Altimmune, Inc. (NASDAQ: ALT) – Q2 2025 Earnings

Altimmune, Inc. (NASDAQ: ALT) – Q2 2025 Earnings

Earnings Release Date: Aug. 12, 2025

Stock Price: $3.38

Market Cap: $275.3 million

Q2 2025 sales of $0.01 million vs $0.01 million in the prior year

Q2 2025 EPS of $-0.27 vs $-0.35 in the prior year

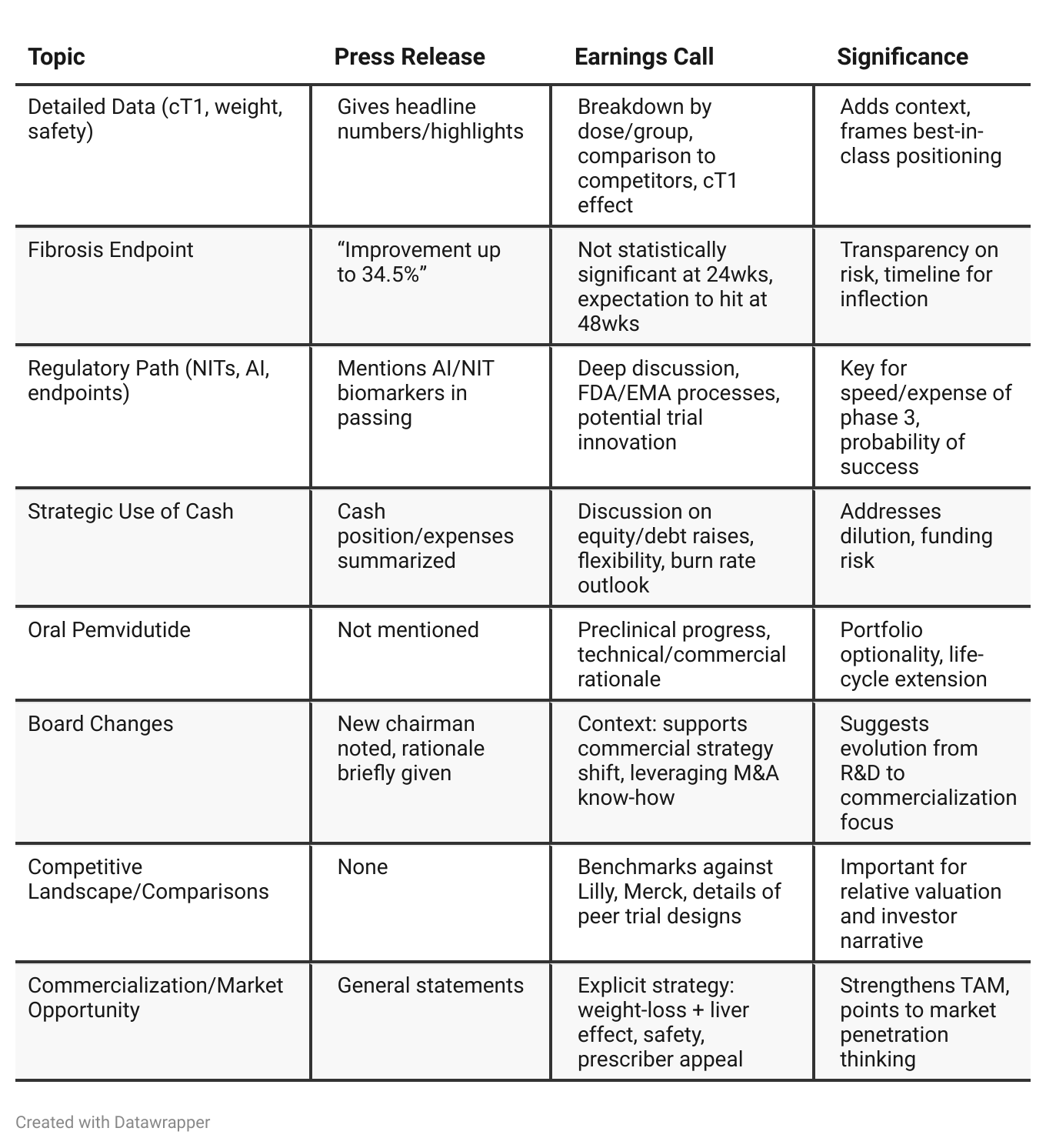

Press Release vs Call Transcript Comparison

Earnings Call surfaces more “strategic depth”: Plans for leveraging noninvasive endpoints and artificial intelligence may lead to a faster, less costly phase 3, but this isn’t guaranteed.

The press release is “cleaner” but omits competitive and regulatory context, focusing mainly on positives.

Risks are more downplayed in the release; the call gives the real issues (uncertain FDA stance on NITs, fibrosis endpoint shortfall).

Financial flexibility is stronger than it first appears: The company is proactive about capital raises and mitigating dilution.

CEO and CMO confidence in Q&A is crucial: They offer a logical case for why endpoints will likely be hit in longer studies—this could inform investor willingness to “buy the dip” if intermediate news is mixed.

Real-time market sensitivity: The earnings call format responds directly to analyst concerns, which can be crucial for sentiment and potential rerating or derating moments.

