ACCESS Newswire Inc. (NYSE: ACCS) – Q3 2025 Earnings

ACCESS Newswire Inc. (NYSE: ACCS) – Q3 2025 Earnings

Press release and earnings call link

Earnings Release Date: Nov. 11, 2025

Stock Price: $8.90

Market Cap: $34.3 million

Q3 2025 sales of $5.7 million vs $5.6 million in the prior year

Q3 2025 adjusted EPS of 0.20 vs 0.05 in the prior year

Q3 2025 diluted EPS of ($0.01) vs ($0.23) in the prior year

Overview: ACCESS Newswire is a PR/IR (public & investor relations) communications platform that distributes press releases, hosts earnings webcasts, and provides IR websites and related tooling. Headquartered in Raleigh, NC.

Revenue drivers (what they sell): Core press release distribution, webcasting/earnings calls, and IR websites; an increasing mix of subscriptions (recurring contracts) vs. one-off services.

Main customer/end-markets: Private enterprises, newly public companies/IPO issuers, and listed corporates running PR/IR workflows.

Market positioning: Share-gainer among the four major newswires; management claims multi-year market-share gains while larger rivals have ceded share.

Recent financial trajectory: Q3 revenue $5.7M (+2% YoY/Seq); gross margin 75%; operating loss narrowed to $184k; Adjusted EBITDA (non-GAAP) $933k (16% margin); YTD revenue down 2% but Adjusted EBITDA more than doubled to $2.3M.

