Alarum Technologies Ltd. (NASDAQ: ALAR) – Q2 2025 Earnings

Alarum Technologies Ltd. (NASDAQ: ALAR) – Q2 2025 Earnings

Earnings Release Date: Aug. 28, 2025

Stock Price: $16.46

Market Cap: $114.4 million

Q2 2025 sales of $8.8 million vs $8.9 million in the prior year

Q2 2025 EPS of $0.17 vs $0.41 in the prior year

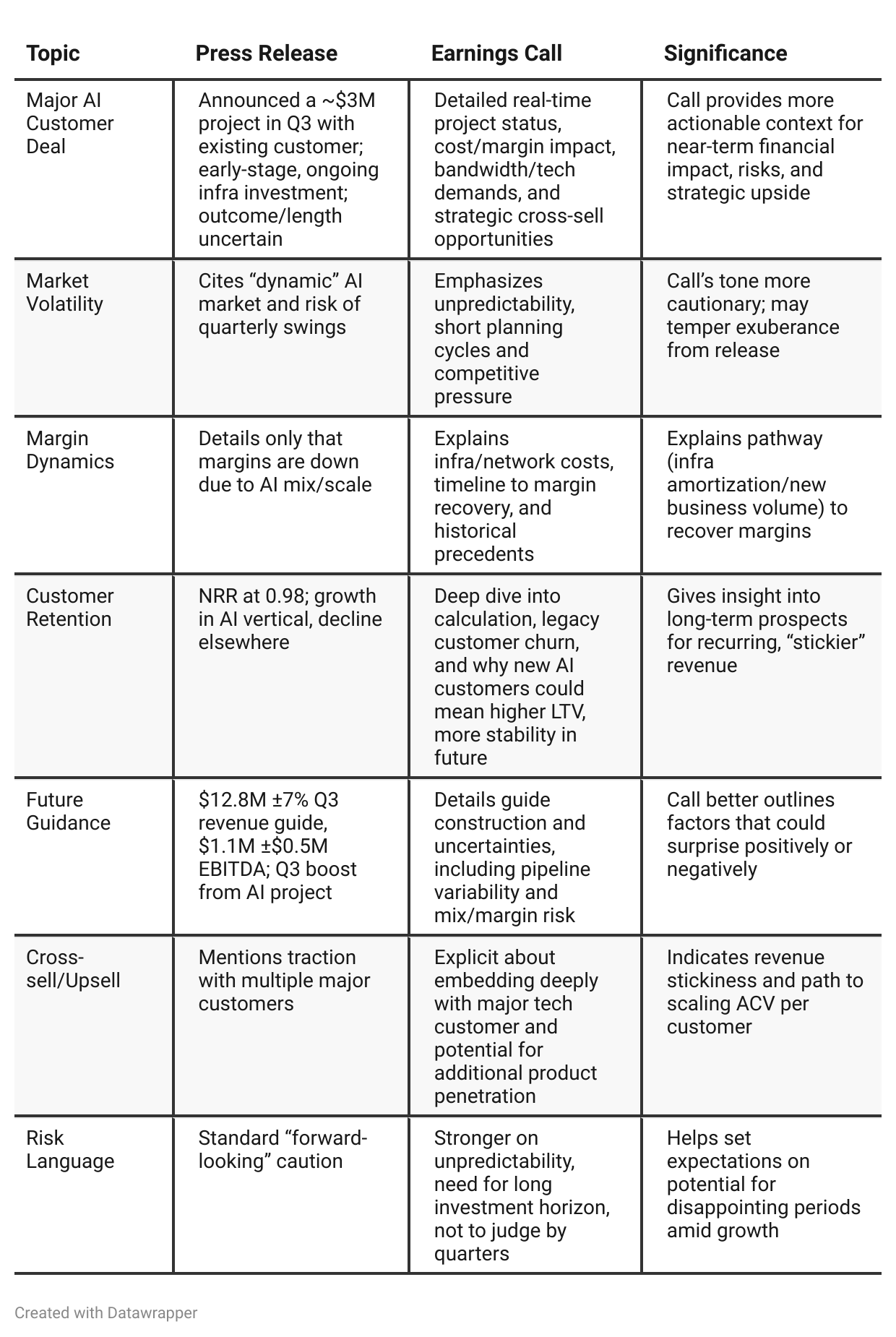

Press Release vs Call Transcript Comparison

Call Risk Disclosure More Direct: While the press release is upbeat and future-focused, the earnings call repeatedly cautions about volatility and near-term margin/headcount headwinds. This sets more realistic expectations that are important for investors, especially those focused on near-term results.

Depth on Cost Structure: The call provides color on why infra investment (network, servers) spikes with AI projects—insight perhaps missed by a surface reading of the press release and margin numbers.

Customer Concentration Risk Acknowledged in Call: Press release highlights new major customers, but call clarifies management is focused on growing total pipeline and diversity, not just chasing whales.

Improved Financial Health: Both documents confirm strong cash/equity balances, which boost the company’s ability to invest through volatility.

Shareholder Composition/Equity Ratios: The press release gives more underlying balance sheet detail for context.

