American Shared Hospital Services (NYSE: AMS) – Q2 2025 Earnings

American Shared Hospital Services (NYSE: AMS) – Q2 2025 Earnings

Earnings Release Date: Aug. 13, 2025

Stock Price: $2.57

Market Cap: $16.9 million

Q2 2025 sales of $7.1 million vs $7.1 million in the prior year

Q2 2025 EPS of $0.04 vs $0.55 in the prior year

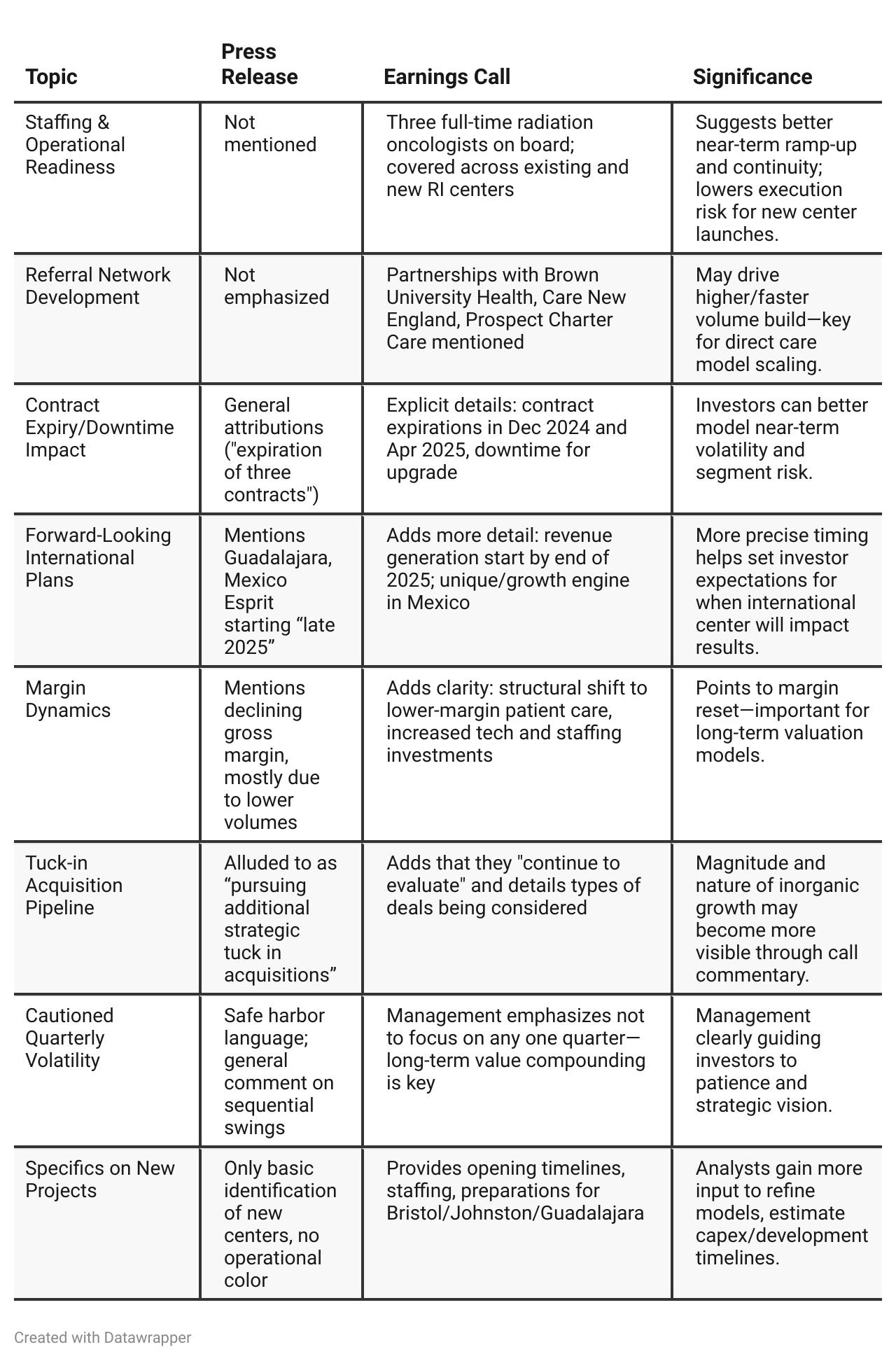

Press Release vs Call Transcript Comparison

Balance Sheet Stability: Cash/working capital levels unchanged, which is positive amid expansion, but a rising current liability balance could become a concern if not watched closely.

Evolving Business Model: Continued transition from high-margin, contract-based equipment leasing to lower-margin, but higher-growth integrated direct patient care; reflects broader industry trends towards vertical integration.

Profitability Headwinds: Short-term pressure from transition, new center ramp, and cost inflation; longer-term gross margin recovery hinges on scaling up patient volumes.

Long-Term Orientation: Both documents reflect a narrative aimed at attracting patient, growth-oriented investors as opposed to those seeking immediate bottom-line improvement.

Explicit Guidance on Use of Adjusted EBITDA: Reliance on this non-GAAP metric to emphasize operational momentum while explaining away non-cash/one-off impacts.