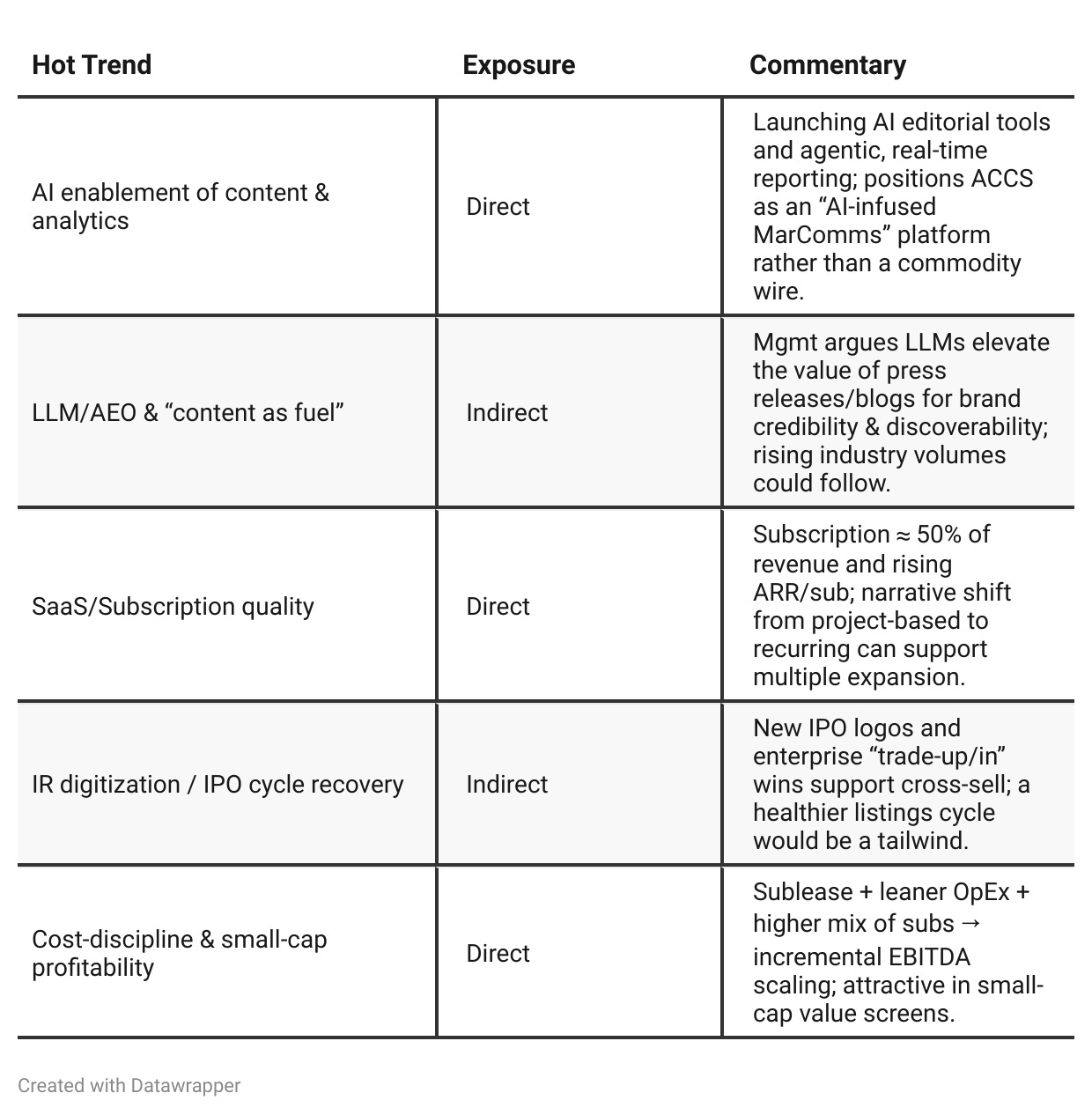

Near-term themes (from management): Push to subscription/ARR (annual recurring revenue), AI-driven editorial automation, social media integrations, “kill the report” real-time analytics, brand/education funnel (EDU program), continued cost discipline (office sublease).

