Axalta Coating Systems Ltd. (NYSE: AXTA) – Q3 2025 Earnings

Axalta Coating Systems Ltd. (NYSE: AXTA) – Q3 2025 Earnings

Earnings Release Date: Oct. 28, 2025

Stock Price: $29.06

Market Cap: $6247.9 million

Q3 2025 sales of $1.2 billion vs $1.3 billion in the prior year

Q3 2025 EPS of $0.51 vs $0.46 in the prior year

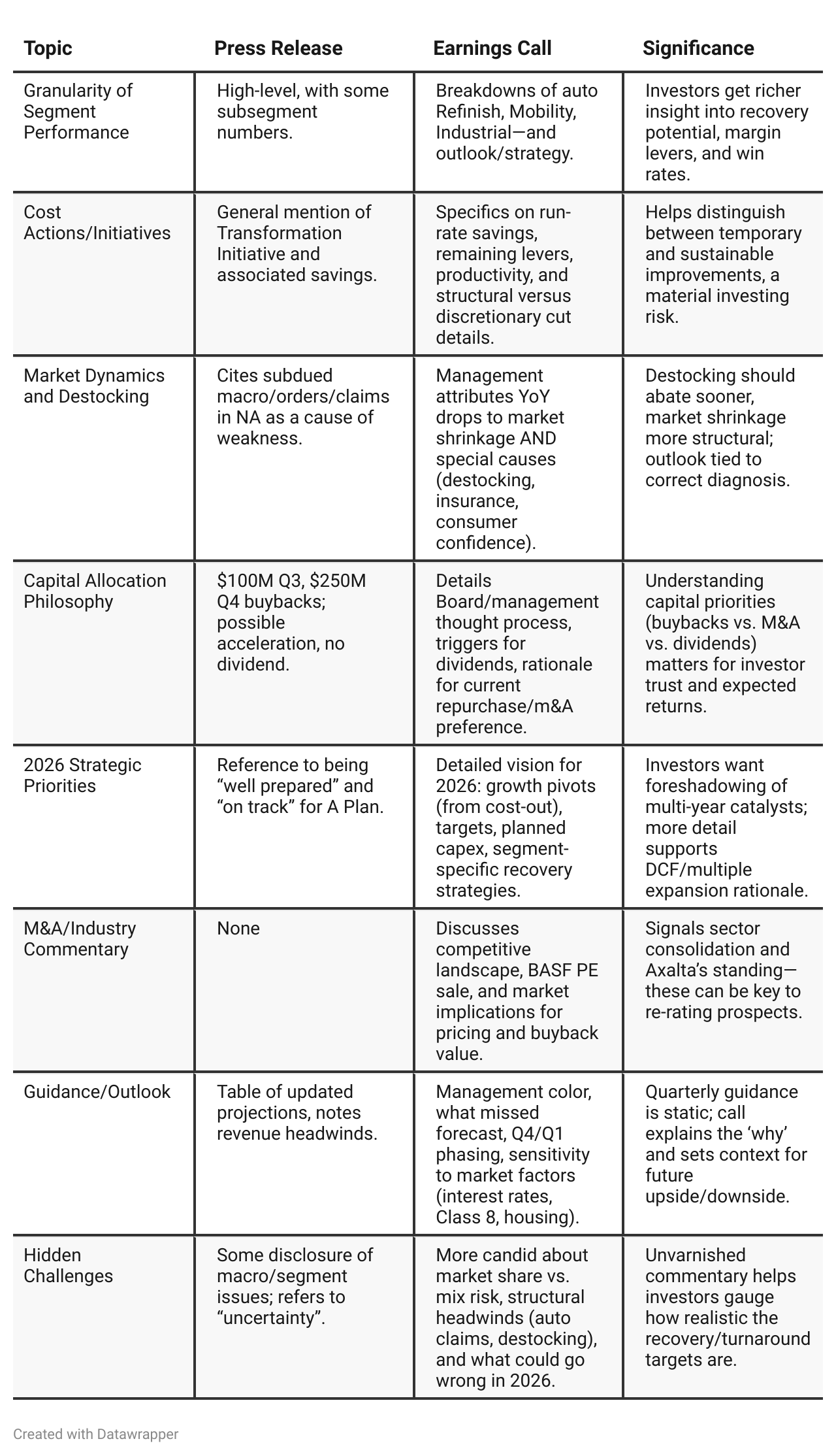

Press Release vs Call Transcript Comparison

The call gives much more context on the “future-proofing” of Axalta: How management is thinking about operational resilience, segment pivots (especially Commercial Vehicles), new adjacencies, and what happens if recovery is delayed.

