Astronics Corporation (NASDAQ: ATRO) – Q2 2025 Earnings

Astronics Corporation (NASDAQ: ATRO) – Q2 2025 Earnings

Earnings Release Date: Aug. 6, 2025

Stock Price: $35.84

Market Cap: $1292.3 million

Q2 2025 sales of $204.7 million vs $198.1 million in the prior year

Q2 2025 EPS of $0.38 vs $0.04 in the prior year

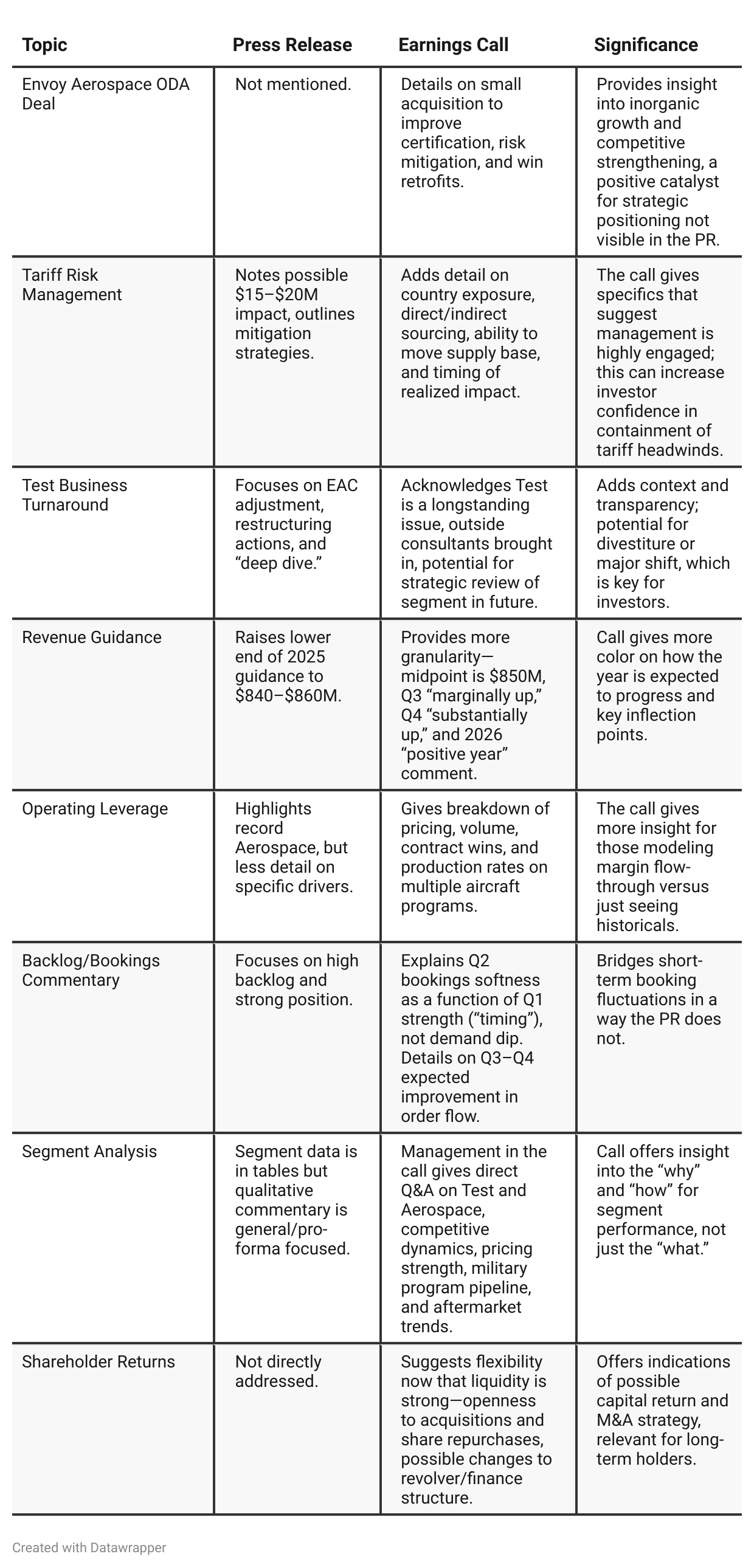

Press Release vs Call Transcript Comparison

Tone and Candor: The call exhibits more candor (esp. about Test challenges), balancing optimism for Aerospace against realism on risks.