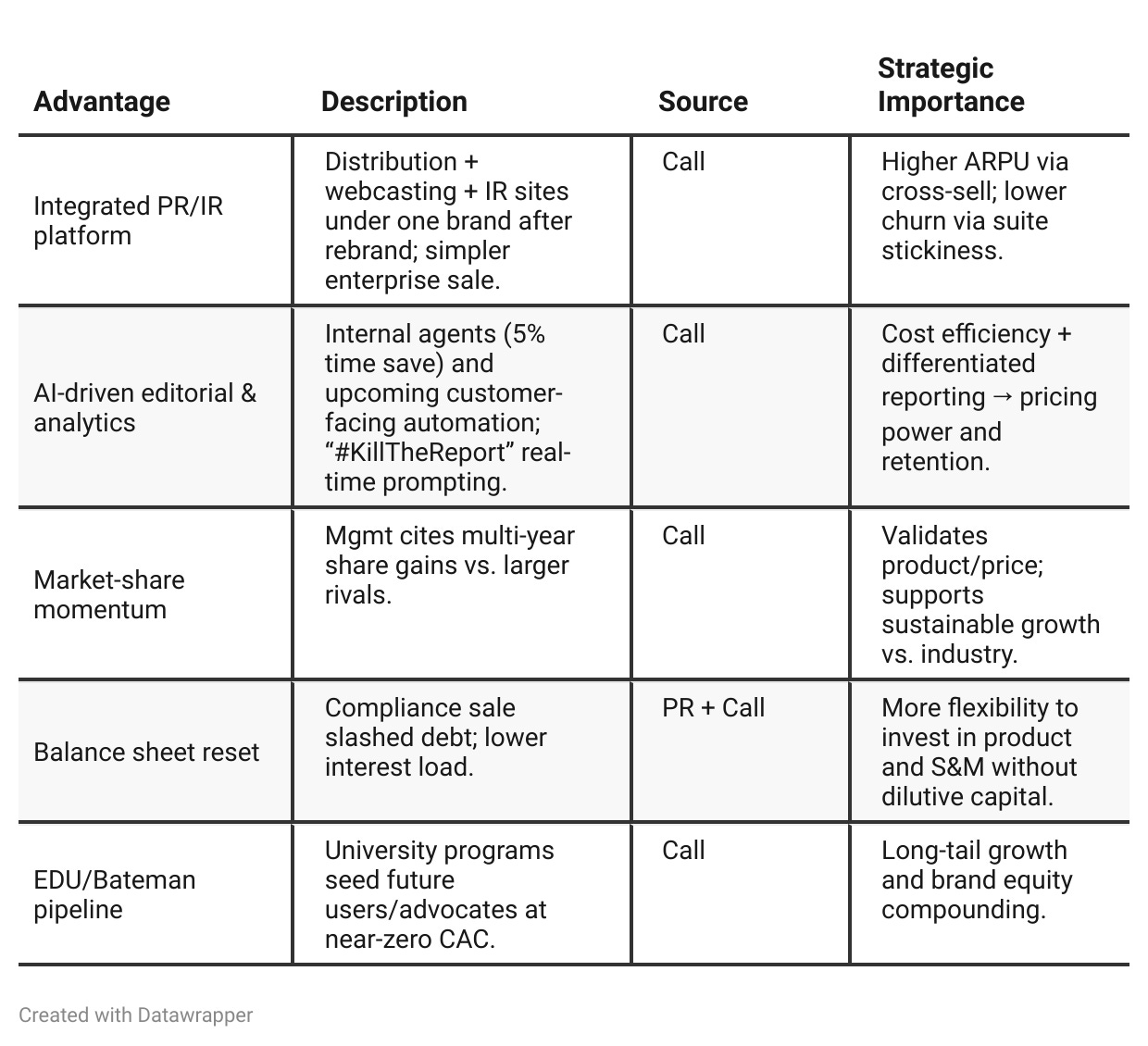

Competitive Advantage Insights

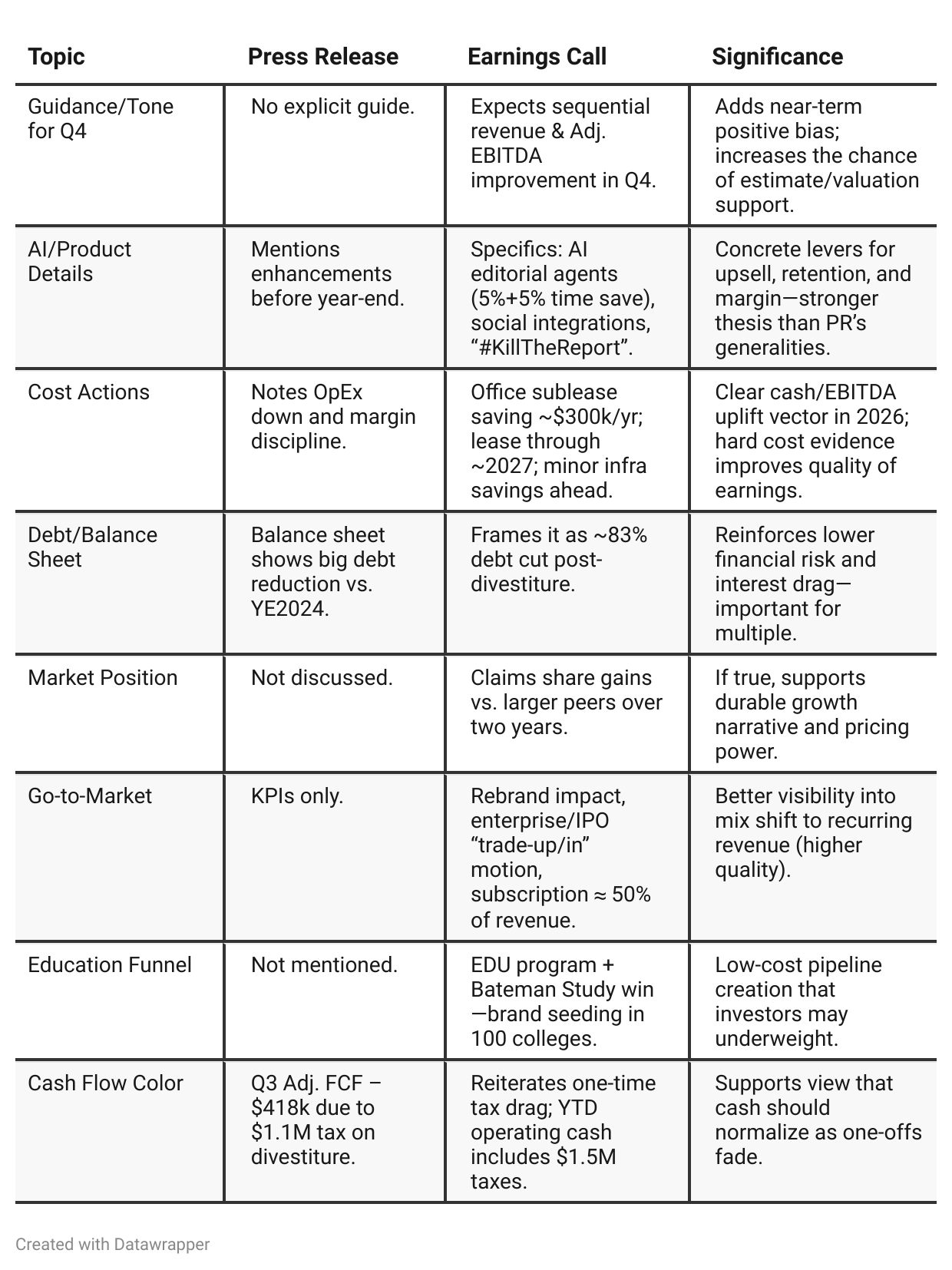

Press Release vs Call Transcript Comparison

Subscription quality vs. quantity: PR highlights 972 subs and $11,651 avg ARR/sub; the call suggests newer/renewing contracts trend around “$13k+” and that 2025’s sub count will likely miss the adjusted 1,200 target—but mgmt expects 1,500–1,600 subs by next year. That’s “fewer-subs-but-richer-ARR” now, with a return to higher net-adds later.

Segment pressure outside PR: Only the call spells out headwinds in webcasting/IR websites—useful for modeling mix and understanding why aggregate YTD revenue is slightly down despite PR growth.

Operational scalability metric: “ARR per employee” appears on the call only—this is a strong internal KPI for operating leverage not visible in the PR.

