AXT, Inc. (NASDAQ: AXTI) – Q3 2025 Earnings

AXT, Inc. (NASDAQ: AXTI) – Q3 2025 Earnings

Earnings Release Date: Oct. 30, 2025

Stock Price: $7.07

Market Cap: $309.0 million

Q3 2025 sales of $28.0 million vs $23.6 million in the prior year

Q3 2025 EPS of -$0.04 vs -$0.07 in the prior year

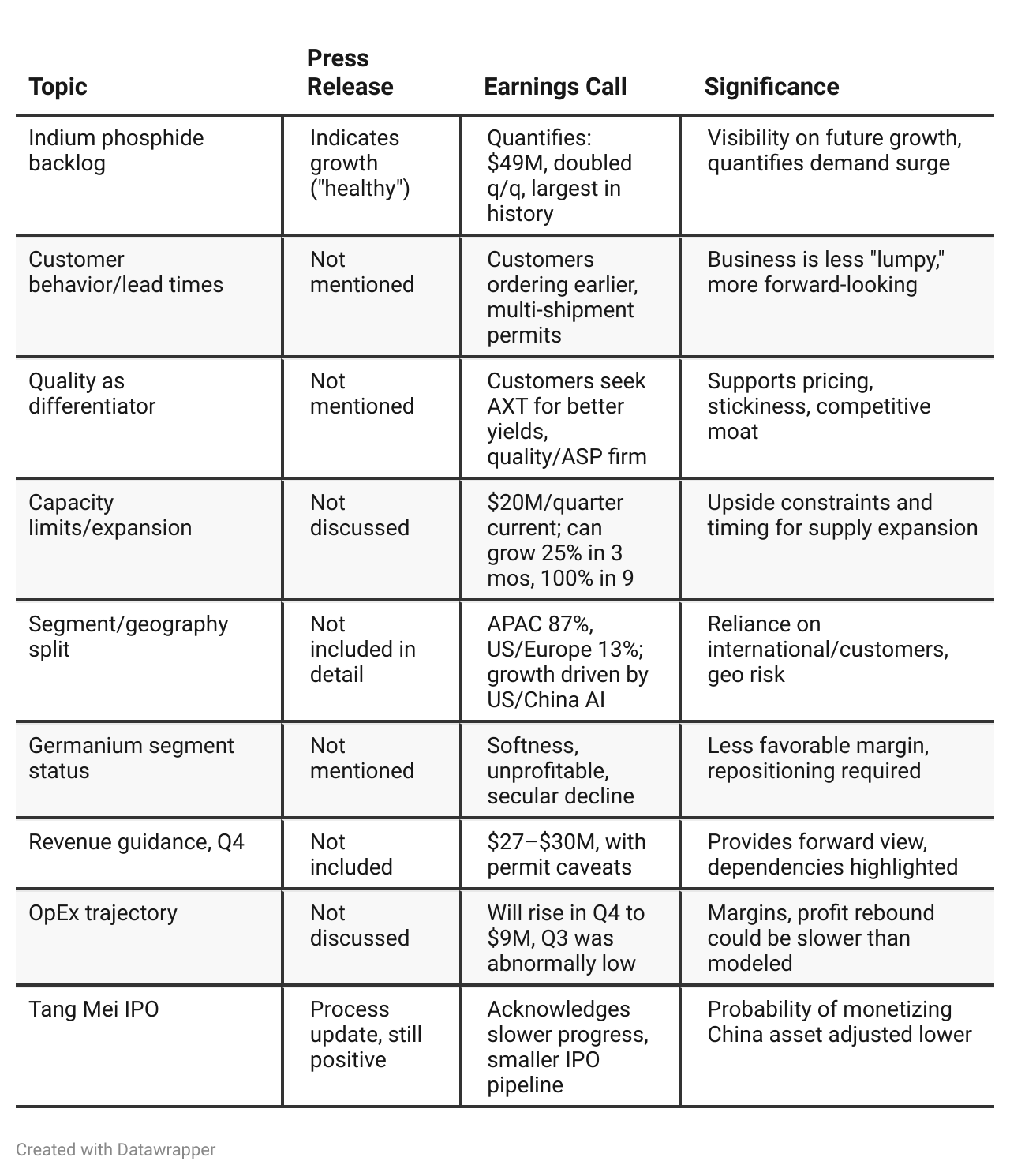

Press Release vs Call Transcript Comparison

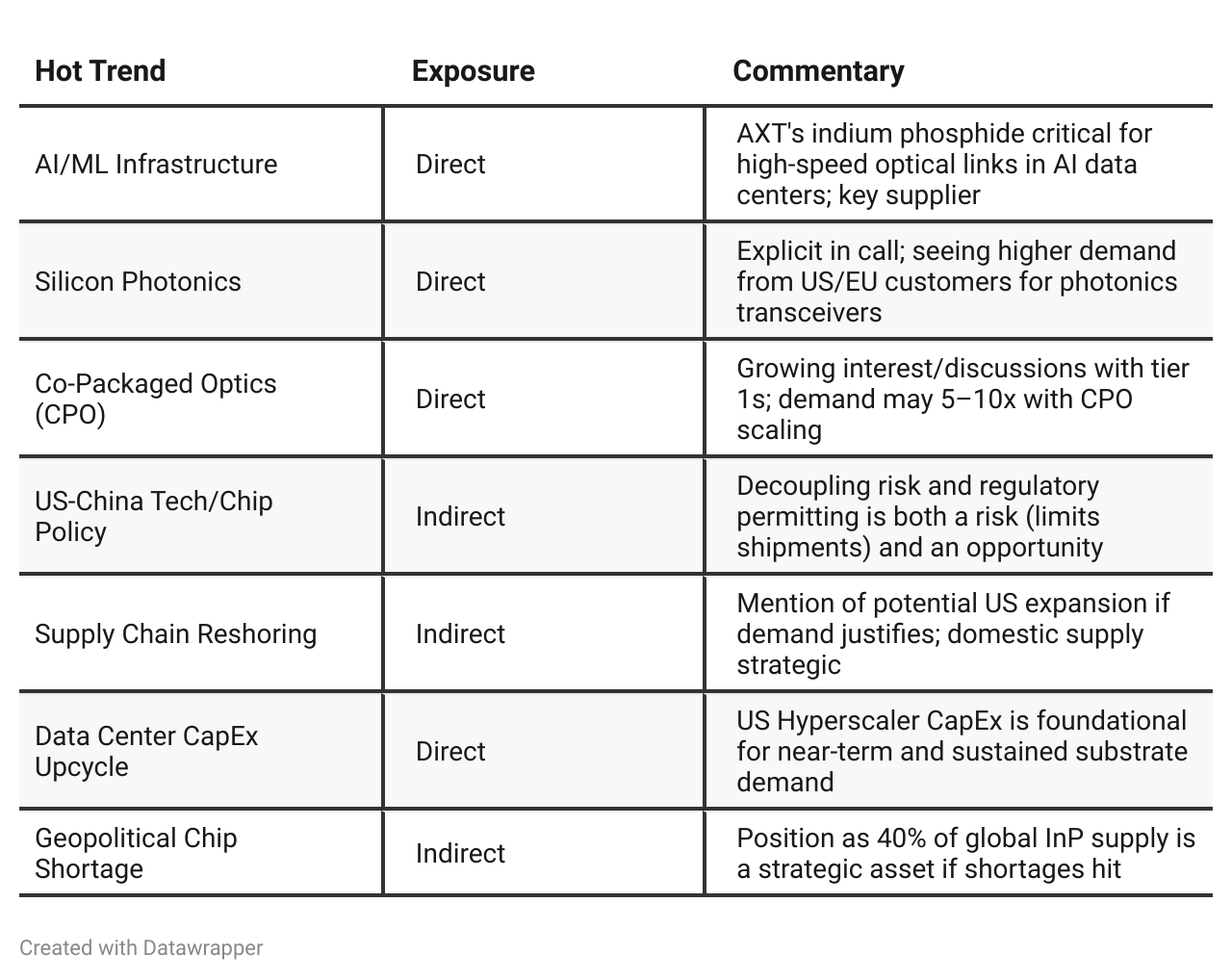

Speculative Hot Trend Exposure: The earnings call gives explicit links to AI data center buildouts, silicon photonics, CPO (co-packaged optics)—all major market themes. The press release does not make these “trendy” connections as directly.

Customer Relationships Deepening: Direct conversations with customers’ customers (hardware, GPU/CPU makers), showing deep integration.

Inventory & Receivables Working Capital: Cash draw in Q3 is due to AR rises (tied to permit timing), not operational cash burn.

Global/Geopolitical Leverage & Risk: US/China interdependence can create catalysts or sudden downside.

Levers to Higher Margin: Margin improvement not tied to price hikes, but efficiency, mix, and scale—less risky, possibly more durable.

