Assertio Holdings, Inc. (NASDAQ: ASRT) – Q2 2025 Earnings

Assertio Holdings, Inc. (NASDAQ: ASRT) – Q2 2025 Earnings

Earnings Release Date: Aug. 11, 2025

Stock Price: $0.73

Market Cap: $69.9 million

Q2 2025 sales of $28.8 million vs $30.7 million in the prior year

Q2 2025 EPS of ($0.17) vs ($0.04) in the prior year

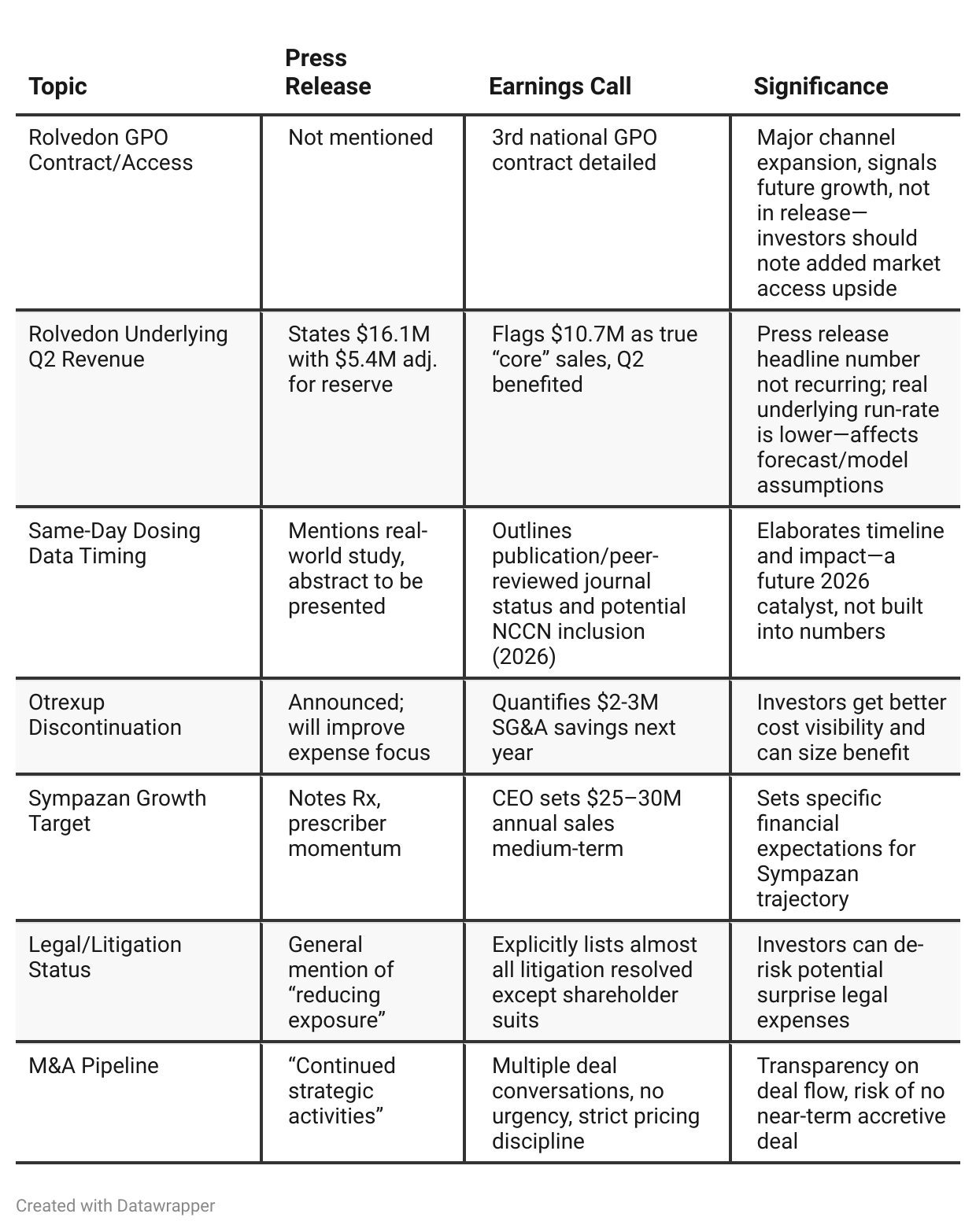

Press Release vs Call Transcript Comparison

Earnings Call Offers More Forward-Looking Granularity: Especially on new commercial access for core products and timing of future data catalysts.

Reserve Release Distorts Near-Term Sales Growth: Models based solely on press release headline sales may overstate organic growth; investors need to normalize for one-off reserve benefit.

Management Tone: The call shows more transparency regarding internal assumptions, M&A caution, and operational changes versus the more confident tone in the release.

Legal Cleanup: The call provides more color and confidence about the lack of major outstanding litigation, a real de-risking factor.

Sensitivity Analysis: The call spells out how guidance is driven by moving parts (pricing, generic competition, strategic actions), while the release is less explicit.