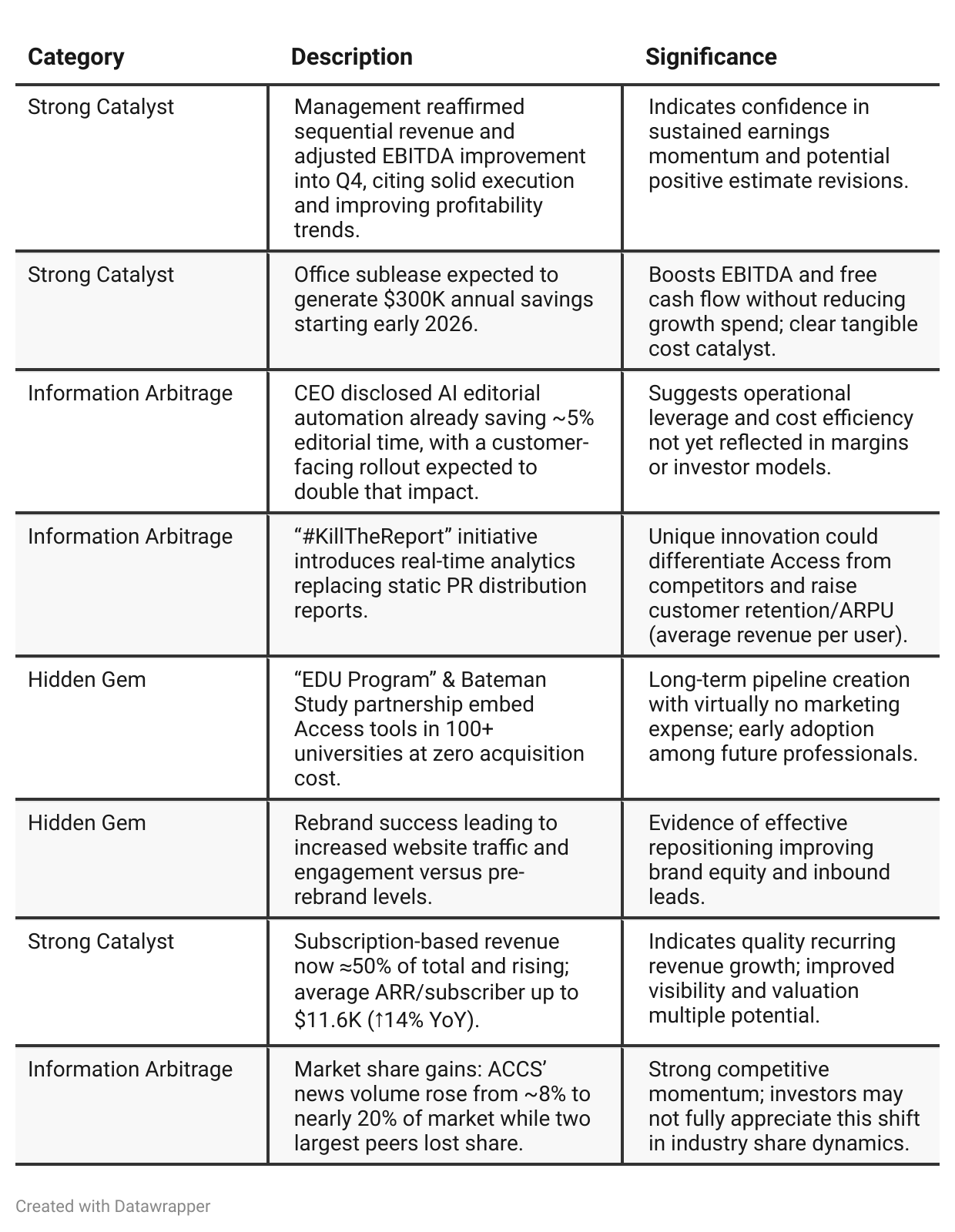

Positive Insights

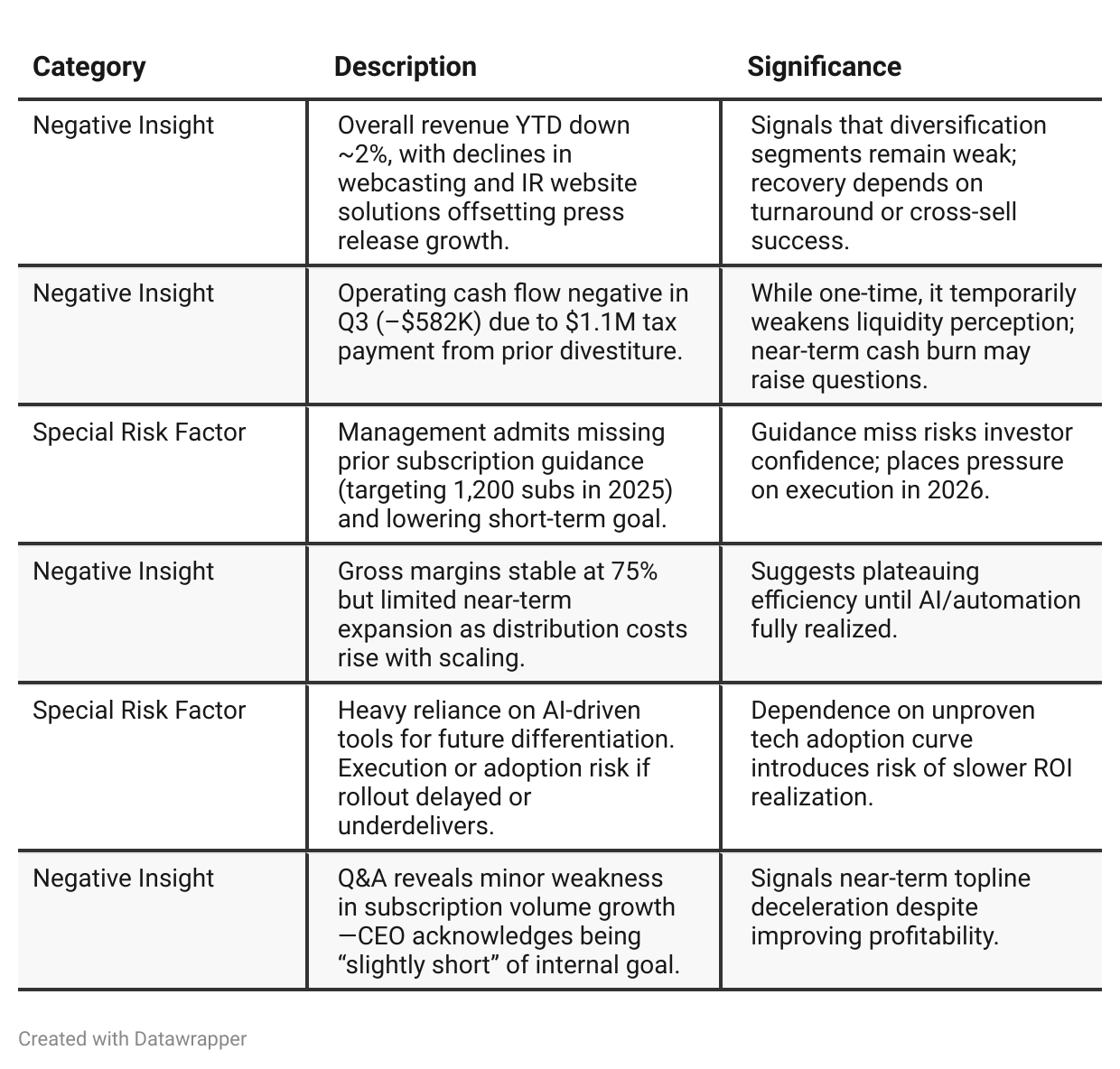

Negative Insights

Investor Underappreciation Signals

✅ AI-Powered Efficiency Gains — ACCESS is rolling out internal and customer-facing AI automation that cuts editorial time by up to 10% and boosts content quality. Investors may be underestimating how these tools could expand gross margins above the current 75% baseline as automation scales across operations in 2026.