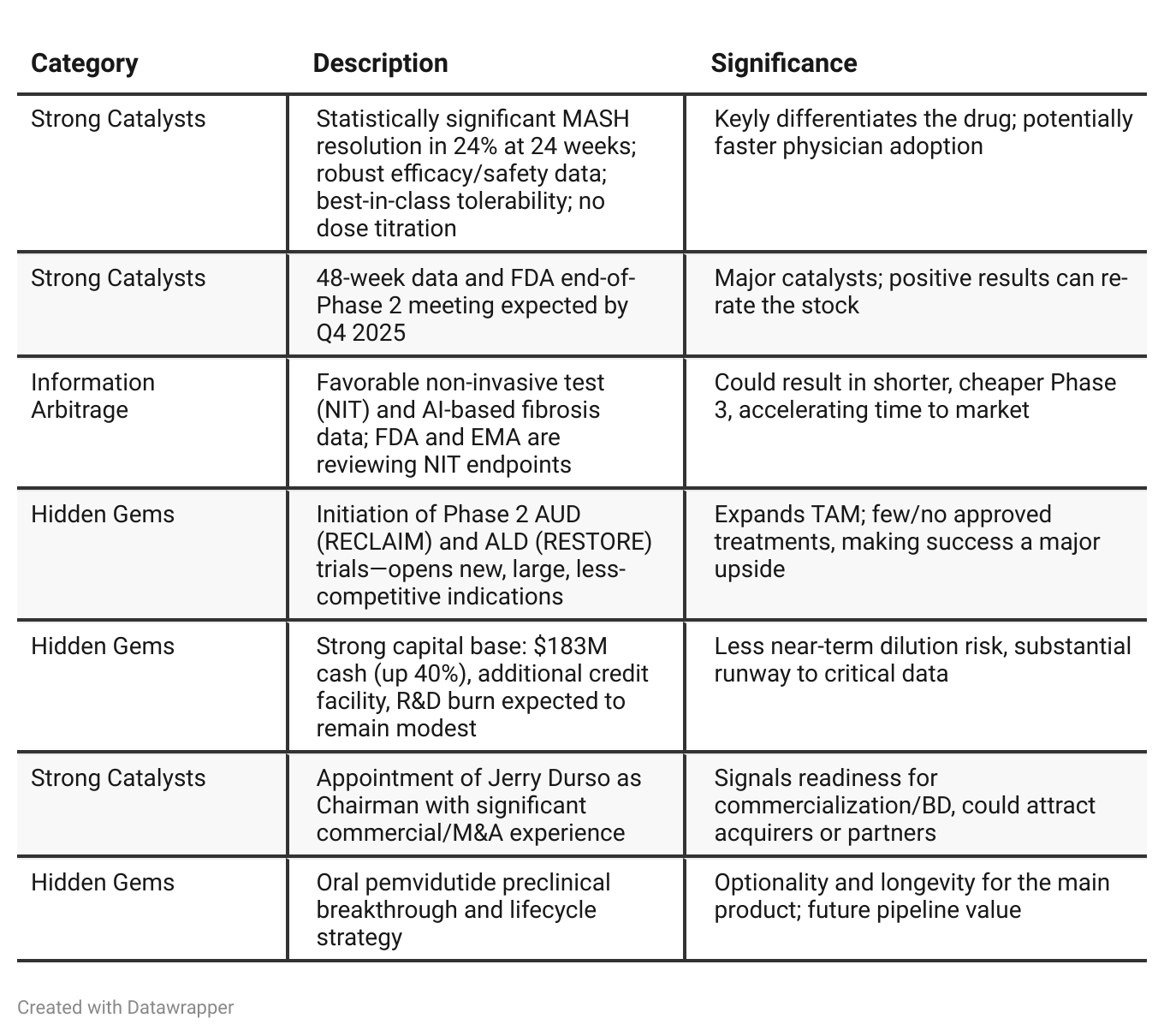

Positive Insights

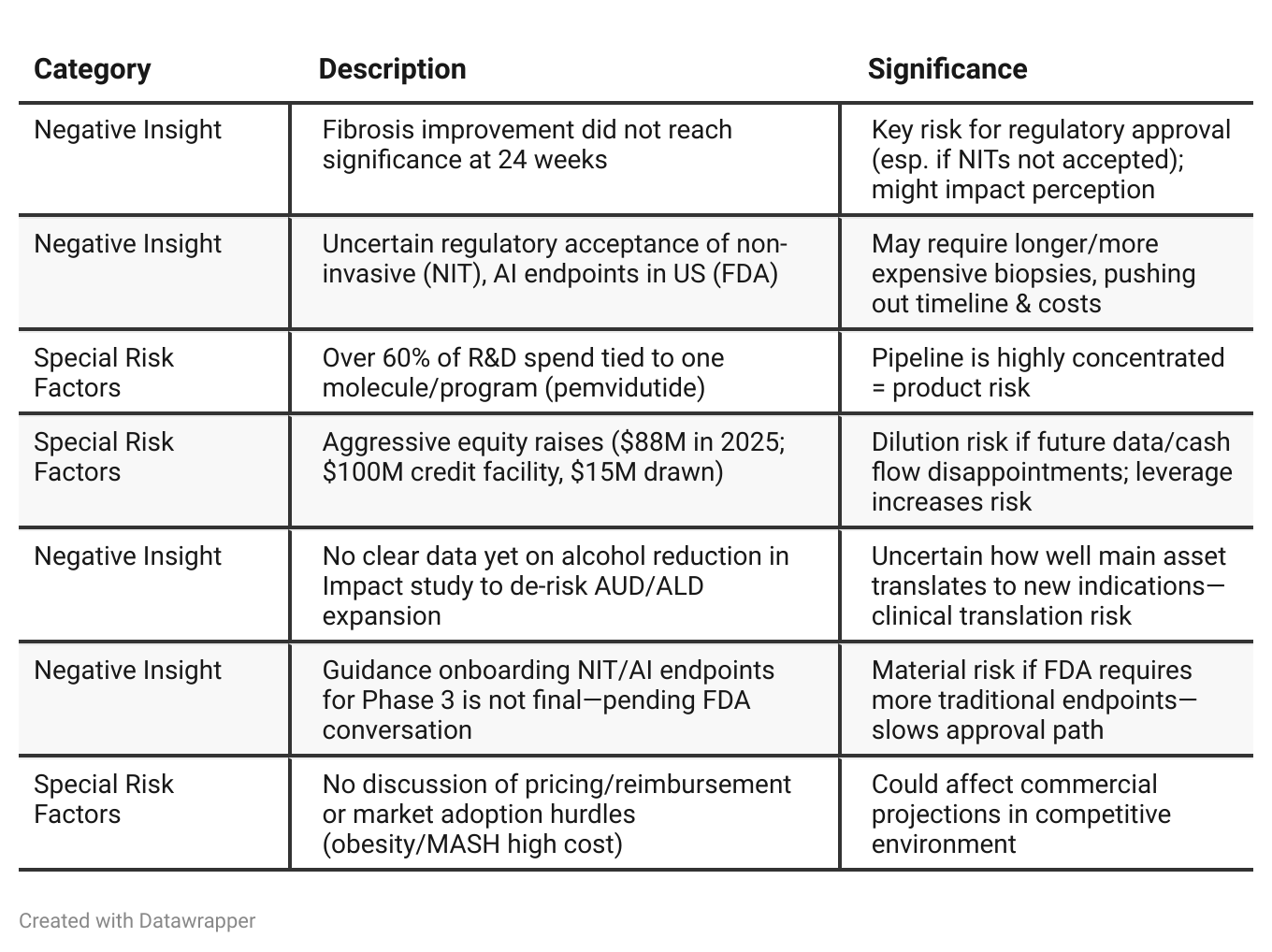

Negative Insights

Tariff Risk

Tariffs/trade policy were NOT mentioned in any context in the transcript provided.

No indication of current, previous, or anticipated tariff impact on supply chain, cost structure, or earnings.

No noted mitigation strategies for tariffs or international trade friction.

No analyst questions or management commentary on relative cost, global sourcing, or competitive advantage related to tariffs.

Conclusion: Tariff risk is immaterial to Altimmune’s investment thesis based on this call’s content.

Previous Earnings Call

Quarter-over-quarter comparison

In Q1 2025, Altimmune was a company on the verge of a potentially transformative clinical data readout, focused on risk management, differentiation, and setting up future growth avenues with new trial launches and enhanced financial flexibility. The tone was one of disciplined optimism, heavy with anticipation and ‘what if’ promises.By Q2 2025, Altimmune’s narrative has shifted to one of real-world validation. The company has delivered statistically significant topline data in its core