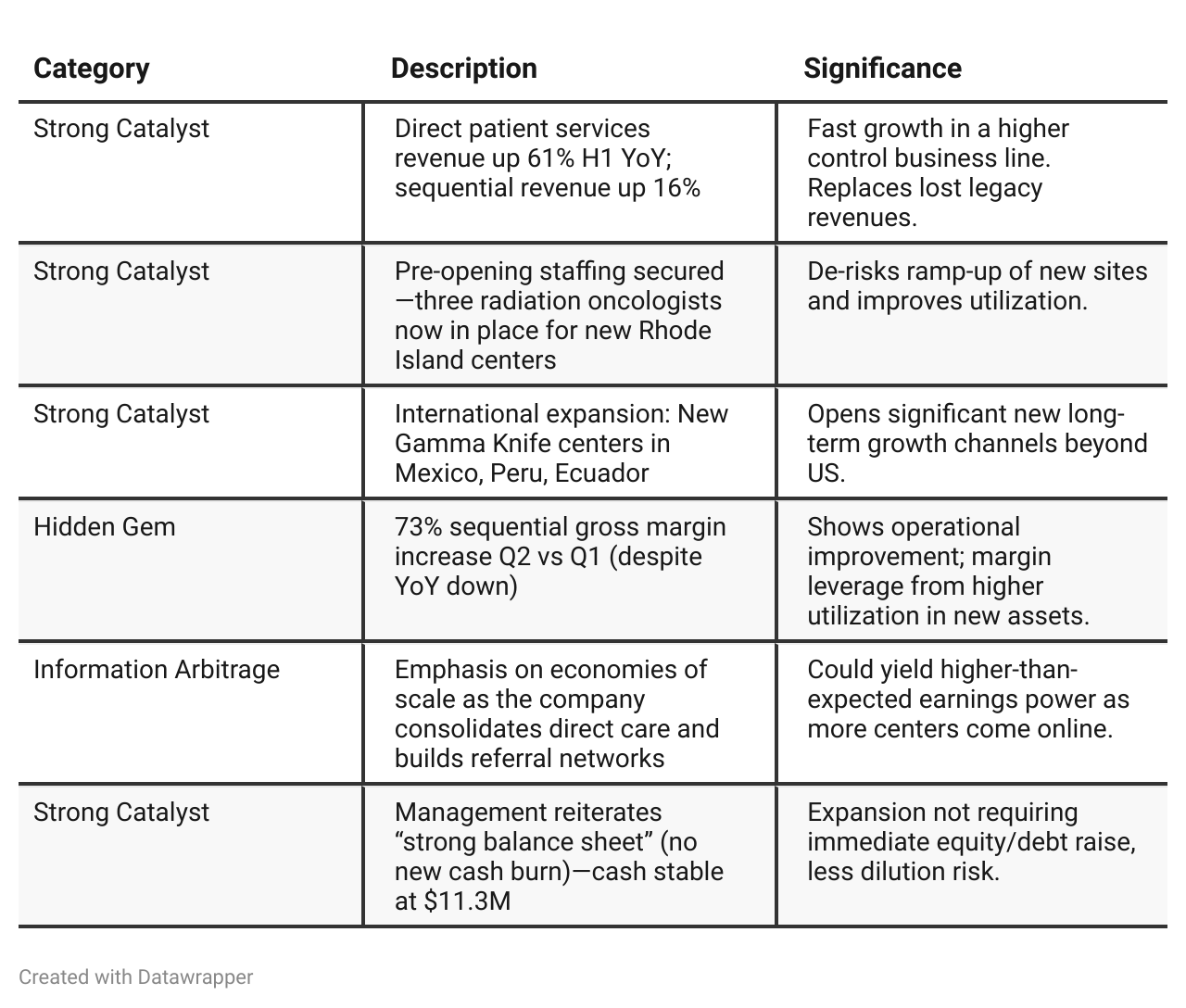

Positive Insights

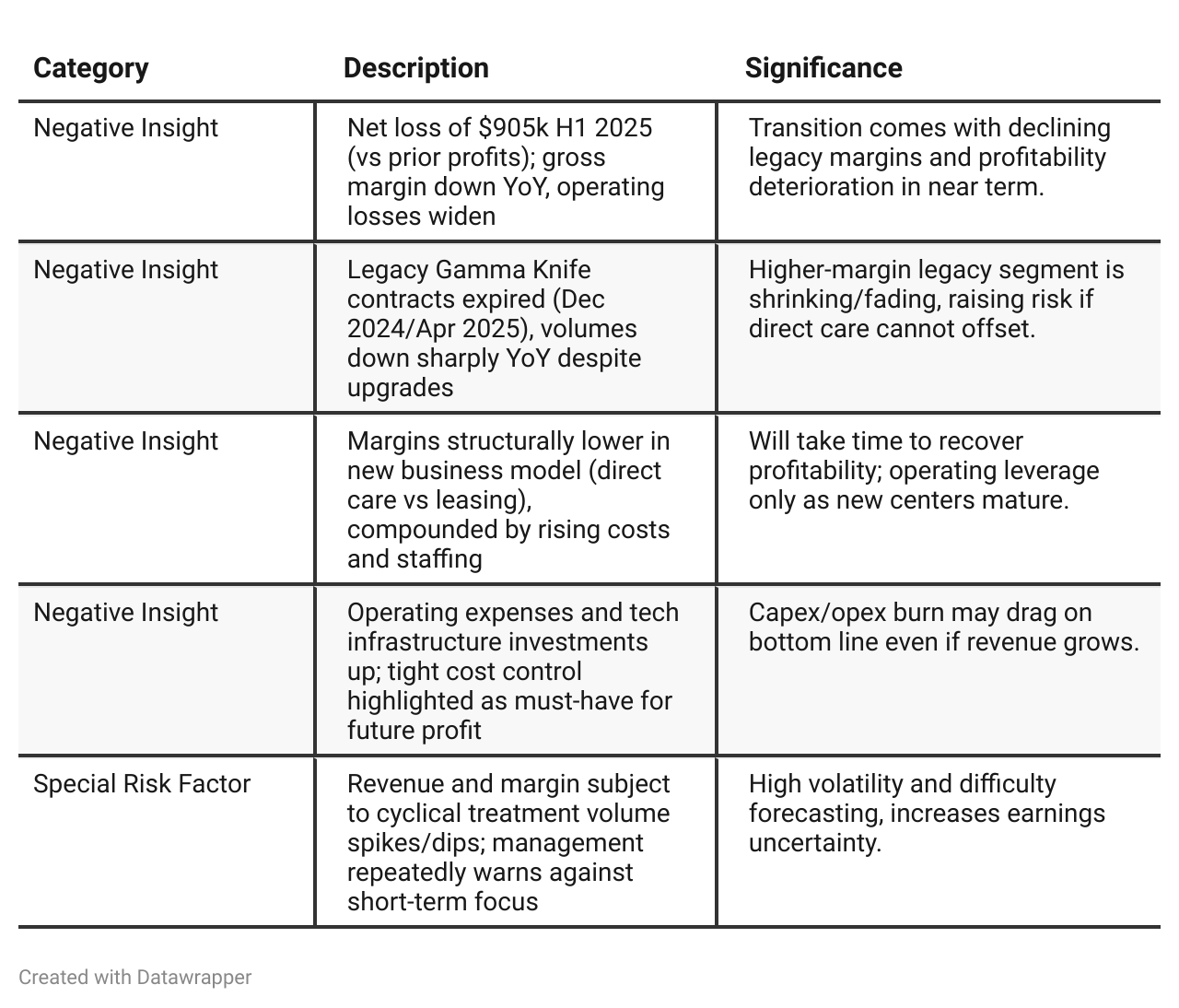

Negative Insights

Tariff Risk

No mention in the transcript of U.S. tariffs or trade policy impacts. No statements found regarding tariffs, supply chain shifts, pricing related to international trade, or mitigation measures. Focus is entirely on domestic/international operations, growth, and health system partnerships rather than import/export or supply chain vulnerabilities. Tariffs do not appear to be a direct risk factor for AMS’s current quarter or forward strategy.

Previous Earnings Call

Quarter-over-quarter comparison

Q1 2025: AMS was in an early stage of strategic transition, dealing with short-term headwinds from legacy segment declines and new segment integration, especially around staffing and fixed cost absorption. Management repeatedly asked investors to look past near-term volatility and focus on longer-term transformation. International opportunities, although on the horizon, were still emerging.Q2 2025: The company’s transition advanced materially. They hit full staffing at new key centers, started seeing volume gains and utilization improvements, and began realizing operational benefits from past investments. Messaging is more confident and focused on delivering results, not just setting expectations. Growth from new segments is compensating for legacy weaknesses more effectively, and the narrative has shifted from preparing for growth to actively capturing it.

Year-over-year comparison

