Acorn Energy, Inc. (NASDAQ: ACFN) – Q2 2025 Earnings

Acorn Energy, Inc. (NASDAQ: ACFN) – Q2 2025 Earnings

Earnings Release Date: Aug. 7, 2025

Stock Price: $29.62

Market Cap: $73.7 million

Q2 2025 sales of $3.53 million vs $2.275 million in the prior year

Q2 2025 EPS of $0.28 vs $0.11 in the prior year

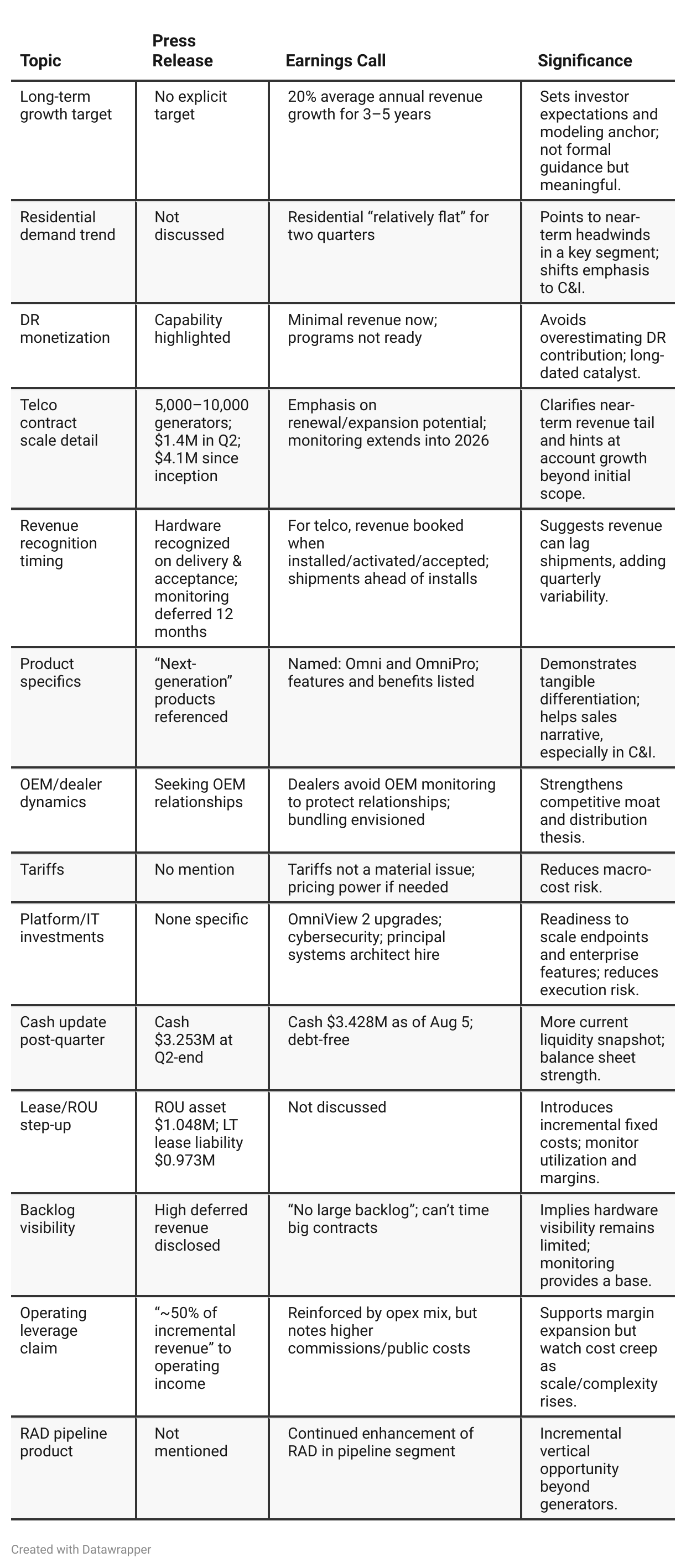

Press Release vs Call Transcript Comparison

Mix and margin: Despite an 89% surge in hardware, gross margin expanded 170 bps to 74.9%, implying healthy hardware margins on the telco rollout and/or scale benefits. As monitoring ramps behind installs, blended margins may remain strong or improve.