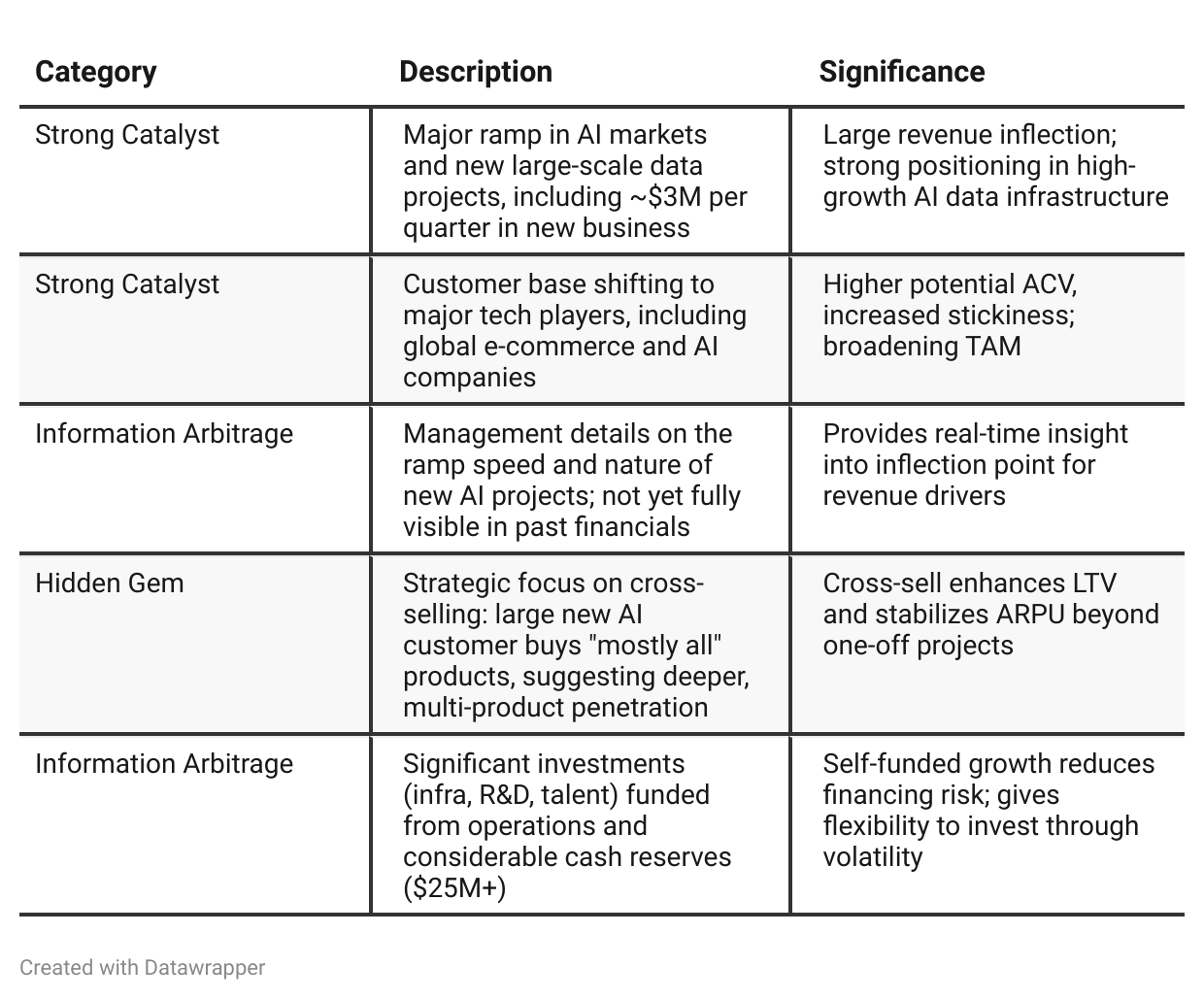

Positive Insights

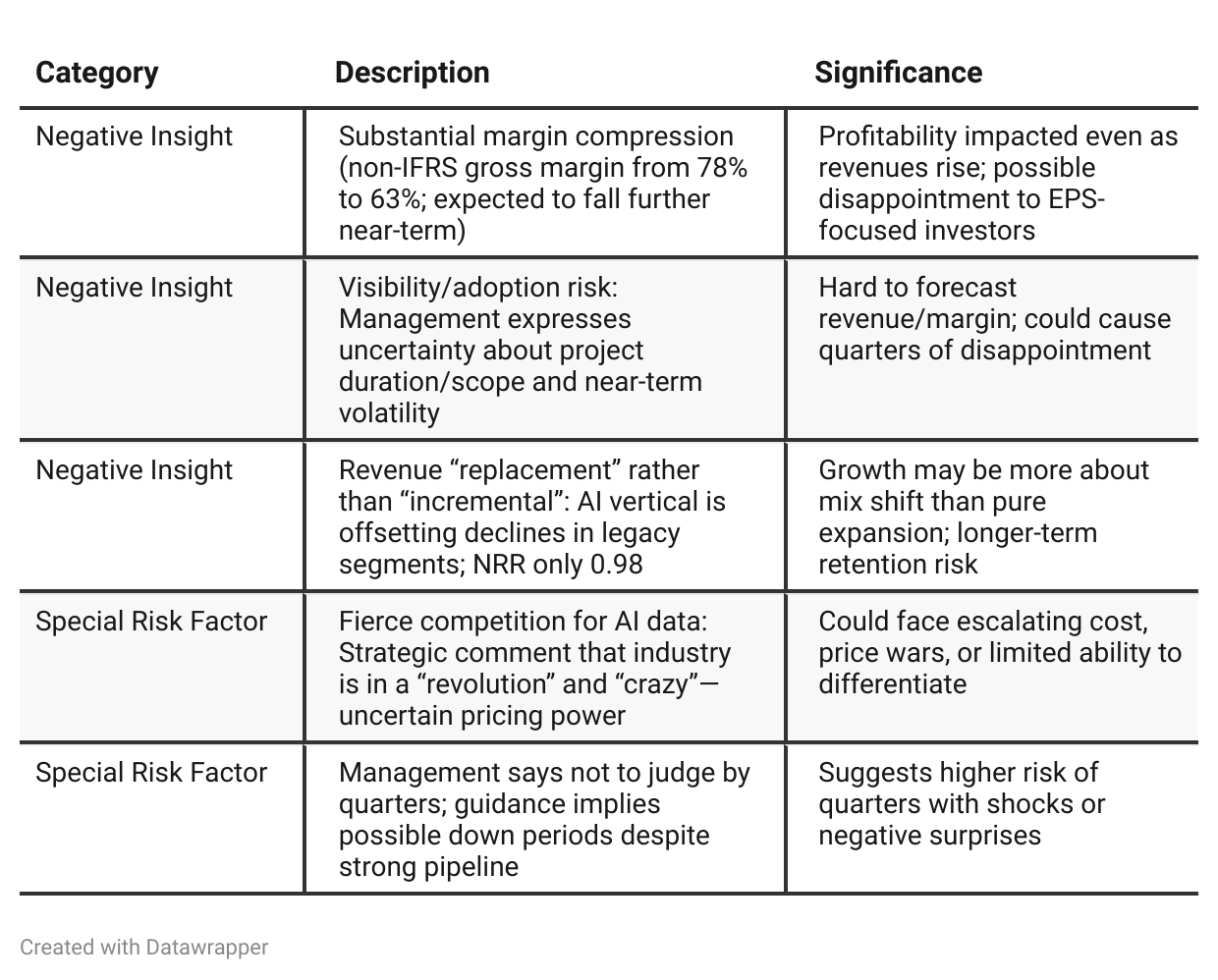

Negative Insights

Tariff Risk

Explicit Mentions: None found in transcript.

Implied Exposure:

No discussion of U.S. tariffs, supply chain rerouting, or trade frictions. The business is cloud/software-centric, focused on data, not physical goods.

No mention of cross-border cost pressures or customer migration related to tariff policy.

Conclusion: Tariff risk appears to be immaterial for Alarum based on this call; the business model revolves around digital data infrastructure and software, with no signals of hardware dependency or global sourcing issues requiring tariff mitigation.

Previous Earnings Call

Quarter-over-quarter comparison

Alarum Technologies began 2025 rallying around the AI data revolution, energetically investing to ensure it could meet a surging, broad-based customer demand—particularly from ambitious global tech and AI players. As the year progressed, this strategy led to concrete wins and a major breakthrough: a large-scale AI project with a flagship customer, driving a quantum leap in short-term revenue but adding