In Q2 2024, AMS was at an inflection point—recovering from management turnover and integrating transformative acquisitions, with high optimism about the future pipeline but a strong need for patient investment and execution management. Risks around new market entries, regulatory permissions, and ramp-up timelines were front and center, with management urging patience and touting the strength of its team and backlog.

By Q2 2025, AMS’s narrative has advanced to one of operational proof: the company is fully staffed at new centers, delivering sequential revenue and volume growth, realizing some economies of scale, and beginning to offset legacy segment shrinkage with faster-growing direct patient services. The tone is more self-assured, with less emphasis on future promise and more on recent delivery. Now, the company’s story is clearly about capitalizing on prior investments—driving utilization, managing margin pressure, and scaling new revenue streams while maintaining a long-term, value-building focus.

Final Takeaway

American Shared Hospital Services (AMS) is in a late-stage transition, scaling up its direct patient care model amid the decline of legacy leasing revenue. While robust growth in new centers, especially with staffing and international expansion, provides a strong long-term narrative, current profitability and margin trends are pressured by contract attrition and inherently lower direct care margins. Execution on referral growth, ramp-up, and cost containment will be pivotal for margin recovery. Verdict: Hold. Upside exists but hinges on demonstrating operating leverage as new sites mature and legacy headwinds abate.