Atlas Engineered Products Ltd. (TSXV: AEP) (OTC: APEUF) – Q2 2025 Earnings

Atlas Engineered Products Ltd. (TSXV: AEP) (OTC: APEUF) – Q2 2025 Earnings

Earnings Release Date: Aug. 29, 2025 (all figures in Canadian dollars)

Stock Price: $0.79

Market Cap: $55.7 million

Q2 2025 sales of $13.7 million vs $15.1 million in the prior year

Q2 2025 loss per share of ($0.01) vs EPS of $0.01 in the prior year

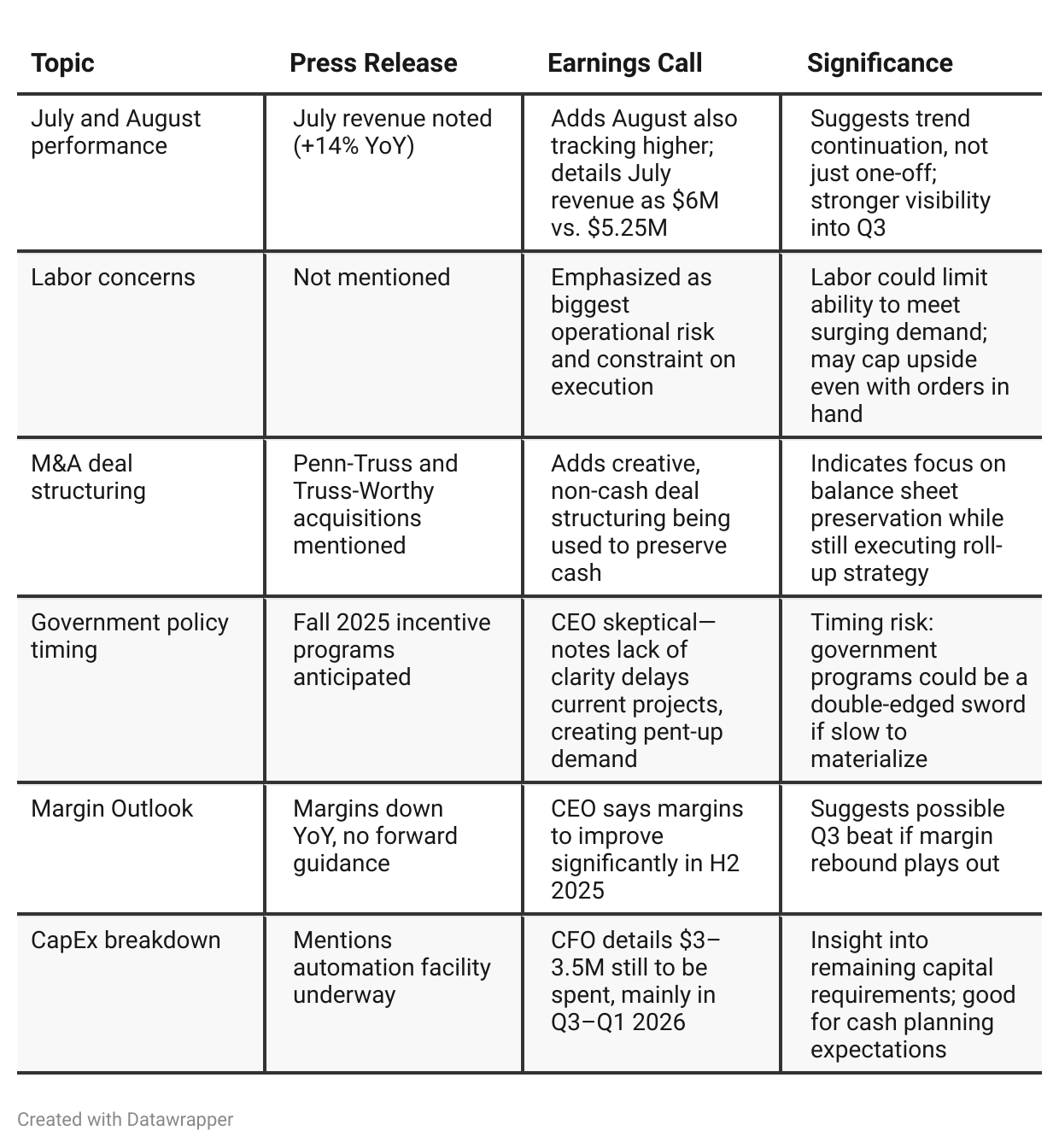

Press Release vs Call Transcript Comparison

The press release delivers the standard financial overview and optimism on quoting activity, acquisitions, and strategic positioning, but the earnings call reveals deeper nuances critical for investors. Notably, the call surfaces concerns about labor availability, delayed revenue recognition due to builder hold-ups, and reliance on as-yet-unconfirmed government support.

These risks are not visible in the press release but materially affect near-term execution and margin recovery. For investors, the call adds important clarity around timing, liquidity discipline, and operational pressures—elements that should weigh heavily in assessing whether APEUF can capitalize on its backlog and quoting pipeline.