significant new volatility and margin pressure. In response, management’s tone became more seasoned and transparent—they now urge patience, pressing investors to judge their journey over many quarters, as Alarum embraces both the upside and risks of being at the epicenter of an unpredictable, but extraordinary, AI infrastructure market. The focus is no longer just on readiness and capacity, but on navigating scale, customer volatility, and margin trade-offs to ultimately become a central, indispensable provider in the AI age.Year-over-year comparison

Q2 2024: Alarum Technologies was riding a wave of successful transformation, shifting to focus on enterprise data collection and AI enablement. The messaging was one of high confidence—record margins, strong cash flow, major customer logos, and scalable profit growth. The company was selling the story of having built a robust, profitable, and innovative platform ready for rapid industry growth.

Q2 2025: The narrative matures. Alarum is now deeply embedded with the AI sector’s most demanding customers, growing revenues fast but deliberately sacrificing margins and near-term profit to aggressively build out infrastructure and talent. Management makes it clear they’ve traded quarterly earnings stability for future positioning as a mission-critical player in the AI data supply chain. There’s greater humility—celebrating wins, but cautioning about volatility, customer unpredictability, project-based lumpiness, and margin pressure. Investors are asked to trust in the compounding value of platform scale and long-term strategy, as the business “bets big” on data as the fuel for the AI revolution.

Final Takeaway

Alarum Technologies is in a high-growth, market-pivot phase, aggressively targeting the surging demand for large-scale AI data collection. While new, large AI customers are driving revenue and positioning Alarum as a key infrastructure provider, near-term profitability is hampered by infrastructure investments and heavy margin compression. Execution on ramping new customers to higher-margin business and diversifying the customer base will be critical for future performance. Verdict: Hold—with meaningful upside if margin/visibility improves, but considerable downside if volatility translates into negative earnings surprises.