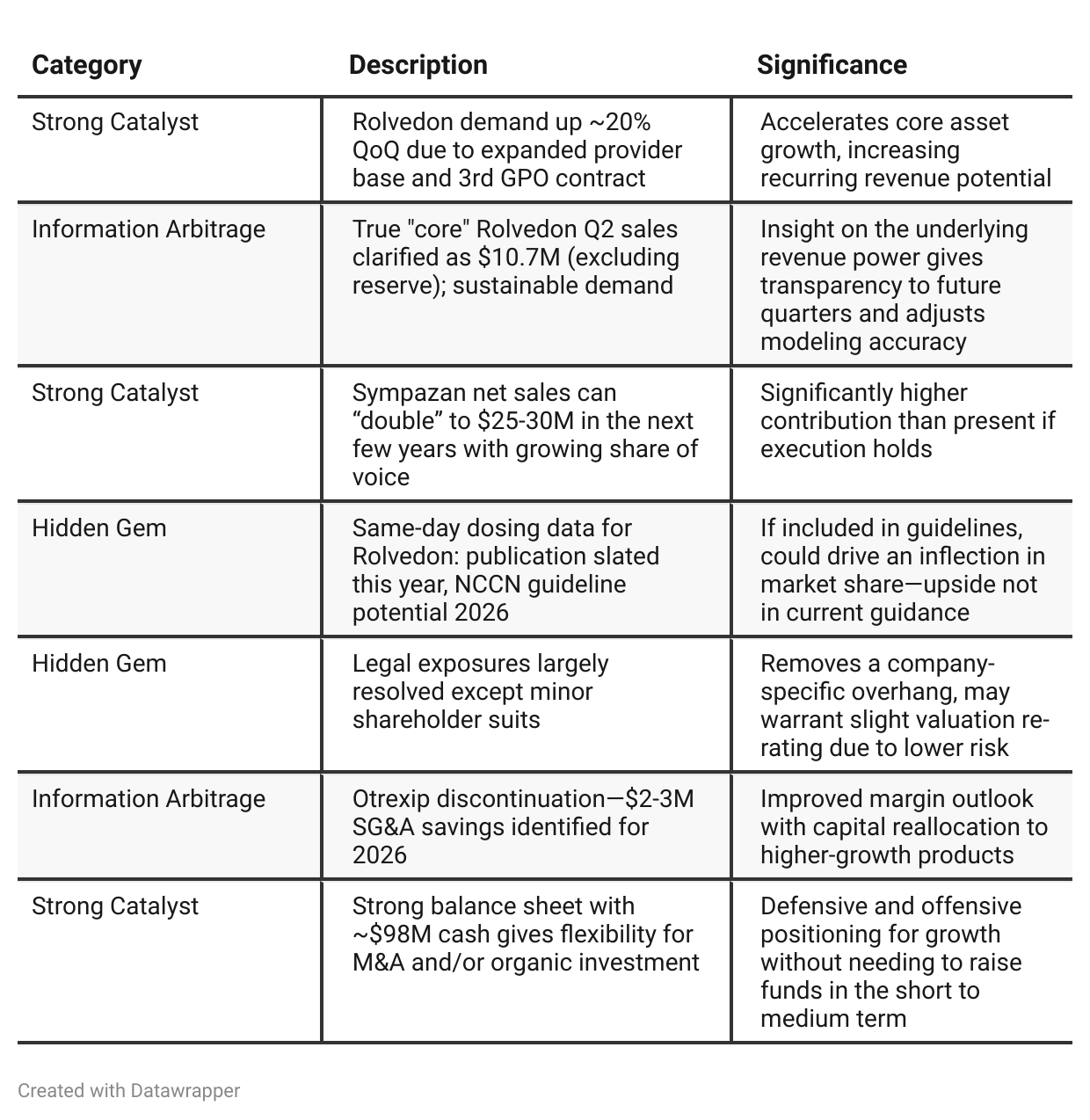

Positive Insights

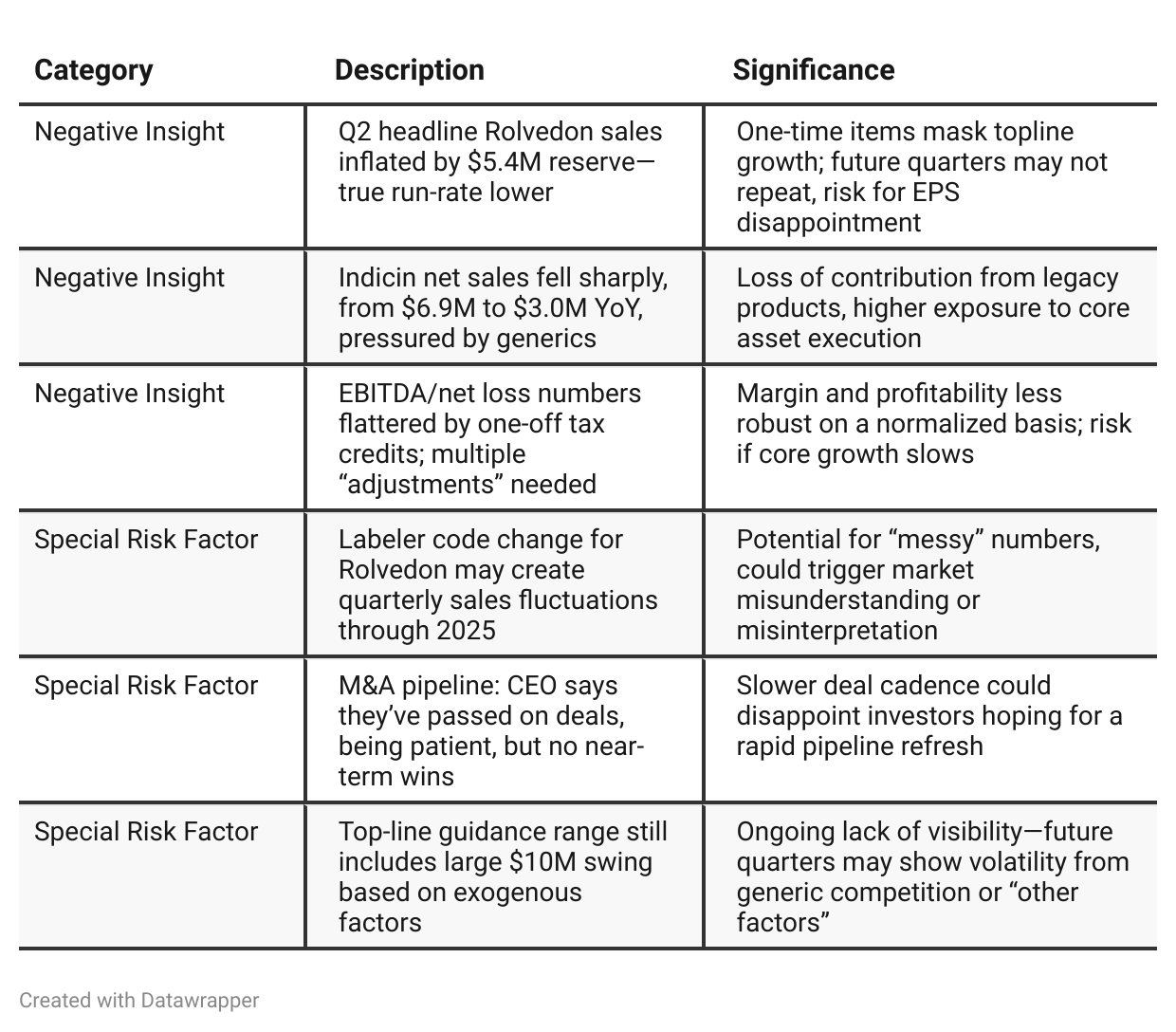

Negative Insights

Tariff Risk

Mentions of tariffs or trade policy:

None found in the transcript.

No discussion of risks or impacts from U.S. tariffs, supply chain shifts, or trade frictions on revenue, supply chain, or profitability.

No commentary on market share or innovation risks due to external trade policy.

Action: Investors should monitor future calls and communications for any developments given the political environment and existing forward-looking statement boilerplate regarding U.S. trade policy more broadly.

Previous Earnings Call

Quarter-over-quarter comparison

Q1 2025 Narrative: Assertio’s narrative was focused on turning the corner—having completed a “stabilization” year, the team was hard at work in the “transformation” phase, determined to resolve legal overhangs, refocus on core growth drivers, and prep for future M&A. The messaging balanced confidence with caution, frequently referencing legal risk, pricing pressure, and the need for “execution,” while reassuring that all action is on track for the long-term plan.Q2 2025 Narrative: Assertio’s story in Q2 matures. Management is now asserting tangible progress: cost-cutting actions (e.g., Otrexip), concrete new access wins (GPO contract), and a meaningfully stronger balance sheet. There is greater candor around revenue quality (ex-reserve adjustments) and a more upbeat tone about demand trends in core assets. Risks and legacy drag from non-core/generic-prone assets are still present, but the company now emphasizes its “inflection point” and readiness for “growth phase” as transformation priorities are completed. While commercial execution and pipeline expansion are still works in progress, the company now feels, and wants investors to feel, it’s on firmer ground—leaner, more focused, and strategically positioned.

Year-over-year comparison

Q2 2024: Assertio, with a new CEO, was turning the page on a difficult year (generic Indicin, integrating Spectrum/Rolvidon). Optimism centered on strong assets (especially Rolvidon), the company’s ability to execute, and leveraging its platform and balance sheet for smart, accretive growth.

Q2 2025: One year later, Assertio describes itself as at an inflection point. The transformation is largely done: non-core distractions divested, costs cut, legal headwinds cleared. The company is more disciplined, more focused, and executing on tangible growth (not just talking about it). Growth is now being driven by targeted resource allocation, concrete market access wins, and operational discipline—setting the stage, in management’s words, for the coming “growth phase.”

Final Takeaway

Assertio Holdings is in a transformation phase focused on streamlining costs, commercializing specialty assets, and clearing legacy risks. While core assets are growing and major legal overhangs are resolved, underlying normalized growth is less robust after excluding one-timers. Execution on product expansion (including commercial access, publication catalysts, and M&A) will determine future upside. Verdict: Hold, as the company needs to prove true acceleration and margin expansion without further one-off support.