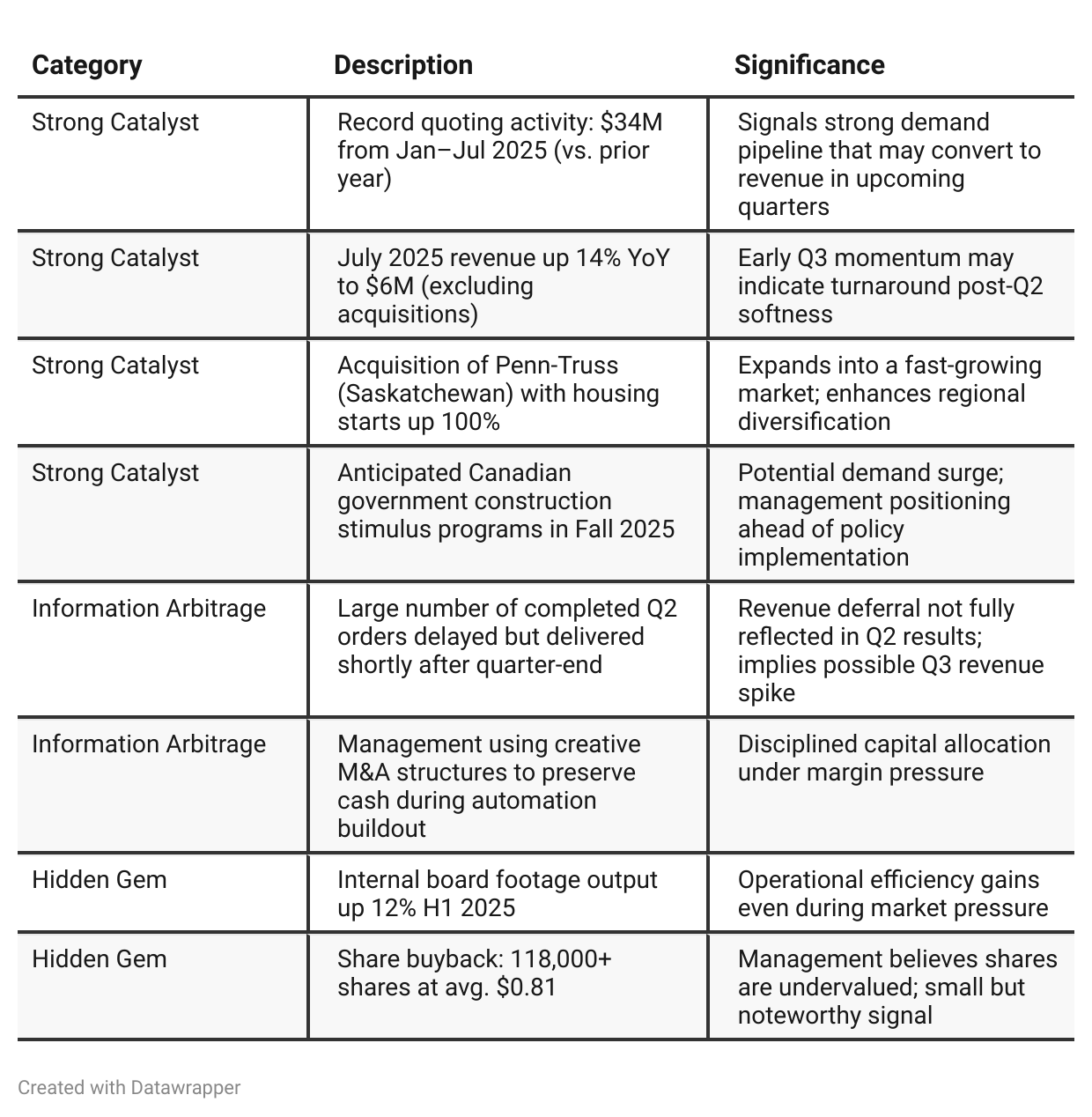

Positive Insights

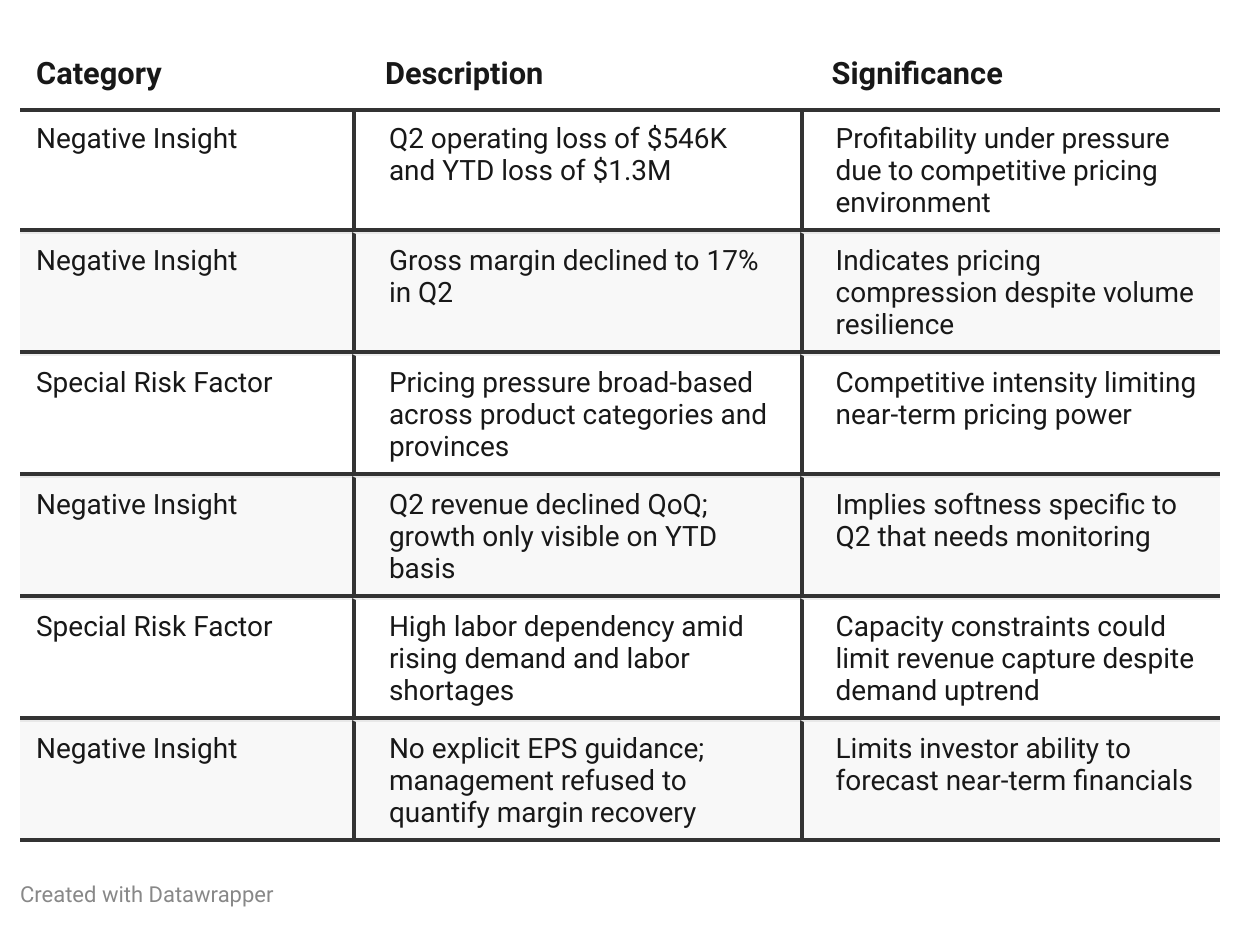

Negative Insights

Tariff Risk

Transcript Mentions: Company acknowledges trade uncertainties between Canada and the U.S. but notes its low exposure to U.S. cross-border transactions and USMCA-covered products mitigates direct tariff impact.

Impacts: Broader trade instability is cited as a reason for Q2 project delays and competitive pricing, which affected margin and revenue timing.

Mitigation Strategy: Geographic diversification through M&A and automation investments appears to be a hedge against regional volatility and external trade pressures.

Forward-Looking: No direct discussion on future tariff changes, but management notes trade policy uncertainty as a macro factor they are tracking.

Conclusion: Tariff impact is indirect and more macro-driven than company-specific; minimal current financial exposure, but remains a watchpoint if U.S.-Canada tensions escalate.

Previous Earnings Call

Quarter-over-quarter comparison