Deferred revenue base: ~$3.7M in deferred revenue provides visibility to future monitoring income, partly cushioning hardware timing swings.

Small float/micro-cap dynamics: With ~2.53M diluted shares and a new NASDAQ listing, the stock may be volatile around contract news and quarterly cadence.

Concentration vs. opportunity: The telco contract concentration heightens single-customer risk near-term, but also creates a marquee reference for OEM and C&I pursuits.

Watch items for next quarters: pace of telco installations/activations (monitoring revenue catch-up), any OEM-bundled wins, conversion of non-generator RFPs, residential demand inflection, clarity on lease expansion, and evidence supporting the 20% multi-year growth ambition.

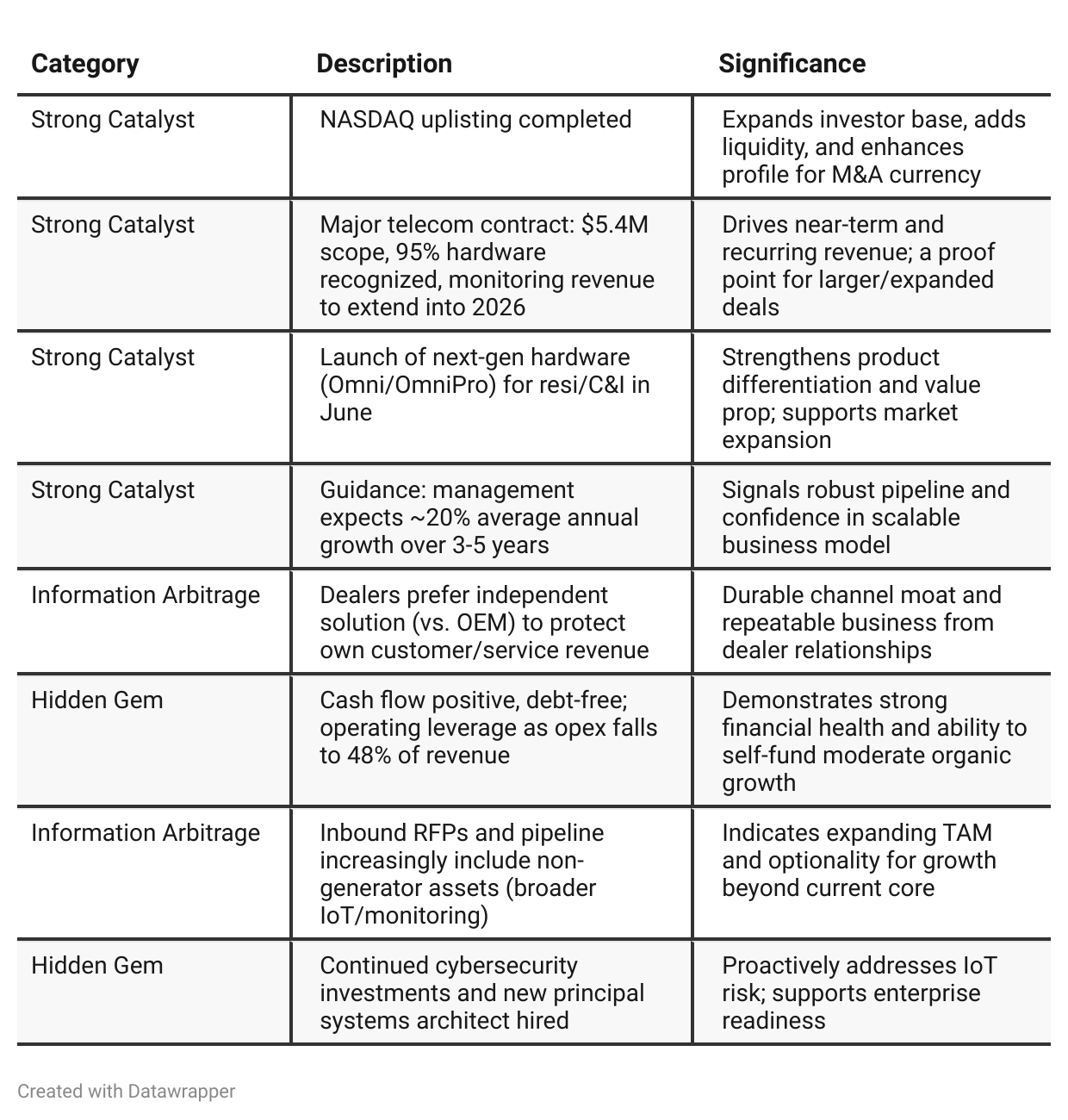

Positive Insights

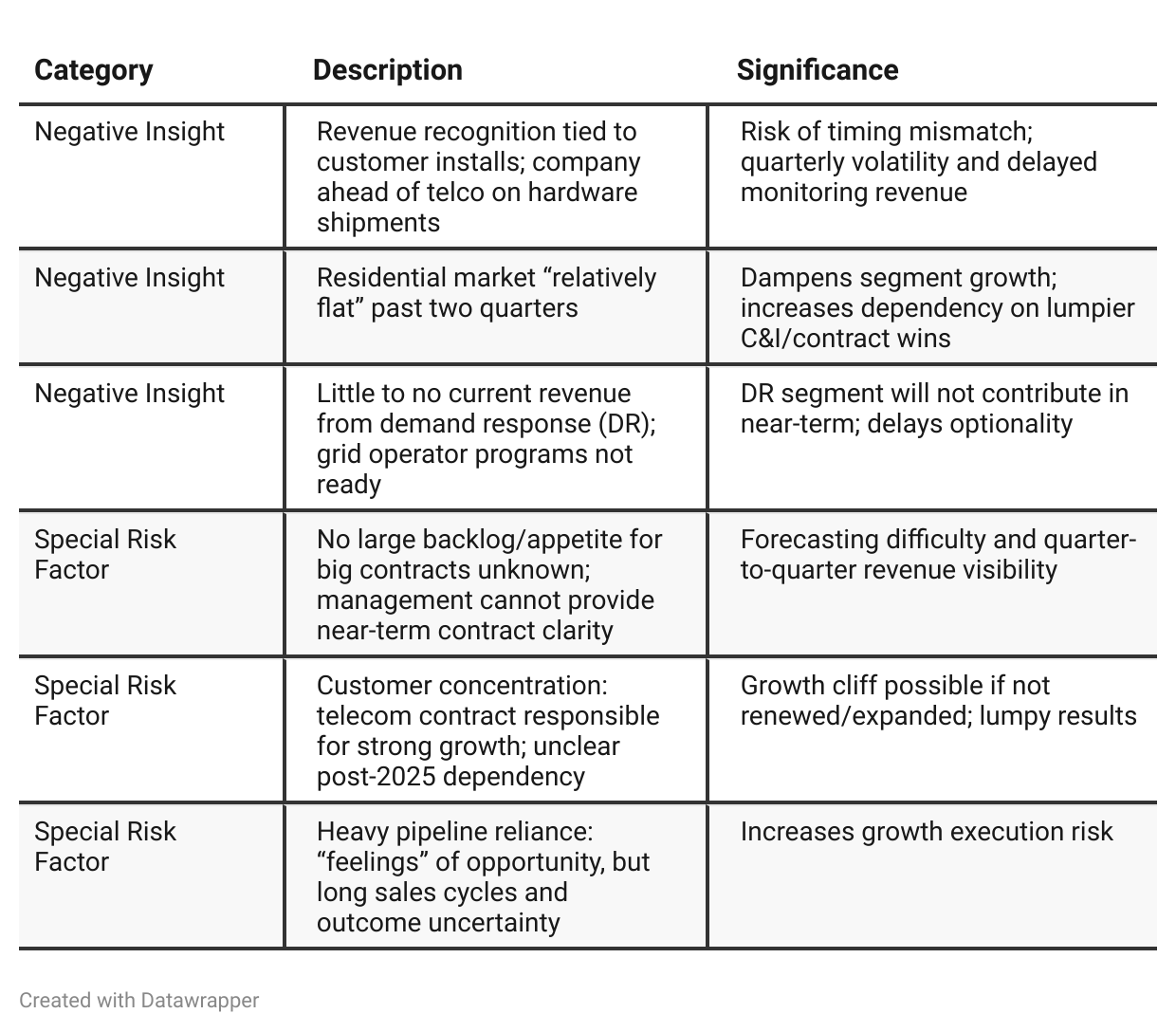

Negative Insights

Tariff Risk

Transcript Mentions: Tariffs are not a significant impact as only a small fraction of components are imported; U.S. assembly.

Mitigation Actions: Monitoring situation; company believes it can flex pricing if cost pressures arise, maintaining historical margins.

Market/Competitive Advantage Observation: No mention that tariffs materially help/hinder market share or innovation.

Forward Statements: Little/no guidance on future impact except confidence in pricing power and margin maintenance.

Summary: Tariffs pose low current risk to Acorn’s costs or execution. The company’s domestic supply chain and flexibility provide insulation.

Sentiment Analysis