Dividends: The press release is silent on dividends, while the earnings call clarifies that a dividend is under board consideration as part of a future “A Plan,” but not likely imminent. This is significant because Axalta is an outlier in the chemicals sector in not paying a dividend, and initiating one could serve as a positive catalyst or help attract a new class of investors.

Management Confidence vs. Macro Risks: The consistent tone of confidence in the earnings call (e.g., “a record year,” “very excited for 2026”) provides reassurance, but is underpinned by candid acknowledgement of macro uncertainty and segment-specific risks. This duality helps investors gauge both upside and potential downside.

Operational Flexibility: The call illuminates the company’s focus on cost control, structural improvements (not just temporary measures), and capital flexibility. Willingness to pivot capex, maintain operational discipline, and pursue smaller bolt-on M&A versus large deals suggest prudent capital stewardship.

Competitive Environment and M&A: The call, not the release, highlights the PE acquisition of BASF’s Refinish unit and the read-through to Axalta’s valuation and sector discipline. This provides both context for share repurchases (as undervaluation is implied) and the potential for sector-wide efficiency/consolidation.

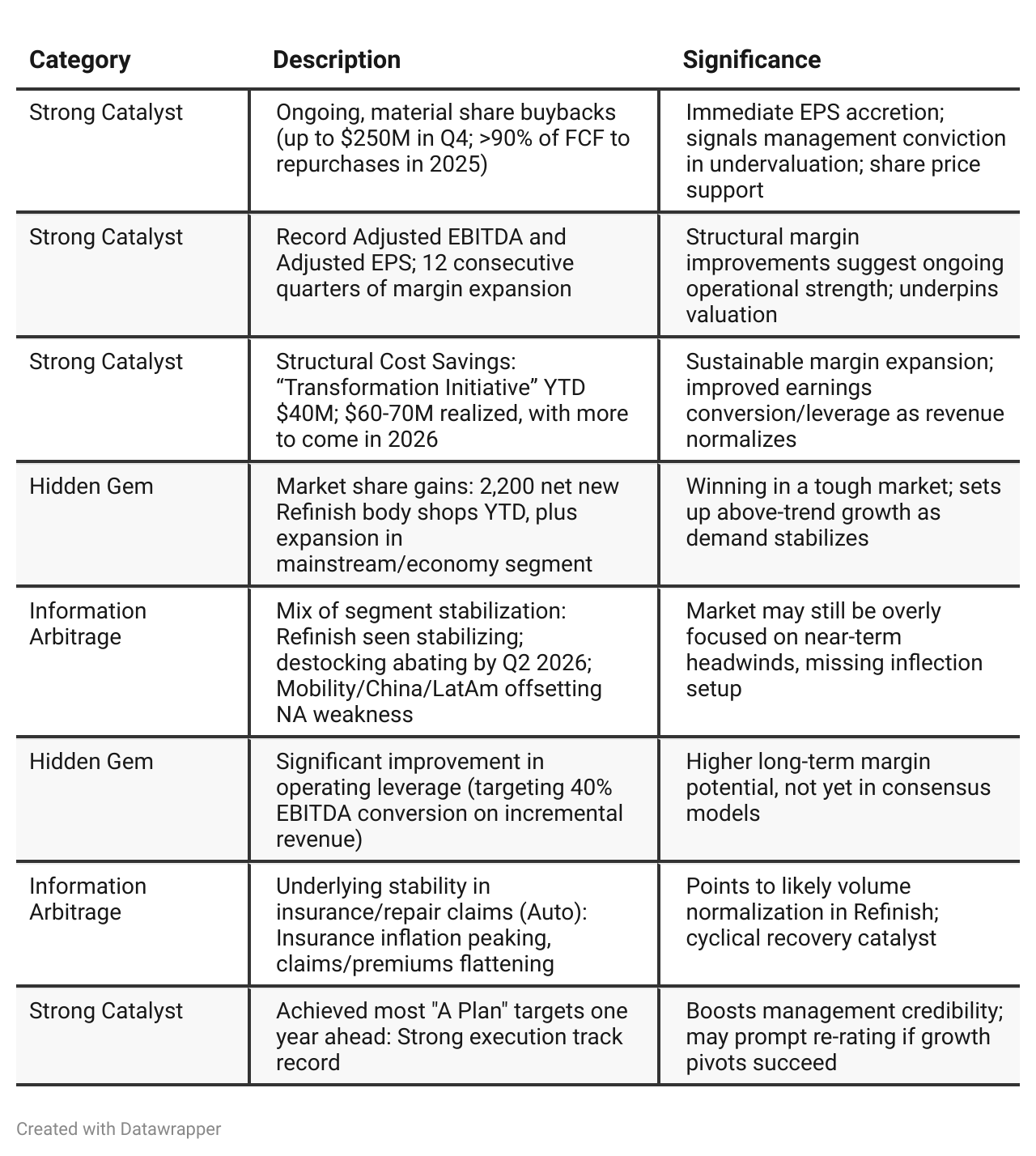

Positive Insights

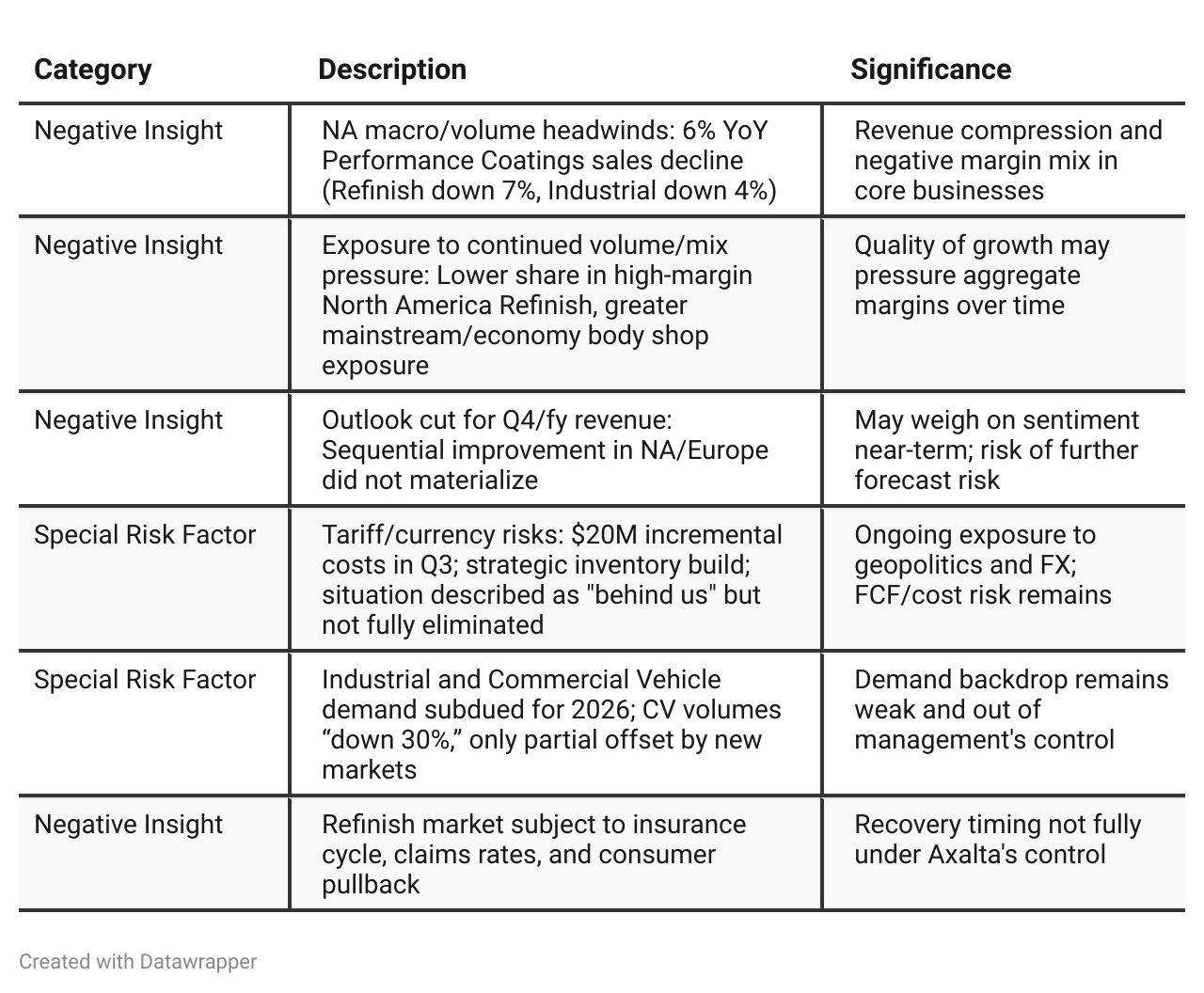

Negative Insights

Tariff Risk

Q3 saw intentional inventory build due to “tariff uncertainty in North America” and Brazil (for business ramp). This affected FCF but is expected to unwind (release cash Q4).

Management quantified ~$20M in incremental tariff-related costs but claims these have been managed effectively. There is optimism that major incremental headwinds are “behind” them; however, they caution that “you never know.”

No explicit mention of lost market share, but Axalta highlights its ability to navigate through the environment and maintain cost/margin discipline.

Adjusted pricing and strategic inventory planning were key mitigation tactics. No mention of relocating manufacturing, supplier shifts, or renegotiated contracts.

Forward-Looking View: Management expects the raw material cost environment—including tariffs—to remain stable for at least the next three to four quarters. They view the bulk of recent tariff-related cost pressure as now largely behind the company, but acknowledge ongoing vigilance is required (“you never know”).

Mitigating Actions:

Strategic Inventory Management: Inventory levels were intentionally increased to address tariff uncertainty, especially in North America and Brazil.

Cost Pass-Through and Pricing: Some costs have been absorbed or managed through pricing and cost optimization.

Operational Flexibility: No supply chain relocations or contract renegotiations mentioned, but management emphasizes adaptability should conditions change.

No Material Impact on Innovation or Market Share: The transcript does not indicate that tariffs have impacted Axalta’s competitive innovation or its ability to win new business. In fact, Axalta reports strong new shop wins and continued share gains in target segments.

Risk Remains on Forward-Looking Basis: While the worst appears over for now, ongoing monitoring is needed due to the inherently unpredictable nature of tariffs and the macro/political backdrop.

