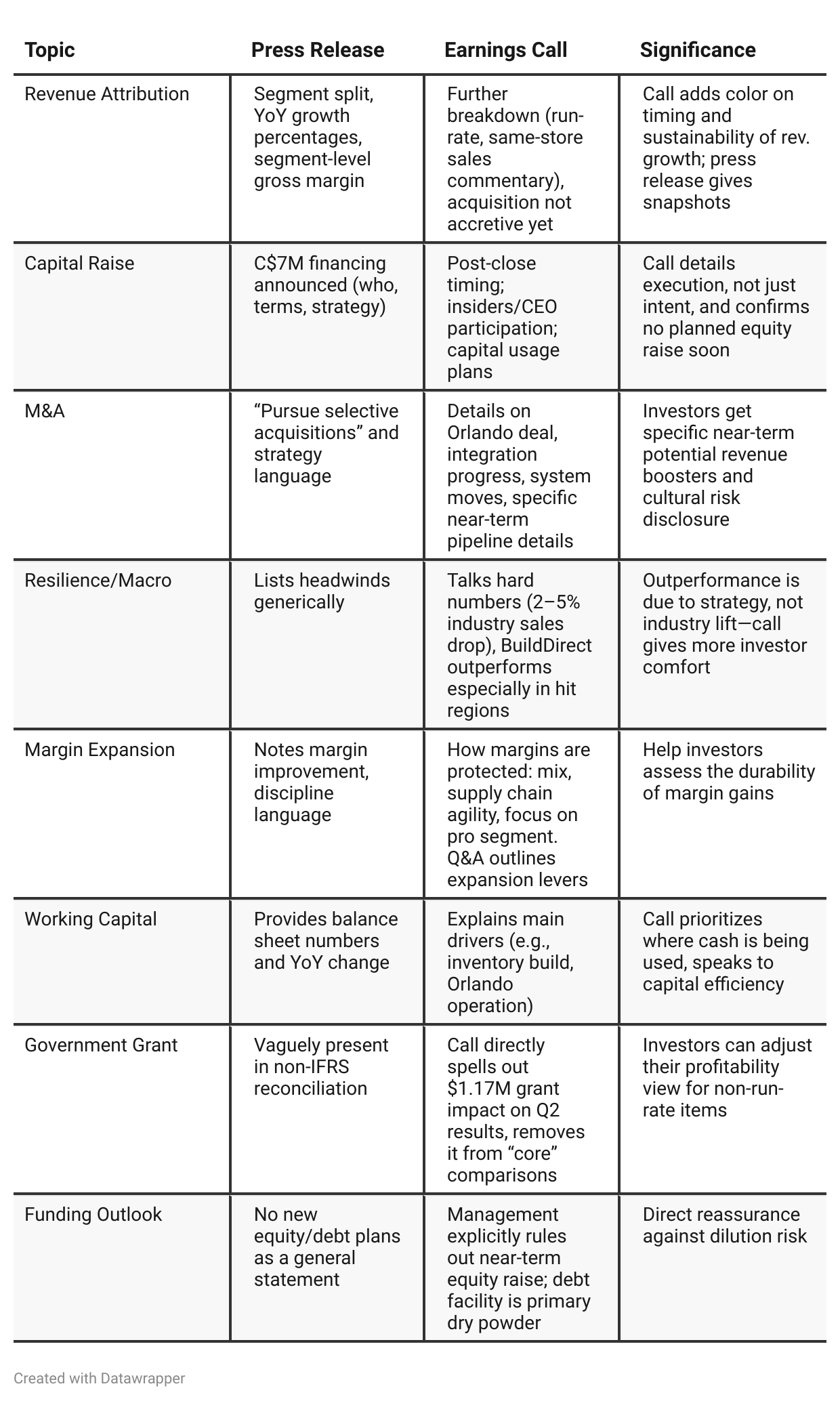

Press Release vs Call Transcript Comparison

Transparency: The call is much more forthcoming with operational color, naming risks (tariffs, Michigan), integrating financials (what’s non-recurring), and explaining segment dynamics.

Capital Allocation Discipline: Messaging shifts from growth-for-growth’s-sake (press release) to very selective, IRR-filtered M&A in the call.

Synergy and Integration: Call highlights actual post-acquisition synergies (ERP integration, shared inventory, cost savings), not just acquisition numbers.

Timing on Growth: E-commerce ramp is not “guidance” in the press release but is timeline-specific in the call (Q4 and 2026 acceleration).

Balance of Channels: Call hierarchy of channel investments and synergies is clearer—Pro Centers fund, and cross-benefit, e-commerce and vice versa.

Risk Management: Call is candid on ongoing restructuring costs and cost profile improvement, less visible in press release.

Cost Management and OpEx: The call explains that operating expense growth is due to specific, temporary items (new center); underlying costs are flat, suggesting operating leverage.