Aftermarket and Retrofit: The call specifies the enduring strength in retrofit work, suggesting recurring revenue and lower cyclicality versus the OEM cycle.

Pricing Power: Detailed examples of price negotiation success with major customers indicate a more favorable inflationary pass-through than many industrials/aerospace suppliers.

Investor Focus: The call’s Q&A confirms the hot-button areas for investors: tariffs, margins, Test drag vs. divestiture, aerospace ramp pace, and capital allocation.

Execution Track Record: The PR’s focus is on results and one-off charges. The call attempts to frame “messy” results (EAC charges, restructuring) as evidence of management taking tough but necessary actions to strengthen long-term performance.

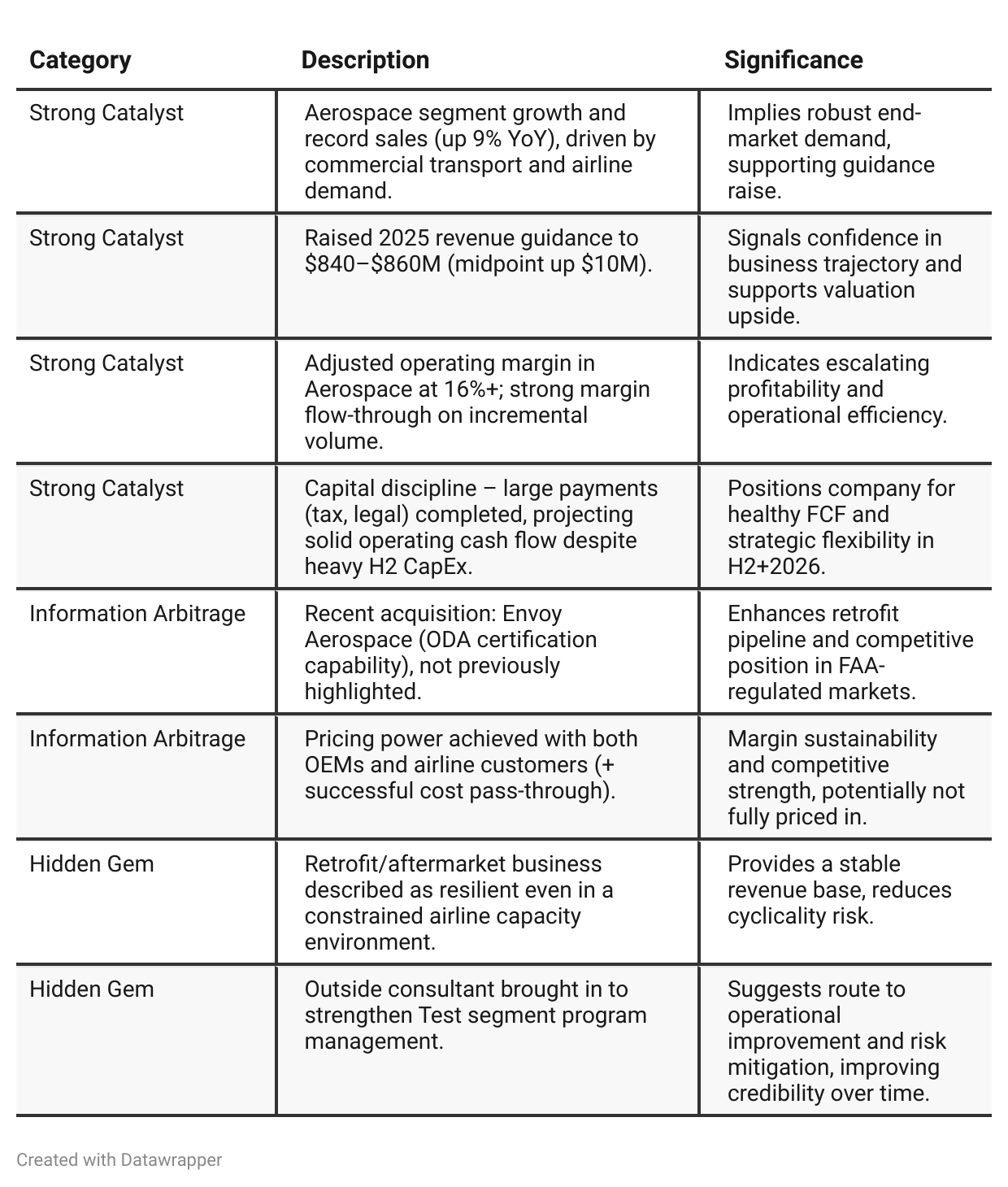

Growth Algorithm: The combination of revenue guidance raise, pricing success, operational leverage, and new accretive acquisitions (ODA/Envoy) all suggest the core business is not just stable but accelerating.

Potential ‘Hidden Optionality’: Not directly highlighted in the PR—acquisition strategy, possible Test segment review/sale, and further leverage to both supply chain and scale in core aerospace.