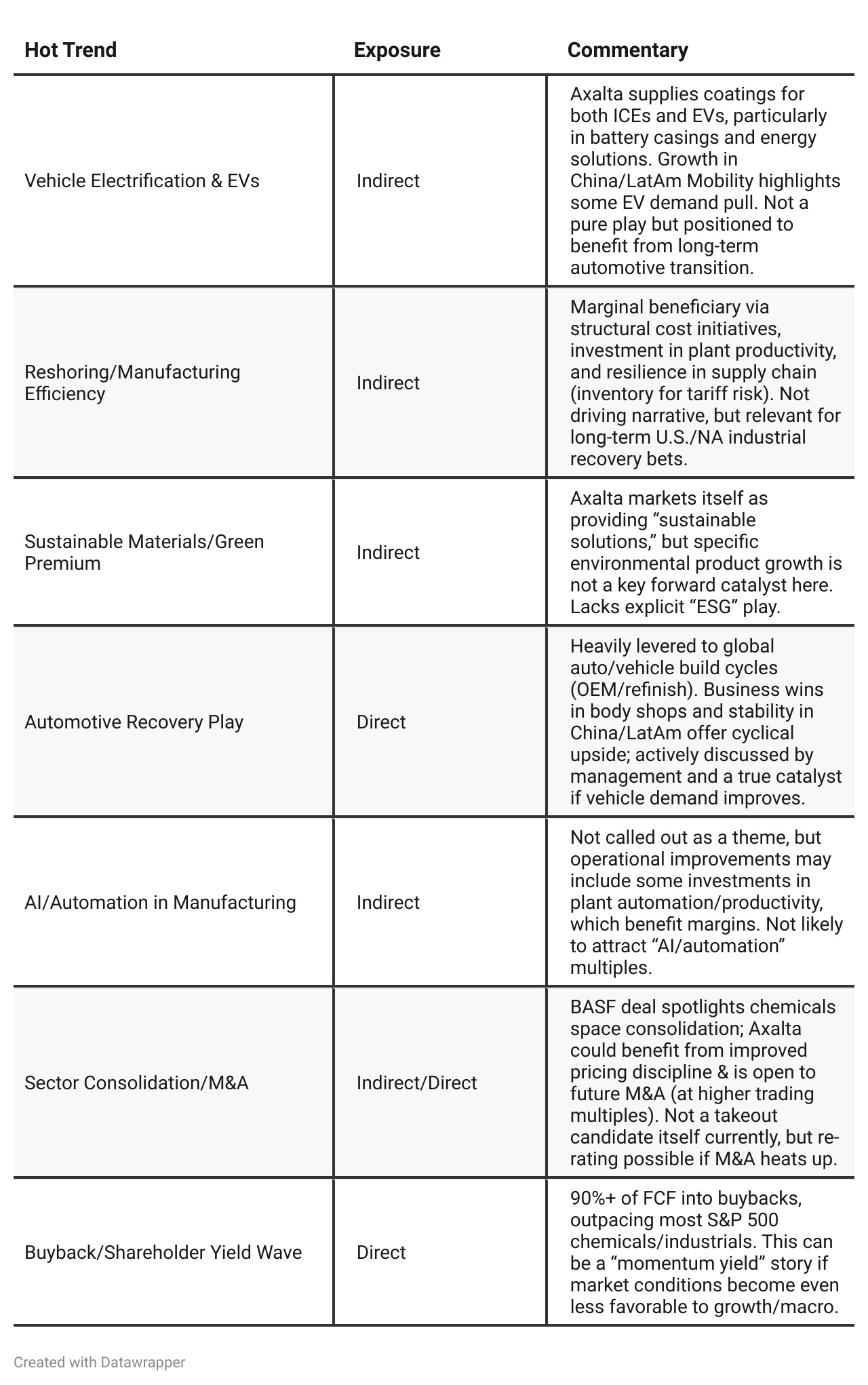

Hot Stock Trends Analysis

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Q2 2025: Axalta is positioning itself as a cost and efficiency leader, winning share in key categories, and deploying capital in a balanced way between buybacks and targeted M&A. Management projects cautious optimism that challenging end markets (especially Refinish North America) are near stabilization and that margins are poised to expand as any cyclical recovery emerges.Q3 2025: The narrative matures: Axalta now fully embraces margin, cash flow, and capital returns as the core of shareholder value, even in the face of continued top-line weakness. Management is more aggressive in buybacks, openly touts the stock as undervalued, and delays expectations for real demand recovery (especially in Refinish and North America) until the second half of 2026. There’s a new emphasis on sector M&A, share accretion, and structural margin leadership, with less focus on near-term growth and more on navigating macro challenges with discipline.

Year-over-year comparison

Q3 2024: Axalta was riding strong operational momentum—beating, raising, and accelerating its A Plan targets, winning new accounts and growing volumes even in a tough macro. The story was about how cost discipline, segment leadership, and focused innovation could drive not only outperformance but an acceleration of longer-term growth targets. M&A and buybacks were positioned as part of a balanced, opportunistic capital strategy.

Q3 2025: Faced with persistent external headwinds and revenue drag, Axalta’s tone is more pragmatic and resilient. The narrative has shifted to “margin, cash, and capital return above all”—from growth chasing to value creation through structural efficiency and capital discipline (massive buybacks, operational rigor). While innovation and share gains remain, the focus is on extracting value now and waiting for macro recovery (particularly in North America and Industrial/Refinish) to reaccelerate top-line growth in 2026. The company positions itself as undervalued, highly disciplined, and prepared for upside when cyclical trends finally turn.

Final Takeaway

Axalta is in a late-cycle stabilization phase with strong operational/cost execution and a compelling capital return story. Management is credible and prioritizes value creation through buybacks and strong margin discipline. However, NA end market/revenue headwinds and global macro uncertainty remain pronounced. Investors should focus on inflections in Refinish volumes and Industrial demand, as well as sustained operational leverage. The verdict is HOLD, with meaningful upside possible on evidence of cyclical demand normalization or faster realization of projected catalysts.