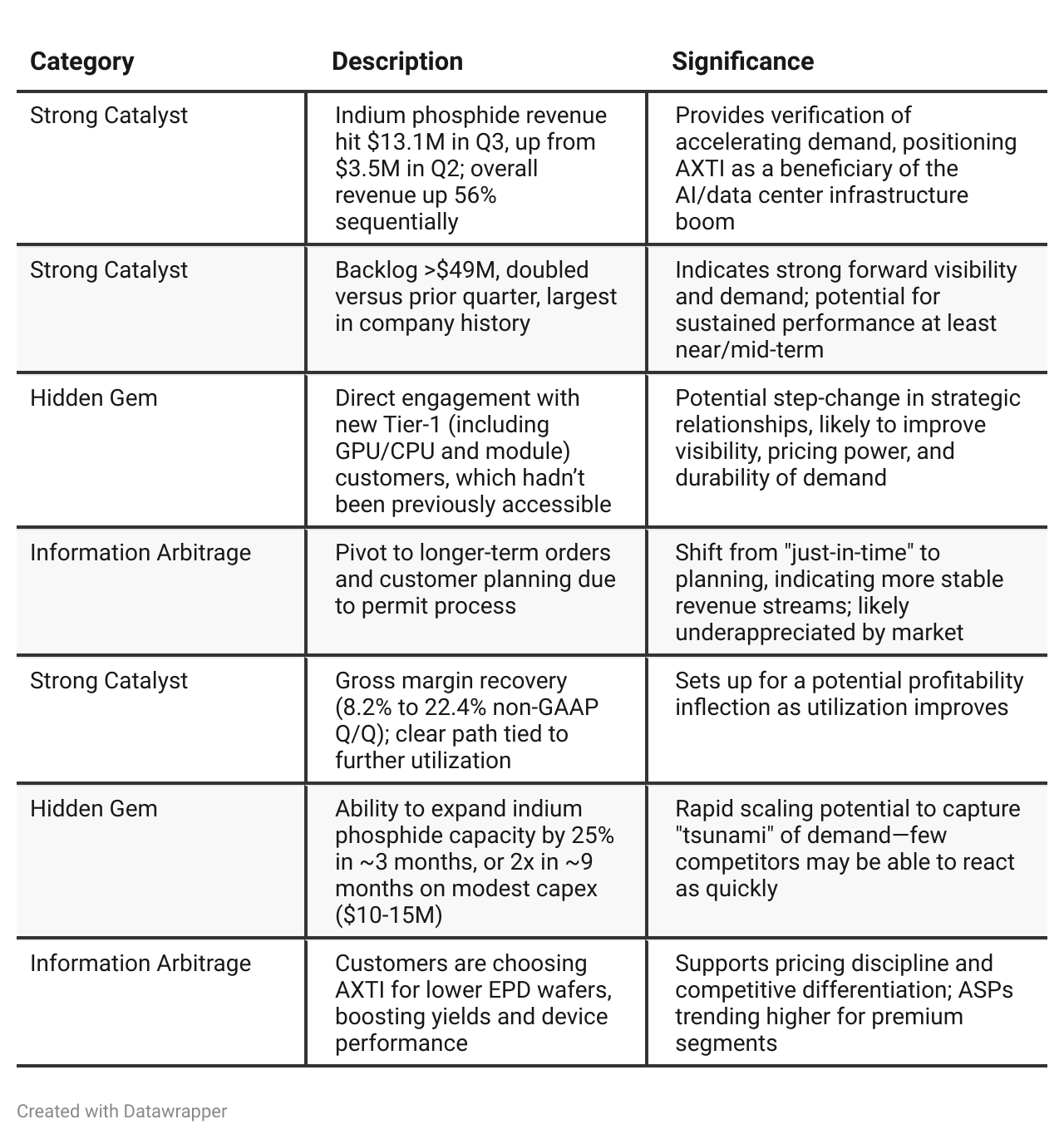

Positive Insights

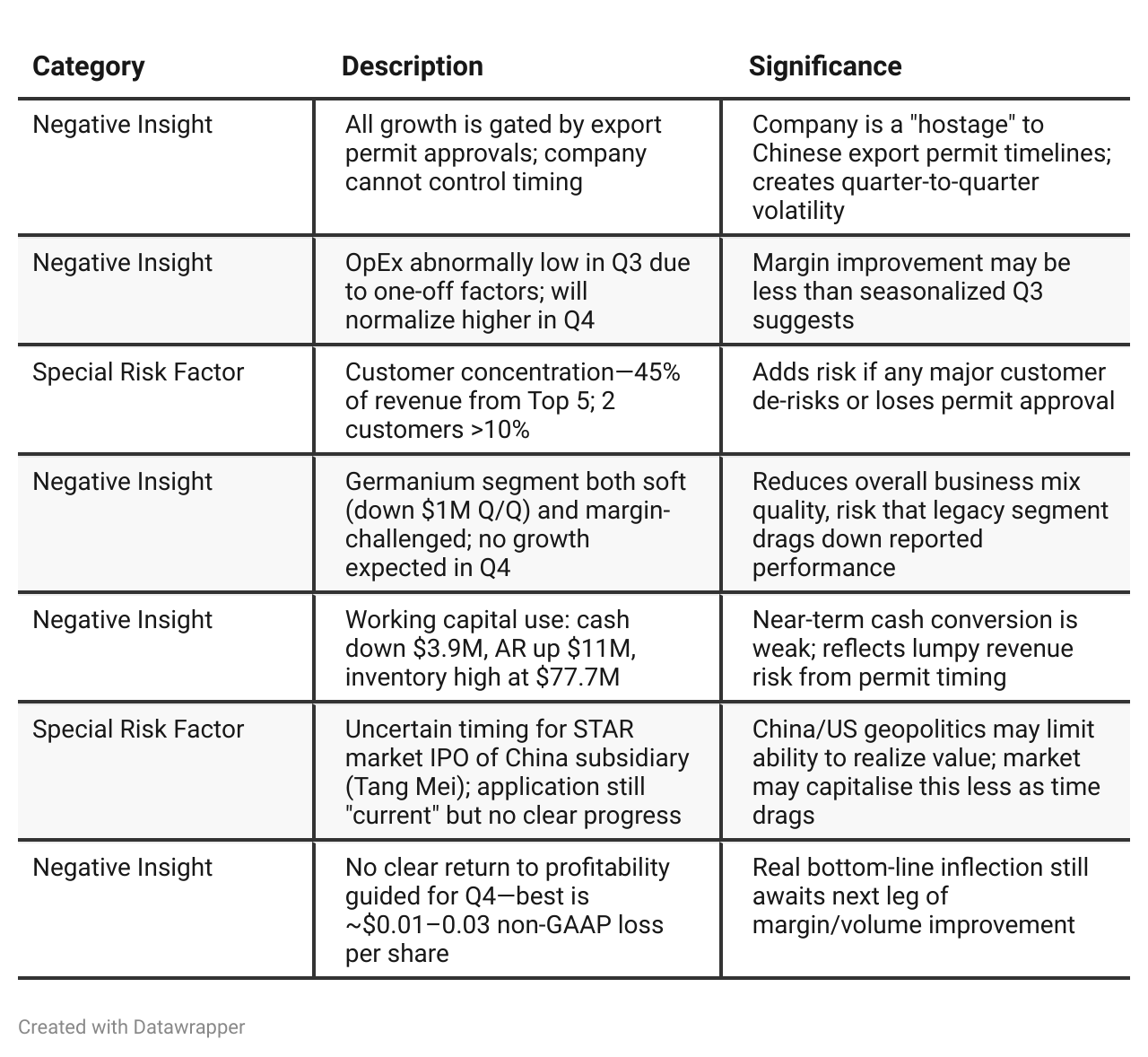

Negative Insights

Tariff Risk

AXTI’s growth is tightly constrained by Chinese export permit approvals, which function as a proxy for trade/tariff restrictions.

The company cannot recognize revenue or ship product to many overseas customers without these permits; the process is slow and unpredictable.

Management is proactively building inventory while awaiting permits but acknowledges this risk is outside their control.

No major supply chain restructuring has been done yet, but U.S. capacity expansion may be considered if trade restrictions worsen.

Bottom line: Growth and cash flow depend on ongoing access to export licenses; any tightening of trade policies or new tariffs would sharply limit upside, while stable permit flow is key to delivering current backlog and further growth.

Hot Stock Trends Analysis

Previous Earnings Call

Quarter-over-quarter comparison

In Q2, AXTI was portrayed as a company fighting through adversity—permit delays, weak demand in China, and persistent losses—but sowing seeds for a future upturn if obstacles could be overcome. Messaging was