✅ Subscription Momentum with Pricing Power — Average ARR per subscription customer jumped 14% year over year to $11,651. The market is likely focusing on slower customer count growth, missing that rising ARPU and retention point to durable pricing leverage and revenue compounding in 2026.

✅ Post-Divestiture Cost Tailwinds — Selling the compliance business cut debt by 83% and operating expenses by 7%, with an additional $300K annual savings expected from an office sublease. Because these structural savings were masked by temporary tax payments, investors may not yet be modeling the full EBITDA benefit visible by early 2026.

✅ Product Integration Catalysts — Upcoming platform upgrades will add real-time social media analytics and integrations with major management tools by year-end. These bundled capabilities can materially expand wallet share, yet investors may be discounting them until tangible ARR growth appears next quarter.

✅ Rebrand and Market Share Shift — The unified “Access Newswire” identity is driving higher customer engagement and helped the company gain share as rivals lost ground. The Street may still view the rebrand as cosmetic, overlooking how it strengthens enterprise credibility and accelerates new customer acquisition.

✅ Educational and PRSSA Partnership Flywheel — The new EDU program and Bateman Study partnership embed Access’s tools into 100+ universities. This initiative is an early-stage funnel for future professionals adopting the platform, an overlooked long-term demand driver that could surface gradually over 2026–2027.

✅ Industry Volume and AI Indexing Advantage — ACCESS is outperforming peers as industry leaders lose share, aided by its early focus on AI-driven news indexing for LLMs. The market may not yet recognize how this positioning secures lasting relevance in an AI-curated media environment poised for renewed volume growth.

Tariff Risk

No direct mentions of U.S. tariffs or trade policy in the transcript. The company’s cost base and operations are service- and software-oriented (PR/IR communications), with no manufacturing or import exposure. Thus, tariffs do not currently affect revenue or margins, and no mitigation strategies were discussed. The business is insulated from tariff volatility at present.

Hot Stock Trends Analysis

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Earlier call (Q2): ACCS was resetting the engine—digesting the compliance sale and rebrand, introducing ARR-per-employee, and laying groundwork for a subscription-led model, AI validation, and future reporting innovations, while acknowledging YoY revenue pressure and product timing delays.Latest call (Q3): ACCS is rolling down the runway—showing both sequential and YoY growth, a 16% Adj. EBITDA margin, and specific cost levers (sublease), while adding a competitively confident tone (share gains), new funnels (EDU/Bateman), near-term Q4 sequential improvement, and clearer product timing (customer-facing AI, social integrations, real-time reporting). Mix risk remains in webcasting/IR sites, but the story now leans toward profitable growth with identifiable catalysts.

Year-over-year comparison

Q3 2024:

Access (then Issuer Direct) was in transition mode—rebranding, integrating new AI features, and laying groundwork for a subscription-based “MediaSuite” platform. Financials were contracting, but management promised long-term ARR growth and a new AI-enabled ecosystem. The tone mixed ambition with defensiveness as they navigated declining compliance revenues and one-off project losses.Q3 2025:

Now as Access Newswire, the company presents a disciplined, execution-oriented narrative. Revenue and EBITDA are growing again, the compliance divestiture cleaned the balance sheet, and cost savings are tangible. AI automation, real-time analytics, and education-sector outreach provide differentiated growth paths. The story has evolved from “we’re building the future” to “we’re profitably scaling the platform we built.”

Final Takeaway

Access Newswire (AMEX: ACCS) is in a profitability-driven transition phase after divesting its compliance business. The company is focusing on subscription-based recurring revenue, AI-enabled workflow automation, and cost discipline. While growth in non-core segments remains tepid, market-share gains, rising ARR per subscriber, and cost savings create a foundation for a valuation re-rating. Execution on AI rollout, Q4 sequential growth, and EDU pipeline conversion will be critical to sustaining momentum.

Verdict: BUY, with upside potential tied to improved visibility and product adoption.