Positive Insights

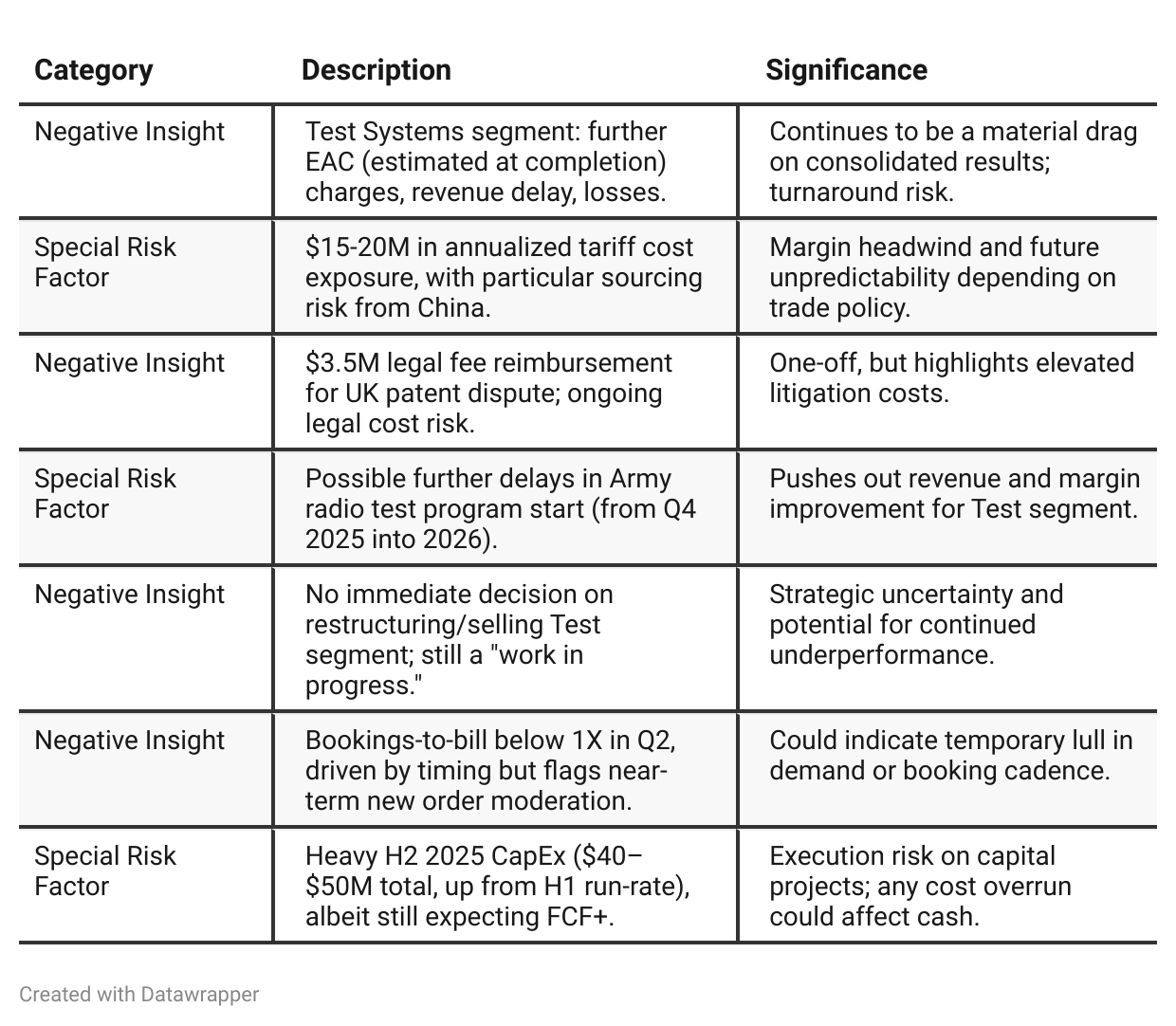

Negative Insights

Tariff Risk

Discussion: Management cited $15–$20M annualized cost impact from new tariffs, with about half coming from Malaysian sources (resourceable—can switch supply), and another quarter from China (harder to mitigate). Pricing power and various mitigation strategies—including supply chain shifts, bonded warehouses, and duty drawback—were emphasized as active offset actions.

Market Effects: Tariffs are recognized as a margin headwind, but mitigation plus strong pricing power might reduce the net effect. The company appears positioned not to lose share or competitive advantage due to tariffs, though near-term volatility risk remains. No suggestion that tariffs will impede innovation or key programs.

Forward Looking: Management is optimistic about reducing tariff impact via mitigation and pricing, but acknowledges unpredictability, especially with China. The situation will require ongoing monitoring.

Investor Take: Tariff risk is bona fide—but, per management’s tone and actions, appears manageable and non-thesis-breaking assuming current mitigation plans execute.

Previous Earnings Call

Quarter-over-quarter comparison

Q1 2025: Astronics enters the year with strong momentum, highlighting operational improvements, record aerospace performance, and a robust pipeline. Management expresses confidence in both their ability to handle emerging tariffs and resolve lingering legal issues, while acknowledging ongoing Test segment work and some product-level cleanup to come. The overall message is one of strength, discipline, and positive outlook, with caveats around macro uncertainty and a need for vigilance.Q2 2025: The company tightens its focus further, executing on portfolio simplification by exiting underperforming lines and restructuring, while double-downing on operational excellence (external consultants for Test, operational leverage in Aerospace). Strong margin performance and pricing power become more