MASH program, is actively shaping FDA and Phase 3 engagement, and is positioning itself as a science-driven, pragmatic player ready for commercialization—with added credibility via new board leadership and executed clinical progress in adjacent indications (AUD/ALD). The messaging is now more qualified, focusing on navigating regulatory complexities, leveraging financial strength for ‘next steps,’ addressing nuanced trial results (such as missing the fibrosis endpoint but excelling elsewhere), and pushing a “best in class” story supported by comparative data. The company appears more mature, with sights set on meaningful partnership, commercialization, and additional value inflection in the near term.

Year-over-year comparison

Q2 2024: Altimmune told a story of scientific momentum and opportunity—a company positioned on the cusp of major clinical news, actively seeking the right strategic partner, and deeply focused on differentiation in a crowded landscape. The tone combined ambition with caution, highlighting potential across several indications but still very much awaiting proof.

Q2 2025: One year later, Altimmune’s narrative is transformed by data and corporate maturation. With pivotal trial readouts showing statistical significance on key endpoints, management speaks from a position of validation—though still navigating scientific and regulatory complexities where results were mixed. The organization is structurally evolving for commercial readiness, moving forward in parallel on multiple indications, and benchmarking itself confidently against other industry leaders. The conversation is more about execution, regulatory alignment, and maximizing realized value from their clinically validated platform than about potential.

Final Takeaway

Altimmune (NASDAQ: ALT) is in an advanced clinical development/growth phase, pushing a differentiated asset (pemvidutide) with best-in-class MASH/weight loss data, expanding into adjacent large unmet needs (AUD/ALD). While positive catalysts (Q4 data, FDA meeting, commercial Board leadership) are visible, there remain key regulatory and clinical readout risks. Execution on FDA endpoint alignment and data at 48 weeks will determine the next major move in the stock. Verdict: Hold with speculative upside—potential re-rating on clear Phase 3 pathway and durable 48-week efficacy/safety.