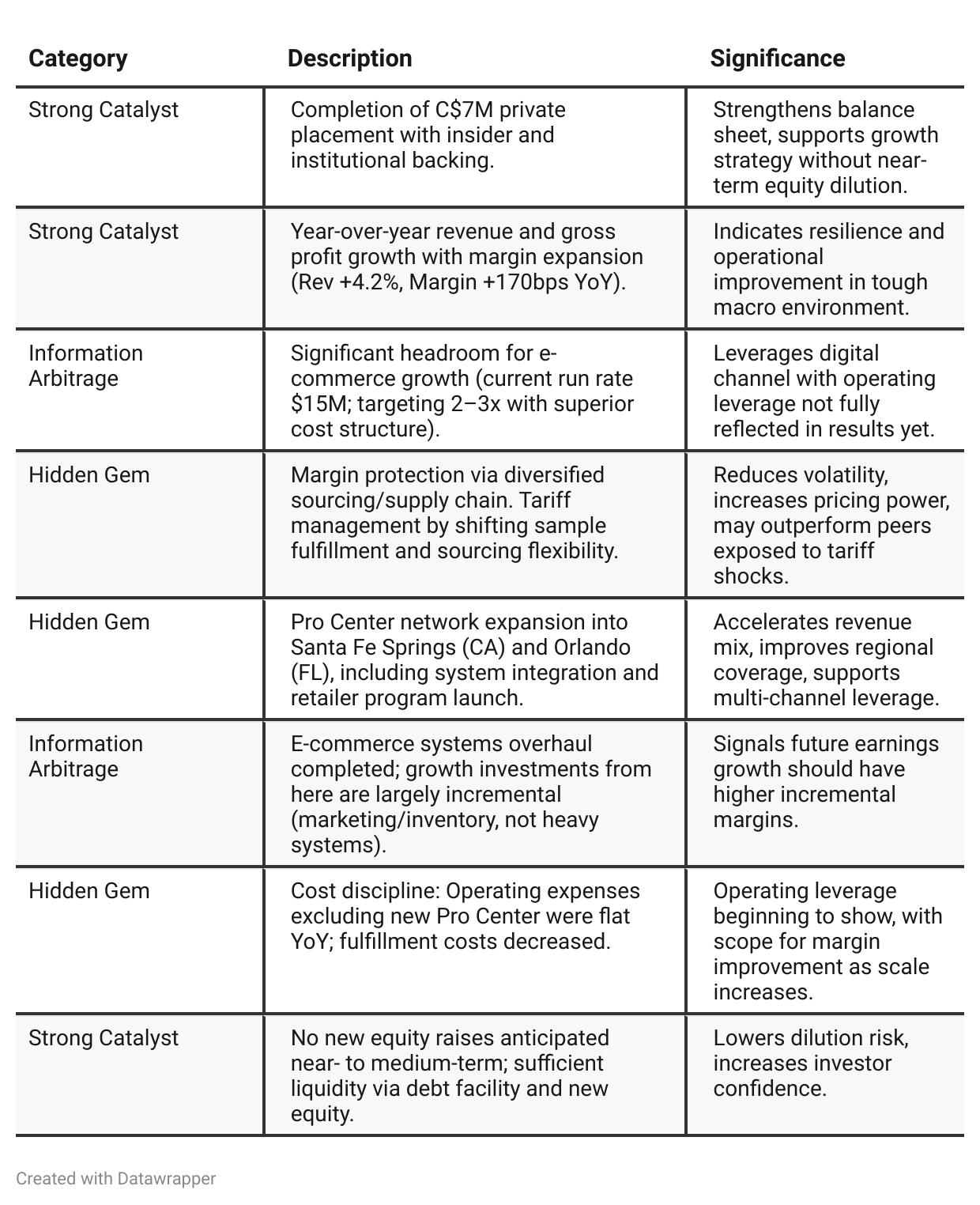

Positive Insights

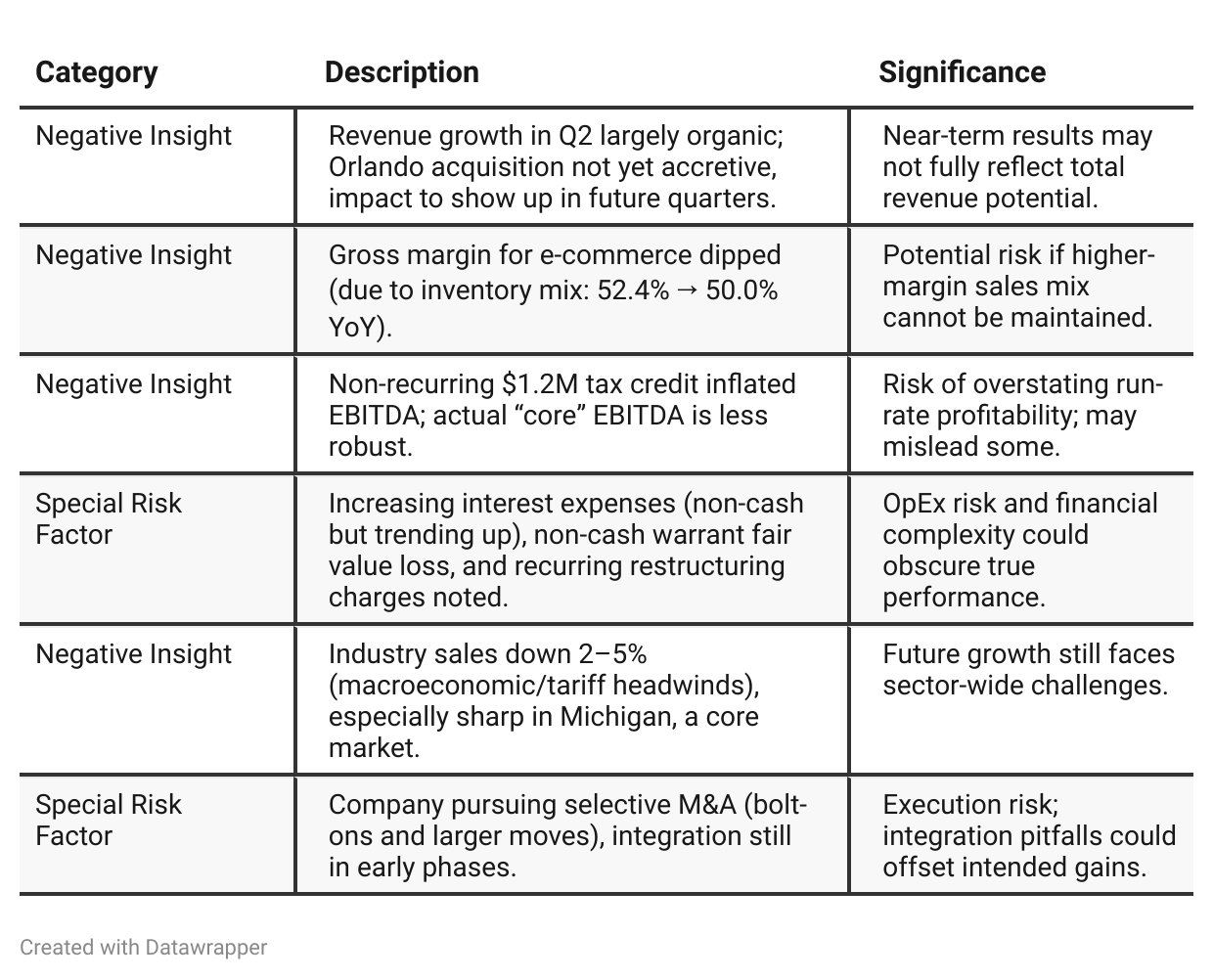

Negative Insights

Tariff Risk

Tariff Risk Analysis:

Management explicitly cited US tariffs as a material headwind impacting the sector, with Michigan (a core market) being “hard hit.”

Mitigation measures mentioned:

Shifted sample distribution from DC to Michigan to avoid additional tariffs.

Direct sourcing from multiple countries, not just China, for flexibility.

Dual supply (direct import + distribution) provides optionality and allows quick shifts in response to tariff fluctuations.

Competitive Advantage:

Management highlighted that competitors without this flexibility are “captive” to disruptions, suggesting a relative market share and margin advantage.

Market Impact:

Company claims its model held up “very well despite the headwinds;” positioned to absorb or pass through tariffs better than others.

Forward-looking:

Management expects continued vigilance; monitoring supply mix and keeping Pro Center focus to protect margin.

Conclusion: BuildDirect is proactively managing tariff risk through operational flexibility and diverse sourcing. While tariffs have impacted the broader sector and local demand, especially in Michigan, BuildDirect’s approach appears to provide resilience and potential outperformance relative to peers, although ongoing monitoring is required.

Previous Earnings Call

Quarter-over-quarter comparison

Earlier Call (Q1 2025): BuildDirect is laying the foundation for future growth by building operational efficiency, integrating a notable acquisition (Anchor YorkShore), and putting in place strict cost discipline. The focus is on “getting ready” and proving that the model works, with prudent capital use and no overreaching promises.Current Call (Q2 2025): BuildDirect presents itself as ready for the next level, having optimized its platform and strengthened its balance sheet via a significant equity raise. The company is shifting gears from foundational work (cost control, integration, set-up) to aggressive pursuit of growth, both organically (particularly through e-commerce) and via synergistic bolt-on acquisitions. Management demonstrates higher confidence, greater clarity of strategic direction, and provides visibility into upcoming growth drivers while remaining openly committed to capital discipline and margin resilience in the face of macro and tariff headwinds.

Year-over-year comparison

—

Final Takeaway

BuildDirect is in an expansion and operational leverage phase, focusing on scaling omni-channel sales growth via Pro Center expansion and e-commerce acceleration. While management has bolstered its balance sheet and protected margins with supply chain flexibility, sector headwinds and risks to integration/execution remain. Delivery of promised organic and acquisition-driven scale-up will be critical. Verdict: Hold—watch for growth from new locations and evidence of e-commerce ramp.