defensive and cautionary, with only glimmers of optimism around order backlog and margin recovery.By Q3, the narrative had decisively shifted: record sequential growth, a “tsunami” of demand driven by the AI/data center hardware cycle, record backlog figures, and real traction with large, high-value international technology customers. Instead of simply fighting fires, the company is now positioning itself as a strategic, essential supplier with growing influence and visibility, guided more by the pace of opportunity than risk control, though still acknowledging the real gating threat of permit approvals.

Year-over-year comparison

Q3 2024: AXTI was cautiously optimistic, focused on selective revenue, gross margin discipline, and promising but largely “potential” growth in AI/data centers. China’s macro and regulatory slowdowns, rising raw material costs, and muted IPO prospects defined the risk landscape. Customer wins and sector shifts (AI/silicon photonics, HPTs) were early stage, with improvement tied to market and process stabilization.

Q3 2025: AXTI’s narrative has powerfully shifted. The company is now a critical bottleneck supplier to the AI/data center optical ecosystem—with surging demand materializing in the form of record revenues and backlogs, and rapid onboarding of global Tier-1 customers. Internal focus has turned from survival and margin defense to proactively scaling capacity and customer engagement. While export permits still throttle upside, overall tone is of opportunity management rather than crisis navigation. The business is now poised as a levered play on secular global tech trends—with the major challenge being how fast AXTI (and policymakers) can execute, not if AXTI will participate.

Final Takeaway

AXTI is in a growth and strategic repositioning phase, capitalizing on surging global demand for indium phosphide in AI/data center optical applications. While record backlog, improving margins, and new tier-1 customer wins are strong positives, the company’s growth is tightly gated by Chinese export permit timing, concentration among key customers, and rising OpEx/working capital needs. Execution on permit flow, margin expansion, and cash discipline will be crucial for upside. Verdict: HOLD—significant upside if operational bottlenecks clear, but the permit constraint is too critical to ignore for aggressive buying.