The overall sentiment toward Acorn Energy, Inc. ($ACFN) is bullish. Investors highlight strong reasons for optimism, including large contracts, recurring revenue streams, no insider selling after a major stock move, and the company’s potential as an acquisition target. Multiple users mention increasing their stakes and express long-term confidence, with expectations of significant price appreciation. While a few concerns are noted about the need for continued order wins and comparables to other stocks, the prevailing tone is positive, focusing on earnings power, transparency, and favorable long-term prospects.

Previous Earnings Call

Quarter-over-quarter comparison

Acorn Energy’s narrative in Q1 2025 was that of a company at an inflection point—demonstrating that its strategy and business model (notably recurring, high-margin monitoring revenue) work, with a large telecom contract validating product-market fit and fueling strong revenue growth. Management was focused on building the foundation: preparing for a NASDAQ uplisting, finalizing next-generation products, and positioning itself for further OEM/DR adoption and industry tailwinds.By Q2 2025, the narrative shifts from planning and proving to executing and scaling. Acorn has now achieved the NASDAQ uplist, successfully launched new monitor products, and delivered record results with best-in-class margins and cash flow, all while being recognized as an industry leader. The pipeline looks larger and more diverse, but the company also openly acknowledges new risks—residential softness, timing of big contract deployments, and the lumpy nature of large deal wins. Acorn’s messaging is more self-assured and open about volatility, with clear confidence in its ability to scale both organically and through potential partnerships or acquisitions.

Year-over-year comparison

In Q2 2024, Acorn Energy’s press release was the story of a company on the cusp—validating its technology and go-to-market strategy through a landmark telecom win, sharpening its focus on recurring revenue, and harnessing macro tailwinds. By Q2 2025, the narrative evolved to one of strong execution and realized growth: Acorn touts delivered results in both top- and bottom-line metrics, emphasizes its ability to scale profitably, and celebrates a successful NASDAQ uplist that positions it for larger ambitions, including M&A. The company’s voice has matured from seeking validation to confidently claiming sector leadership and outlining a clear path for future, multi-dimensional growth, while providing more transparency about the levers and risks guiding its strategy.

Final Takeaway

Acorn Energy is in a growth phase, leveraging strong sector trends, a transformative telecom contract, new product launches, and a fresh NASDAQ uplisting. While financial discipline, channel strength, and growing C&I pipeline support upside, risks remain around single-customer dependency and limited near-term contract/cashflow visibility, especially as residential demand stays flat. Execution on large account wins and conversion of broadening RFP activity will be crucial going forward. Verdict: HOLD, upgradeable to BUY on evidence of large new or expanded wins.