central themes, and management is candid about areas needing improvement, giving more specific plans for accountability and timeline. New opportunities (Envoy ODA) reflect a shift to competitive differentiation through capability, not just scale. The narrative has become more process-driven and “quality over quantity,” signaling a business shifting from broad-based growth to disciplined, high-margin execution—reinforcing investor confidence in durability, not just momentum, as the story evolves.

Year-over-year comparison

2024: Astronics returns to pre-pandemic growth, led by aerospace, and fixes operational/financial weaknesses. The narrative is one of broad-based recovery, strong order intake, and taking steps to resolve legacy problems (Test, supply chain, debt).

2025: The company pivots from just growing/recovering to systematically increasing the quality of its earnings: divesting non-core assets, rigorously managing margin, and focusing on scalable, high-return programs. There’s an increased willingness to “clean house,” adopt outside help where needed, and tighten the focus on differentiated competitive strengths (e.g., FAA certification). Capex and opex discipline, as well as explicit management of macro and industry risks, signal a company moving from post-crisis recovery to optimized, resilient performance.

Final Takeaway

Astronics is in a growth and operational improvement phase, capitalizing on the strength of its aerospace business while managing through lingering structural and contract risks in Test Systems. Key growth drivers are increasing aircraft build rates, adoption of modern cabin/IFEC technologies, and aftermarket resilience, offset by ongoing Test turnaround efforts and moderate tariff risk. Execution on cost containment, segment profitability, and program timing (particularly in Test) will be critical for sustained stock outperformance. Verdict: Buy, with meaningful upside potential if Test segment recovery proceeds and aerospace margin/volume execution persists.