Between Q1 and Q2 2025, AEP's narrative evolved from upbeat inflection-point optimism to a more realistic and execution-focused message. In Q1, the company leaned into themes of growth, automation, and a strong pipeline, highlighting its strategic position to benefit from a Canadian housing rebound.

By Q2, while topline momentum persisted (record quoting, July revenue growth), management acknowledged margin pressure, project delivery delays, and operating losses, particularly in Ontario and BC.Still, the tone remains confident about market share expansion, new regional opportunities (Saskatchewan), and a margin recovery in H2, especially as expected government support and potential rate cuts come into play. The company is also shifting its capital approach, exploring more creative, non-cash M&A structures while prioritizing liquidity for the Clinton automation rollout.

Year-over-year comparison

From Q2 2024 to Q2 2025, Atlas Engineered Products has shifted from strategic transformation mode to tactical execution and margin defense mode.

In 2024, management painted a bold long-term picture built on automation, real estate, and M&A. In 2025, the focus is on surviving near-term margin pressure and labor constraints while staying committed to its long-term vision.

The strategic pillars (automation, consolidation, housing demand) are still intact, but management now speaks more candidly about near-term cost pressures and execution hurdles. Despite this, quoting volume, geographic expansion (Saskatchewan), and visibility into Q3/Q4 trends suggest AEP is maintaining its forward momentum.

Final Takeaway

Atlas Engineered Products is in a stabilization phase, balancing short-term pricing pressures with long-term growth investments.

While Q2 margins and profitability suffered, the company is positioning itself for a rebound with record quoting activity, regional expansion into high-growth provinces, and automation investments. Upside potential hinges on execution in H2, margin restoration, and the rollout of federal housing stimulus programs.

Verdict: Hold, with potential upside contingent on sustained revenue acceleration and margin recovery by year-end.